Abstract

Using the Survey of Income and Program Participation from 2001, 2004, and 2008 and federal and state variation in earned income tax credit generosity over time, I investigate how changes in expected household earned income tax credit benefits associated with marriage affect cohabitation and marriage behavior among low-income single mothers. I simulate a marriage market to predict potential spouse earnings for a sample of single mothers in order to estimate the potential losses or gains in earned income tax credit benefits upon marriage. Using multinomial logistic regressions, I then analyze how the anticipated loss in earned income tax credit benefits upon marriage affects the likelihood of marrying or cohabiting. Results suggest that the average earned income tax credit-eligible woman can expect to lose approximately US$1,300 in earned income tax credit benefits in the year following marriage, or about half of pre-marriage benefits. Single mothers who expect to lose earned income tax credit benefits upon marriage are 2.5 percentage points less likely to marry their partners and 2.5 percentage points more likely to cohabit compared to single mothers who expect no change or to gain earned income tax credit benefits upon marriage. Despite recent policy efforts to reduce the size of the marriage penalty embedded in the earned income tax credit structure, these results suggest that the earned income tax credit still creates distortions in marriage and cohabitation decisions among low-income single mothers.

Similar content being viewed by others

Notes

Recent studies have found that marginal tax rates for a second earner approach nearly 70 %, once accounting for the phase out of the EITC and other means-tested programs such as food stamps (Kearney and Turner 2013).

All dollars are scaled to 2014 dollars using the consumer price index.

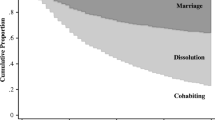

Many of these studies focus on cohabiting couples where both individuals are the biological parents of the children in the household. In my sample, approximately half of the women who cohabit do so with the biological father, while only 25 % of women who marry do so with the biological father of her children.

I focus on single mothers, as they are the primary recipients of the EITC, but results are quite similar including childless single women in the analysis as well (see Supplementary appendix Table A2).

I exclude single mothers with a college degree from the analysis since there were very few that were eligible for the EITC, and those that were eligible are likely quite different from lower-educated single mothers. Results are robust to including college-educated single mothers and are available upon request.

Approximately half of the single mothers who cohabit during the survey window do so with a man who is biologically related to at least one child in the household. Approximately 25 % of the single mothers who married married the biological father of at least one of the children in the household. The biological father was determined by whether any children of the respondent reported having a biological father in the household.

A qualifying child is a biological child, adopted child, sibling, or descendent of any of these (such as grandchild or niece/nephew) who resides in the home for at least 6 months, or a foster child who lives in the house for the entire year (Internal Revenue Service 2013).

In some analyses, I also model the dollar amount of expected gain or loss as a linear function or parameterized into quintiles of expected change in EITC benefits upon marriage.

Sample size limitations prevent conducting separate spouse matches within each state.

As an additional robustness check, I also test the sensitivity of results to matching all respondents to spouses earning either $1000; $5000; or $10,000. This eliminates the variation in the expectation to lose benefits generated by the spouse match and instead relies on variation generated by federal and state policy changes to the EITC, as well as respondent earnings and number of children.

Results were quite similar using a logistic regression to predict the likelihood of marrying compared to remaining unmarried. Results available upon request.

A few individuals experience a transition to both cohabitation and marriage over the time period, so I code these individuals as married by the end of the survey. Approximately 4 % of the sample experiences both a cohabitation and a marriage within the 36–60 month surveys.

I also restricted the window to the first 12 months of the survey. Results are also presented in Supplementary appendix Table A4 and indicate no significant marriage patterns in the first year of the SIPP panel for women who expect to lose benefits upon marriage. Expectations to lose EITC benefits upon marriage may not be immediately realized, households may take a few years to respond to policy changes in the tax code.

Those who expect no change or to gain benefits upon marriage have a zero for the dollar amount of the expected loss in EITC benefits.

A parallel analysis modeling whether a respondent expects to gain benefits upon marriage is presented in Supplementary appendix Table A6 and provides consistent results with those discussed thus far. Women who expect to gain EITC benefits upon marriage are more likely to marry compared to those who expect to lose benefits upon marriage. Far fewer single mothers expect to gain EITC benefits upon marriage than the share who lose benefits, thus these results are somewhat less precise. Only 22 % of the sample expects to gain any benefits upon marriage, with just 12 % gaining more than $1000.

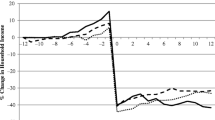

See Fig. 2 for an illustration of how the marriage penalty changes over time.

References

Alm, J., Dickert-Conlin, S., & Whittington, L. A. (1999). Policy watch: The marriage penalty. The Journal of Economic Perspectives, 13(3), 193–204.

Alm, J., & Whittington, L. A. (2003). Shacking up or shelling out: Income taxes, marriage, and cohabitation. Review of Economics of the Household, 1(3), 169–186.

Baughman, R., & Dickert-Conlin, S. (2009). The earned income tax credit and fertility. Journal of Population Economics, 22, 537–563.

Becker, G. (1974). A theory of marriage: Part II. Journal of Political Economy, 82(2), 511–26.

