Abstract

Although private long-term care insurance (LTCI) is often discussed as a potential solution to the need for long-term care financing in the U.S., there is little empirical evidence on the economic consequences of having LTCI. We use U.S. Health and Retirement Study data to examine how LTCI affects key financial outcomes of insured individuals. Using an instrumental variable approach to account for the endogeneity of LTCI purchase, we find that LTCI leads to consistently positive effects on assets, consistently negative effects on Medicaid and Food Stamp enrolment and parent–child financial transfers, and ambiguous effects on out-of-pocket medical payments. These results suggest that although private LTCI does not entirely protect insured individuals against large medical expenditure, it improves the general financial well-being of insured individuals, potentially by reducing Medicaid-related disincentives to asset accumulation, motivating individuals to save more and reduce intergenerational wealth transfers.

Similar content being viewed by others

Notes

In 2014, the average monthly cost was USD 6000 for nursing home care and USD 4000 for home-based care in the U.S. (Genworth Financial 2014).

Medicare is a national health insurance programme administered by the U.S. federal government. It provides health insurance for individuals aged 65 and older, younger adults with certain disability status, and individuals with end-stage renal diseases or amyotrophic lateral sclerosis.

Medicaid is a joint federal and state programme that provides health insurance to people with limited income and resources.

In most states, an individual can keep USD 2000 in countable assets, and married couples who are still living in the same household can keep USD 3000 in countable assets.

For example, the federal government and some state governments offer tax subsidies for LTCI premiums, and the Partnership for LTC programme allows LTCI policyholders to keep more assets when they turn to Medicaid after their private policy benefits have been exhausted.

The Food Stamp Program (or Supplemental Nutrition Assistance Program) is a federal programme that provides food purchasing assistance for low-income Americans.

However, gifts or transfers made within 60 months prior to Medicaid application might be subject to penalties under the Deficit Reduction Act of 2005. Elderly people who plan to rely on Medicaid would need to start this process years before they need Medicaid.

The HRS question is “Are you currently covered by TRI-CARE, CHAMPUS, CHAMP-VA, or any other military health care plan?”

Non-housing financial assets are defined as the net value of stocks—mutual funds, investment trusts, bank accounts, certificates of deposit, Treasury bills, government bonds, bonds, and bond funds—less debt. Total assets are defined as the net value of non-housing financial assets—housing, real estate, vehicles, businesses, and Individual Retirement Account (IRA) /Keogh pension plan—less home loans.

Respondents are asked to report their household-level asset ownership and values. Those who do not provide an exact amount are then asked unfolding bracket questions. RAND imputes a consistent measure of wealth across all waves using bracketed responses and imputation models if an exact amount is not reported. See the RAND HRS Data Version N for a detailed description of the imputation method (RAND Center for the Study of Aging 2014).

Respondents are asked to report their individual-level spending on hospitals, nursing homes, doctors, dentists, outpatient surgery, prescription drugs, home-based care, and special facilities since the previous wave. For individuals who do not provide an exact value, RAND imputes a consistent measure of out-of-pocket medical expenditure across all waves using bracketed responses and imputation models. See the RAND HRS Data Version N for a detailed description of the imputation method (RAND Center for the Study of Aging 2014).

One of the main purposes of having LTCI is arguably to reduce the likelihood of having catastrophic out-of-pocket medical expenditure, defined as endangering the family's ability to maintain its customary standard of living. In our study, we directly measure the likelihood of having very large out-of-pocket medical expenditure. Given the average household income of USD 75,627 among our sample, USD 10,000 and USD 25,000 represent about 13% and 33% of the average household income, respectively.

Respondents are asked: “Not including government programs, do you now have any insurance which specifically pays any part of long-term care, such as personal or medical care in the home or in a nursing home?”.

Respondents are asked: “Does this plan cover care in a nursing home facility only, personal or long-term care at home, or both in-home and nursing home care?”

Number of diagnosed chronic conditions out of a list of 8 conditions, including hypertension, diabetes, cancer, lung diseases, heart problems, stroke, psychiatric problems, and arthritis.

AK, FL, NV, SD, TX, WA, and WY did not have an income tax, and NH and TN collected income tax only on interest and dividend income.

