Abstract

The study explores the holiday effect on stock price reactions to analyst recommendation revisions and on post-recommendation price drifts. Based on the Mood Maintenance Hypothesis and on the literature documenting lower stock trading activity before holidays, I hypothesize that if a recommendation revision is issued before a holiday, then investors striving to maintain their positive pre-holiday mood, may be less willing to make influential trading decisions, and therefore, may underreact to the recommendation revision, leading to stronger post-recommendation price drift. Analyzing a large sample of analyst recommendation revisions, I document that, compared to “regular” recommendation revisions, pre-holiday recommendation revisions are followed by: (i) significantly weaker event-day stock price reactions, and (ii) significantly more pronounced post-event price drifts, whose magnitude increases over longer post-event periods (up to 6 months). Both effects are more pronounced for small and more volatile stocks and remain robust after accounting for additional company- (size, market model beta, historical volatility) and event-specific (number of recommendation categories changed in the revision, analyst experience) factors.

Similar content being viewed by others

Notes

The two datasets are merged based on either CUSIP or exchange tickers combined with the requirement that the period these identifiers are used in the datasets overlap.

In order to test if the holiday effect on stock price reactions to analyst recommendation revisions is not predominantly driven by any one of the public holidays, I have repeated my analysis by consecutively omitting one of the nine public holidays at a time (that is, excluding from my analysis the recommendation revisions, which took place prior to this specific holiday). The results (available upon request from the author) are homogeneous (and similar to those reported in “Results description” section for the whole list of holidays), indicating that all the public holidays have exerted approximately similar effects on the way investors treated recommendation revisions.

Alternatively, I calculate ARs using Market-Adjusted Returns (MAR)—return differences from the market index, and the Fama-French three-factor model. The results (available upon request from the author) remain qualitatively similar to those reported in “Results description” section.

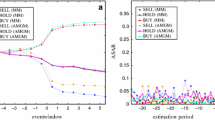

It should be noted that pre-holiday recommendation revisions make up slightly less than 3% of the study's working sample. Still, 2168 (2416) pre-holiday recommendation upgrades (downgrades) accumulated over the 15-year sampling period are sufficient for obtaining statistically significant results.

I have repeated the tests, whose results are reported in “Holiday effect on post-recommendation stock returns within different stock groups” and “Multifactor analysis” sections, for the post-event time windows employed in Table 4. The holiday effect on CAR (2, 5) remained weak and nonsignificant, so that the results for CAR (6, 21), CAR (6, 63) and CAR (6, 126) were very similar to those for CAR (2, 21), CAR (2, 63) and CAR (2, 126), respectively, as reported in Tables 5, 6 and 7. The detailed results are available upon request from the author.

The results for medium capitalization stocks indicate that these stocks are less influenced by the holiday effect (on both event-day ARs and post-event drifts) than low capitalization stocks, and more influenced by the holiday effect than high capitalization stocks. The detailed results are available upon request from the author. Overall, the results demonstrate that the holiday effect on stock price reactions to recommendation revisions decreases with market capitalization.

The sample partition approach by both market capitalization and historical stock volatility is similar to the one employed by Kliger and Kudryavtsev (2010).

The results for medium volatility stocks indicate that these stocks are less influenced by the holiday effect (on both event-day ARs and post-event drifts) than high volatility stocks, and more influenced by the holiday effect than low volatility stocks. The detailed results are available upon request from the author. Overall, the results demonstrate that the holiday effect on stock price reactions to recommendation revisions increases with historical stock volatility.

I have also performed the analysis of event-day and post-event ARs for three subsamples partitioned by the CAPM stock beta calculated over Days − 251 to − 1. In line with Baker and Wurgler (2006), I have documented that the holiday effect on stock price reactions to recommendation revisions (expressed both in weaker event-day price reactions and higher post-event price drifts) increases with stock beta. The detailed results are available upon request from the author.

References

Agrawal, A., and K. Tandon. 1994. Anomalies or Illusions?: Evidence from stock markets in eighteen countries. Journal of International Money and Finance 13(1): 83–106.

Ariel, R.A. 1990. High stock returns before holidays: Existence and evidence on possible causes. Journal of Finance 45(5): 1611–1626.

Baker, M., and J. Wurgler. 2006. Investor sentiment and the cross-section of stock returns. Journal of Finance 61(4): 1645–1680.

Barber, B., R. Lehavy, M. McNichols, and B. Trueman. 2001. Can investors profit from the prophets? Security analyst recommendations and stock returns. Journal of Finance 56(2): 531–563.

Barone, E. 1990. The Italian stock market: Efficiency and calendar anomalies. Journal of Banking & Finance 14(2): 483–510.

Bergsma, K., and D. Jiang. 2015. Cultural New Year holidays and stock returns around the world. Financial Management 45(1): 3–35.

Beyer, A., D.A. Cohen, T.Z. Lys, and B.R. Walther. 2010. The financial reporting environment: Review of the recent literature. Journal of Accounting and Economics 50(2–3): 296–343.

