Abstract

The November 2014 Saudi gambit to increase oil production and drive down prices was a deliberate decision to quell the shale oil revolution. Ostensibly, that decision has been very costly to the Saudis, but the relevant question is would they find themselves worse off had they not acted. This paper presents a counterfactual analysis of that decision and finds that to have continued to cut production to sustain high prices would have been worse yet. Consequently, because of the shale revolution, future oil prices appear likely to fluctuate between a new floor and new ceiling price. A critical question then becomes what role will OPEC play in affecting prices within this new range of variation. This paper presents two contrasting views.

Similar content being viewed by others

Notes

For example, see Bazzi (2014).

See Goldsmith (2014).

See Goldwyn (2015).

See Evans-Pritchard (2014).

These shale formations contain high porosity of hydrocarbons but low permeability preventing the hydrocarbons from flowing to the well bore. Hydraulic fracturing, which uses large volumes of water and sand, effectively creates permeability by fracturing the tight oil/shale formations. At the same time, the combination of horizontal drilling allows the well bore to penetrate the formation horizontally, creating interaction with the shale formation over distances as long as several miles.

A superficial calculation might conclude that finding costs per barrel less are only about $14/barrel. But this overlooks the fact that these wells produce large quantities of natural gas which sells for much less than oil on a BTU basis.

We choose to adopt $100/barrel as the counterfactual price even though at the time of the November 2014 OPEC meeting, oil prices were already below $100/barrel. The rationale is that a sizeable contingent of OPEC producers were proposing output cuts in an effort to re-establish the previous trading range from 2011 to August 2014. By choosing $100/barrel as the counterfactual price instead of $80/barrel, Saudi revenues would have been 20% lower. A lower counterfactual price would imply that the Saudi decision was even less costly than at $100/barrel. Thus, by choosing $100/barrel as a counterfactual price, the analysis tends to favor the contention that the Saudi gambit was a mistake.

Interestingly, after prices plummeted to $8/barrel, order was restored in the cartel by the Saudis adopting a tit-for-tat strategy to deter cheating. See Griffin and Neilson (1994).

This was the hay-day of the peak oil theorists. At the same time, Matthew Simmons (2005) published his book, “Twilight in the Desert,” asserting that Saudi oil reserves were grossly over-stated as well.

Because this latter figure is reported in barrels of oil equivalent (converting natural gas to barrels of oil based on its BTU content), it masks the effect of drilling locations with greater liquid content. Given the relative low price of natural gas, producers likely focused on locations with greater oil content.

In an interesting paper, Smith and Lee (2017) recognize the importance of excess capacity and attempts to include these effects in his reserves analysis.

See Smith and Lee (2017).

James Sweeney (2016) illustrates their importance and provides an interesting analysis of the various sources of efficiency gains in energy conservation.

See Cunningham (2016).

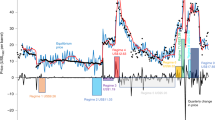

Over the period 2014–2016, Iraqi production increased by 1.1 MMB/D while Iranian production increased by 0.9 MMB/D.

Potentially, some countries might join Saudi Arabia in cutting output while other members could offset these cuts by increasing output.

Smith and Lee (2017) contend that the price floor could be as low as $20/barrel. This assumption does not account for uncertainties in drilling and fracking as well as the assumption of a log-normal distribution of drilling sites.

Interestingly, Pashigian’s limit pricing model, while not intended for oil, appears directly applicable.

See Aguilera and Radetzki (2016), p.4.

Ibid, p. 77.

Ibid, p. 208.

Based on the short-run price elasticity in Griffin and Schulman (2005), a 1-MMB/D output cut could increase oil prices from $50 to $65/barrel in the absence of any cheating or supply response by non-OPEC producers. But even after allowing for these other factors, the price effects can be substantial.