In 1998, among the 41 states and the District of Columbia that levied a broad-based personal income tax, 26 states and the District of Columbia provided a full exclusion for income from Social Security, and 10 states provided a full exclusion for income from pensions. As of 2010, only the State of Wisconsin had changed its tax policies and started to offer full exclusion for Social Security income in 2008 (Baer 2001; Edwards and Wallace 2004; McNichol 2006; Penner 2000; Snell 2011; Snell and Waisanen 2009).

2SRI IV estimates based on varying forms of residuals may be different (Basu and Coe 2017). We include the most commonly used response residuals in our 2SRI models.

Defined as individuals who need help with ADL/IADL, who have been diagnosed with memory-related diseases, and who have bad self-reported memory.

We drop individuals who indicated having LTCI but were not able to answer the coverage question.

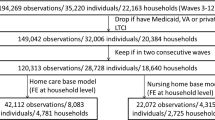

Among the 63,171 observations that meet our inclusion restrictions, 1199 observations have missing LTCI status and are not used in our analyses. Table 1 shows statistics for the 61,972 observations that have non-missing LTCI status.

We also assess the effects on financial assets and total assets using a wealthier sample, and we find larger effects. This suggests that the large treatment effects are driven by wealthier individuals, which is consistent with spend-down theory.

Because many LTCI policies have an elimination period, usually 30 to 100 days, during which the policyholders still have to pay their LTC out-of-pocket, we also use a higher out-of-pocket threshold, USD 50,000. We still find no significant effect.

References

Angrist, J.D., G.W. Imbens, and D.B. Rubin. 1996. Identification of causal effects using instrumental variables. Journal of the American Statistical Association 91 (434): 444–455. https://doi.org/10.2307/2291629.

Baer, D. 2001. State taxation of social security and pensions in 2000. Washington, D.C.: AARP Public Policy Institute.

Bassett, W.F. 2007. Medicaid’s nursing home coverage and asset transfers. Public Finance Review 35 (3): 414–439. https://doi.org/10.1177/1091142106293944.

Basu, A., and N.B. Coe. 2017. 2SLS vs 2SRI: Appropriate methods for rare outcomes and/or rare exposures. Health Economics. https://doi.org/10.1002/hec.3490.

Brown, J.R., and A. Finkelstein. 2004. The interaction of public and private insurance: Medicaid and the long-term care insurance market. Working Paper No. 10989. National Bureau of Economic Research. Retrieved from http://www.nber.org/papers/w10989.

Brown, J.R., and A. Finkelstein. 2007. Why is the market for long-term care insurance so small? Journal of Public Economics 91 (10): 1967–1991.

Centers for Medicare and Medicaid Services. 2008. Transfer of assets in the Medicaid program. MD: Baltimore.

Coe, N.B., G.S. Goda, and C.H. Van Houtven. 2015. Family spillovers of long-term care insurance. Working Paper No. 21483. National Bureau of Economic Research. Retrieved from http://www.nber.org/papers/w21483.

Congressional Budget Office. 2013. Rising demand for long-term services and supports for elderly people. Washington, DC: Congressional Budget Office.

De Nardi, M., E. French, and J.B. Jones. 2010. Why do the elderly save? The role of medical expenses. Journal of Political Economy 118 (1): 39–75. https://doi.org/10.1086/651674.

Edwards, B., and S. Wallace. 2004. State income tax treatment of the elderly. Public Budgeting & Finance 24 (2): 1–20. https://doi.org/10.1111/j.0275-1100.2004.02402001.x.

Efron, B. 1981. Nonparametric estimates of standard error: The jackknife, the bootstrap and other methods. Biometrika 68 (3): 589–599. https://doi.org/10.2307/2335441.

Finkelstein, A., and K. McGarry. 2006. Multiple dimensions of private information: Evidence from the long-term care insurance market. American Economic Review 96 (4): 938–958. https://doi.org/10.1257/aer.96.4.938.

Genworth Financial. 2014. 2014 Cost of care survey. VA: Richmond.

Goda, G.S. 2010. The impact of state tax subsidies for private long-term care insurance on coverage and Medicaid expenditures. Working Paper No. 16406. National Bureau of Economic Research. Retrieved from http://www.nber.org/papers/w16406.

Greenhalgh-Stanley, N. 2015. Are the elderly responsive in their savings behavior to changes in asset limits for Medicaid? Public Finance Review 43 (3): 324–346.

Gruber, J., and A. Yelowitz. 1999. Public health insurance and private savings. Journal of Political Economy 107 (6): 1249–1274.

Hubbard, R.G., J. Skinner, and S.P. Zeldes. 1995. Precautionary saving and social insurance. Journal of Political Economy 103 (2): 360–399.