Bertrand, M., Kamenica, E., & Pan, J. (2013). Gender identity and relative income within households (No. w19023). National Bureau of Economic Research.

Bitler, M. P., Gelbach, J. B., Hoynes, H. W., & Zavodny, M. (2004). The impact of welfare reform on marriage and divorce. Demography, 41(2), 213–236.

Bumpass, L., & Lu, H. (2000). Trends in cohabitation and implications for children’s family contexts in the United States. Population Studies, 54(1), 29–41.

Dahl, G. B., & Lochner, L. (2012). The impact of family income on child achievement. American Economic Review, 102(5), 1927–1956.

DeLeire, T., & Kalil, A. (2005). How do cohabiting couples with children spend their money?. Journal of Marriage and Family, 67(2), 286–295.

Dickert-Conlin, S., & Houser, S. (2002). EITC and marriage. National Tax Journal, 55, 25–40.

Edin, K. (2000). What do low-income single mothers say about marriage?. Social Problems, 47(1), 112–133.

Edin, K., & Kefalas, M. (2005). Promises I can keep: Why poor women put motherhood before marriage. Berkeley: University of California Press.

Eissa, N., & Hoynes, H. W. (2000). Tax and transfer policy, and family formation: Marriage and cohabitation. Mimeo

Ellwood, D. (2000). The impact of the earned income tax credit and social policy reforms on work, marriage, and living arrangements. National Tax Journal, 54(4), 1063–1105.

Evans, W. N., & Garthwaite, C. L. (2010). Giving mom a break: The impact of higher EITC payments on maternal health. National Bureau of Economic Research Working Paper: 16296.

Fisher, H. (2013). The effect of marriage tax penalties and subsidies on marital status. Fiscal Studies, 34(4), 437–465.

Grogger, J., & Bronars, S. G. (2001). The effect of welfare payments on the marriage and fertility behavior of unwed mothers: Results from a twin experiment. Journal of Political Economy, 109(3), 529–545.

Herbst, C. M. (2011). The impact of the earned income tax credit on marriage and divorce: Evidence from flow data. Population Research Policy Review, 30(1), 101–128.

Internal Revenue Service. (2013). Qualifying child rules. http://www.irs.gov/Individuals/Qualifying-Child-Rules. Accessed 12 February 2013

Kearney, M. S., & Turner, L. J. (2013). Giving secondary earners a tax break: A proposal to help low- and middle-income families. The Hamilton Project Discussion Paper.

Kennedy, S., & Bumpass, L. (2011). Cohabitation and trends in the structure and stability of children’s family lives. Paper presented at the Annual Meeting of the Population Association of America, Washington, DC.

Kenney, C. (2004). Cohabiting couple, filing jointly? Resource pooling and U.S. poverty policies. Family Relations, 53, 237–247.

Lichter, D. T., Qian, Z., & Mellott, L. M. (2006). Marriage or dissolution? Union transitions among poor cohabiting women. Demography, 43(2), 223–240.

Meyer, B., & Rosenbaum, D. T. (2001). Welfare, the earned income tax credit, and the labor supply of single mothers. The Quarterly Journal of Economics, 116(3), 1063–1114.

Moffitt, R. A. (1998). The effect of welfare on marriage and fertility. In: Robert A. Moffitt (Ed.), Welfare, the family, and reproductive behavior: Research perspectives (p. 50). Washington DC: National Academies Press.

Oropesa, R. S., Landale, N. S., & Kenkre, T. (2003). Income allocation in marital and cohabiting unions: The case of mainland Puerto Ricans. Journal of Marriage and Family, 65(4), 910–926.

Smock, P. J., Manning, W. D., & Porter, M. (2005). Everything’s there except money: How money shapes decisions to marry among cohabitors. Journal of Marriage and Family, 67(3), 680–696.

Tach, Laura, & Halpern-Meekin, Sarah (2013). Tax code knowledge and behavioral responses among EITC recipients: Policy insights from qualitative data. Journal of Policy Analysis and Mangement, 33(2), 413–439.

Tax Policy Center. (2011). EITC, TANF, and food stamp participation rates, 1990–2004. Taxpolicycenter.org. http://www.taxpolicycenter.org/taxfacts/displayafact.cfm?Docid=273. Accessed 30 April 2011, http://www.taxpolicycenter.org/taxfacts/displayafact.cfm?Docid=36 Historical EITC parameters. Accessed 30 April 2011

Acknowledgments

The author would like to thank Michael Lovenheim, Kelly Musick, Sharon Sassler, and Laura Tach for helpful advice and comments. She would also like to acknowledge support from the Institute for Education Sciences on grant R305B110001. Any remaining errors are the author’s own.

Author information

Authors and Affiliations

Corresponding author

Ethics declarations

Conflict of interest

The authors declare that they have no conflict of interest.

Electronic supplementary material

Rights and permissions

About this article

Cite this article

Michelmore, K. The earned income tax credit and union formation: The impact of expected spouse earnings. Rev Econ Household 16, 377–406 (2018). https://doi.org/10.1007/s11150-016-9348-7

Received:

Accepted:

Published:

Issue Date:

DOI: https://doi.org/10.1007/s11150-016-9348-7