Griffin and Neilson (1994) explore various game theoretic methods to deter cheating and conclude that particularly in the late 1980s that a “tit-for-tat” strategy was used with some success by the Saudis. They show that the Saudis ignored minor levels of cheating recognizing that small producers have more incentives to cheat. But the Saudis moved aggressively to punish large-scale cheating, with the result that after punishment, prices returned to higher levels.

See Griffin (2009), p. 45.

See Wingfield et al. (2017).

For a discussion, see Griffin and Xiong (1997).

For some interesting estimates for various plays, see Smith and Lee (2017).

References

Adelman MA (2001) The clumsy cartel: OPEC’s uncertain future. Harv Int Rev 23(1):20–23

Aguilera RF, Radetzki M (2016) The price of oil. Cambridge University Press, Cambridge. https://doi.org/10.1017/CBO9781316272527

Bazzi M (2014) Saudi Arabia is using oil as a weapon to punish Russia and Iran. Hurriyet Daily News, December 22, 2014

Campbell CS, Laherrere JH (1998) The end of cheap oil. Sci Am 278(3):78–83. https://doi.org/10.1038/scientificamerican0398-78

Cunningham N (2016) 27 billion barrels worth of oil projects now cancelled. OilPrice.com. http://oilprice.com/energy/crude-oil/27-billion-barrels-worth-of-oil-projects-now-cancelled.html. Accessed 10 October 2017

Evans-Pritchard A (2014) Saudis risk playing with fire in shale-price showdown as crude crashes. The Telegraph, November 30, 2014

Evans-Pritchard A (2016) Texas shale has fought Saudi Arabia to a standstill. Financial Times, July 31, 2016

Goldsmith S (2014) Oil update: this is the real reason OPEC didn’t cut production. The Crux, December 4, 2014

Goldwyn D (2015) Here’s why Saudi Arabia has let oil prices fall—and why they could revive by year’s end. Atlantic Council, January 20, 2015

Griffin JM (2009) A smart energy policy: an economist’s Rx for balancing cheap, clean, and secure energy. Yale University Press, New Haven. https://doi.org/10.12987/yale/9780300149852.001.0001

Griffin JM, Neilson WS (1994) The 1985-86 oil price collapse and afterwards: what does game theory add? Econ Inq 32(4):543–561. https://doi.org/10.1111/j.1465-7295.1994.tb01350.x

Griffin JM, Schulman CT (2005) Price-asymmetry in energy demand models: a proxy for energy-saving technical change? Energy J 26(2):1–22. https://doi.org/10.2307/41323059

Griffin JM, Xiong W (1997) The incentive to cheat: an empirical analysis of OPEC. J Law Econ 40(2):289–316. https://doi.org/10.1086/467374

Pashigian BP (1968) Limit price and the market share of the leading firm. J Ind Econ 16(3):165–177. https://doi.org/10.2307/2097557

Simmons MR (2005) Twilight in the desert: the coming Saudi oil shock and the world economy. Wiley & Sons, Hoboken

Smith JL, Lee TK (2017) The price elasticity of U.S. shale oil reserves. Energy Econ 67:121–135. https://doi.org/10.1016/j.eneco.2017.06.021

Sweeney J (2016) Energy efficiency: building a clean, Secure Economy. Hoover Institution Press, Stanford

Wingfield B, Dodge S, Sam C (2017) OPEC’s allies race ahead on output cuts. Bloomberg, September 2017. https://www.bloomberg.com/graphics/2017-opec-production-targets/. Accessed 10 Oct 2017

Acknowledgments

The author wishes to thank Michael Pollard and F. Gregory Gause as well as an anonymous referee for helpful suggestions. Shelby Ponzik and Cynthia Gause provided excellent editorial assistance.

Author information

Authors and Affiliations

Corresponding author

Rights and permissions

About this article

Cite this article

Griffin, J.M. The Saudi 2014 gambit: a counterfactual analysis. Miner Econ 31, 253–261 (2018). https://doi.org/10.1007/s13563-017-0134-7

Received:

Accepted:

Published:

Issue Date:

DOI: https://doi.org/10.1007/s13563-017-0134-7