Bley, J., and M. Saad. 2010. Cross cultural differences in seasonality. International Review of Financial Analysis 19(4): 306–312.

Boni, L., and K.L. Womack. 2006. Analysts, industries, and price momentum. Journal of Financial and Quantitative Analysis 41(1): 85–109.

Brav, A., and R. Lehavy. 2003. An empirical analysis of analysts’ target prices: Short-term informativeness and long-term dynamics. Journal of Finance 58(5): 1933–1968.

Brockman, P. 1995. A review and analysis of the holiday effect. Financial Markets, Institutions and Instruments 4(5): 37–58.

Brockman, P., and D. Michayluk. 1997. The holiday anomaly: An investigation of firm size versus share price. Quarterly Journal of Business and Economics 36(3): 23–35.

Brockman, P., and D. Michayluk. 1998. The persistent holiday effect: Additional evidence. Applied Economics Letters 5(2): 205–209.

Cadsby, C., and M. Ratner. 1992. Turn of the month and pre holiday effects on stock returns: Some international evidence. Journal of Banking & Finance 16(3): 497–509.

Cao, X., I.M. Premachandra, G.S. Bharba, and Y.P. Tang. 2009. Firm size and the pre-holiday effect in New Zealand. International Research Journal of Finance and Economics 32: 171–187.

Chan, M., A. Khanthavit, and H. Thomas. 1996. Seasonality and cultural influences on four Asian stock markets. Asia Pacific Journal of Management 13(2): 1–24.

Della Vigna, S., and J. Pollet. 2009. Investor inattention and friday earnings announcements. Journal of Finance 64(2): 709–749.

Diether, K.B., C.J. Malloy, and A. Scherbina. 2002. Differences of opinion and the cross-section of stock returns. Journal of Finance 57(5): 2113–2141.

Dodd, O., and A. Gakhovich. 2011. The holiday effect in Central and Eastern European financial markets. Investment Management and Financial Innovations 8(4): 29–35.

Elton, E.J., M.J. Gruber, and S. Grossman. 1986. Discrete expectational data and portfolio performance. Journal of Finance 41(3): 699–713.

Erber, R., and A. Tesser. 1992. Task effort and the regulation of mood: The absorption hypothesis. Journal of Experimental Social Psychology 28(4): 339–359.

Francis, J., and L. Soffer. 1997. The relative informativeness of analysts’ stock recommendations and earnings forecast revisions. Journal of Accounting Research 35(2): 193–211.

Frankel, R., S.P. Kothari, and J. Weber. 2006. Determinants of the informativeness of analyst research. Journal of Accounting and Economics 41(1): 29–54.

Frieder, L., and A. Subrahmanyam. 2004. Nonsecular regularities in returns and volume. Financial Analysts Journal 60(4): 29–34.

Gavriilidis, K., P. Herbst, and A. Kagkadis, 2016, Investor attention to stock recommendations, Working Paper, University of Stirling.

Gleason, C., and C. Lee. 2003. Analyst forecast revision and market price discovery. The Accounting Review 78(1): 193–225.

Green, C.T. 2006. The value of client access to analyst recommendations. Journal of Financial and Quantitative Analysis 41(1): 1–24.

Grossman, S. 1995. Dynamic asset allocation and the informationally efficiency of markets. Journal of Finance 50(5): 773–778.

Healy, P.M., and K.G. Palepu. 2001. Information asymmetry, corporate disclosure, and the capital markets: A review of the empirical disclosure literature. Journal of Accounting and Economics 31(1–3): 405–440.

Hirschleifer, D., D. Jiang, and Y. Meng, 2016, Mood beta and seasonalities in stock returns, Working Paper, IVEY Business School.

Hirshleifer, D., S.S. Lim, and S.H. Teoh. 2011. Limited investor attention and stock market misreactions to accounting information. Review of Asset Pricing Studies 1(1): 35–73.

Isen, A.M. 1984. Toward understanding the role of affect in cognition. In Handbook of social cognition, ed. R.S. Wyer and T.K. Srull, 179–236. Hillsdale, NJ: Erlbaum.

Isen, A.M., 2000, Positive affect and decision making. In Handbook of emotions, ed. M. Lewis and J. M. Havieland, Vol. 2, 417–435. London: Guilford.

Jegadeesh, N., J. Kim, and S.D. Krische. 2004. Analyzing the analysts: When do recommendations add value? The Journal of Finance 59(3): 1083–1124.

Jegadeesh, N., and W. Kim. 2010. Do analysts herd? An analysis of recommendations and market reactions. Review of Financial Studies 23(2): 901–937.

Kavanagh, D.J., and G.H. Bower. 1985. Mood and self-efficacy: Impact of joy and sadness on perceived capabilities. Cognitive Therapy and Research 9(5): 507–525.

Kecskes, A., R. Michaely, and K.L. Womack, 2010, What drives the value of analysts’ recommendations: Earnings estimates or discount rate estimates? Working paper, Darthmouth College.