Imbens, G.W., and J.D. Angrist. 1994. Identification and estimation of local average treatment effects. Econometrica 62 (2): 467–475. https://doi.org/10.2307/2951620.

Konetzka, R.T., D. He, J. Dong, M.J. Guo, and J.A. Nyman. 2017. Moral hazard and long-term care insurance. Working Paper.

Kopecky, K.A., and T. Koreshkova. 2014. The impact of medical and nursing home expenses on savings. American Economic Journal: Macroeconomics 6 (3): 29–72. https://doi.org/10.1257/mac.6.3.29.

Li, Y., and G.A. Jensen. 2011. The impact of private long-term care insurance on the use of long-term care. Inquiry: The Journal of Medical Care Organization, Provision and Financing 48 (1): 34–50.

McGuire, T.G. 2011. Demand for health insurance. In Handbook of Health Economics, vol. 2, ed. Mark V. Pauly, Thomas G. McGuire, and Pedro P. Barros, 317–396. New York: Elsevier.

McNichol, E.C. 2006. Revisiting state tax preferences for seniors. Washington, D.C.: Center on Budget and Policy Priorities.

Mor, V., J. Zinn, J. Angelelli, J.M. Teno, and S.C. Miller. 2004. Driven to tiers: Socioeconomic and racial disparities in the quality of nursing home care. The Milbank Quarterly 82 (2): 227–256. https://doi.org/10.1111/j.0887-378X.2004.00309.x.

Norton, E.C., and C.H. Van Houtven. 2006. Inter-vivos transfers and exchange. Southern Economic Journal 73 (1): 157–172. https://doi.org/10.2307/20111880.

Nyman, J.A. 2003. The theory of demand for health insurance. Stanford, CA: Stanford University Press.

Pauly, M.V. 1968. The economics of moral hazard: Comment. The American Economic Review 58 (3): 531–537.

Pauly, M.V. 1990. The rational nonpurchase of long-term-care insurance. Journal of Political Economy 98 (1): 153–168.

Penner, R.G. 2000. Tax benefits for the elderly. Occasional Paper No. 5. Washington, D.C.: The Urban Institute.

RAND Center for the Study of Aging. 2014. RAND HRS longitudinal data file 2014 (V2), supported by NIA and SSA. Retrieved September 2, 2015, from http://www.rand.org/labor/aging/dataprod/hrs-data.html.

Snell, R. 2011. State personal income taxes on pensions and retirement income: Tax year 2010. Denver, CO: National Conference of State Legislatures.

Snell, R., and B. Waisanen. 2009. State personal income taxes on pensions and retirement income: Tax year 2008. Denver, CO: National Conference of State Legislatures.

Sperber, N.R., C.I. Voils, N.B. Coe, R.T. Konetzka, J. Boles, and C.H. Van Houtven. 2014. How can adult children influence parents’ long-term care insurance purchase decisions? The Gerontologist 57 (2): 292–299. https://doi.org/10.1093/geront/gnu082.

Terza, J.V., A. Basu, and P.J. Rathouz. 2008. Two-stage residual inclusion estimation: Addressing endogeneity in health econometric modeling. Journal of Health Economics 27 (3): 531–543. https://doi.org/10.1016/j.jhealeco.2007.09.009.

Thompson, L. 2004. Long-term care: Support for family caregivers (Issue Brief). Georgetown University.

Waidmann, T., and K. Liu. 2006. Asset transfer and nursing home use: Empirical evidence and policy significance. Washington, DC Kaiser Family Foundation. Retrieved from http://kff.org/medicaid/issue-brief/asset-transfer-and-nursing-home-use-empirical/.

Zeckhauser, R. 1970. Medical insurance: A case study of the tradeoff between risk spreading and appropriate incentives. Journal of Economic Theory 2 (1): 10–26. https://doi.org/10.1016/0022-0531(70)90010-4.

Author information

Authors and Affiliations

Corresponding author

Appendix

Appendix

Rights and permissions

About this article

Cite this article

Dong, J., Smieliauskas, F. & Konetzka, R.T. Effects of long-term care insurance on financial well-being. Geneva Pap Risk Insur Issues Pract 44, 277–302 (2019). https://doi.org/10.1057/s41288-018-00113-7

Received:

Accepted:

Published:

Issue Date:

DOI: https://doi.org/10.1057/s41288-018-00113-7