Keef, S.P., and M.L. Roush. 2005. Day-of-the-week effects in the pre-holiday returns of the standard & poor’s 500 stock index. Applied Financial Economics 15(1): 107–119.

Keim, D.B. 1989. Trading patterns, bid-ask spreads and estimated security returns: The case of common stocks at calendar turning points. Journal of Financial Economics 25(1): 57–67.

Kim, C.W., and J. Park. 1994. Holiday effects and stock returns: Further evidence. Journal of Financial and Quantitative Analysis 29(1): 145–157.

Kliger, D., and A. Kudryavtsev. 2010. The availability heuristic and investors’ reaction to company-specific events. The Journal of Behavioral Finance 11(1): 50–65.

Kuykendall, D., and J.P. Keating. 1990. Mood and persuasion: Evidence for the differential impact of positive and negative states. Psychology and Marketing 7(1): 1–9.

Lang, M.H., and R.J. Lundholm. 1996. Corporate disclosure policy and analyst behavior. Accounting Review 71(4): 467–492.

Lakonishok, J., and S. Smidt. 1988. Are seasonal anomalies real? A 90 year perspective. Review of Financial Studies 1(4): 403–425.

Li, F., C. Lin, and T.C. Lin, 2016, The 52-week high stock price and analyst recommendation revisions, Working Paper, University of Hong Kong.

Li, K., J. Lockwood, L. J. Lockwood, and M. R. Uddin, 2015, Analyst optimism and stock price momentum, Working Paper.

Liano, K., P.H. Marchand, and G.C. Huang. 1992. The holiday effect in stock returns: Evidence from the OTC market. Review of Financial Economics 2(1): 45–54.

Loh, R.K. 2010. Investor inattention and the underreaction to stock recommendations. Financial Management 39(3): 1223–1252.

Loh, R.K., and G.M. Mian. 2006. Do accurate earnings forecasts facilitate superior investment recommendations? Journal of Financial Economics 80(2): 455–483.

Loh, R.K., and R.M. Stulz. 2011. When are analyst recommendation changes influential? Review of Financial Studies 24(2): 593–627.

Mackie, D.M., and L.T. Worth. 1989. Processing deficits and the mediation of positive affect in persuasion. Journal of Personality and Social Psychology 57(1): 27–40.

Malkiel, B.G., and E.F. Fama. 1970. Efficient capital markets: A review of theory and empirical work. Journal of Finance 25(2): 383–417.

Marrett, G.K., and A.C. Worthington. 2009. An empirical note on the holiday effect in the Australian stock market. Applied Financial Letters 16(17): 1769–1772.

Meneu, V., and A. Pardo. 2004. Pre-holiday effect, large trades and small investor behavior. Journal of Empirical Finance 11(2): 231–246.

Michaely, R., and K.L. Womack, 2006, What are analysts really good at? Working Paper, Darthmouth College.

Mikhail, M.B., B.R. Walther, and R.H. Willis. 2004. Do security analysts exhibit persistent differences in stock picking ability? The Journal of Financial Economics 74(1): 67–91.

Nagel, S. 2005. Short sales, institutional investors and the cross-section of stock returns. Journal of Financial Economics 77(2): 277–309.

Peng, L., and W. Xiong. 2006. Investor attention, overconfidence, and category learning. Journal of Financial Economics 80(3): 563–602.

Pettengill, G.N. 1989. Holiday closings and security returns. Journal of Financial Research 12(1): 57–67.

Schwarz, N. 2001. Feelings as information: Implications for affective influences on information processing. In Theories of mood and cognition: A user’s guidebook, ed. L.L. Martin and G.L. Clore, 159–176. Mahwah: Erlbaum.

Sorescu, S., and A. Subrahmanyam. 2006. The cross section of analyst recommendations. Journal of Financial and Quantitative Analysis 41(1): 139–168.

Stickel, S.E. 1995. The anatomy of the performance of buy and sell recommendations. Financial Analysts Journal 51(5): 25–39.

Thaler, R.H. 1999. The end of behavioral finance. Financial Analyst Journal 55(6): 12–17.

Vergin, R.C., and J. McGinnis. 1999. Revisiting the holiday effect: Is it on holiday? Applied Financial Economics 9(3): 477–482.

Womack, K.L. 1996. Do brokerage analysts recommendations have investment value? Journal of Finance 51(1): 137–167.

Author information

Authors and Affiliations

Corresponding author

Rights and permissions

About this article

Cite this article

Kudryavtsev, A. Holiday effect on stock price reactions to analyst recommendation revisions. J Asset Manag 19, 507–521 (2018). https://doi.org/10.1057/s41260-018-0095-6

Revised:

Published:

Issue Date:

DOI: https://doi.org/10.1057/s41260-018-0095-6

Keywords

- Analyst Recommendation Revisions

- Behavioral Finance

- Holiday Effect

- Mood Maintenance Hypothesis

- Stock Price Drifts