Abstract

In this paper we reconsider the degree of international comovement of inflation rates. We use a dynamic hierarchical factor model that is able to decompose Consumer Price Index (CPI) inflation in a panel of countries into (i) a factor common to all inflation series and all countries, (ii) a factor specific to a given sub-section of the CPI, (iii) a country group-factor and (iv) a country-specific component. With its pyramidal structure, the model allows for the possibility that the global factor affects the country-group factor and other subordinated factors but not vice versa. Using quarterly data for industrialized and emerging economies from 1996 to 2011 we find that about two thirds of overall inflation volatility is due to country-specific determinants. For CPI inflation net of food and energy, the global factor and the CPI basket-specific factor account for less than 20 % of inflation variation. Only energy price inflation in industrial economies is dominated by common factors.

Similar content being viewed by others

1 Introduction

Since the late 1990s, inflation in most economies is remarkably low and stable. At the same time, inflation rates appear highly synchronized across countries. This observation prompted researchers to argue that international inflation rates are in fact driven by economic forces common to all countries. Whether global inflation dynamics really show signs of being coupled to a global inflation cycle is subject to a number of recent empirical papers. Ciccarelli and Mojon (2010), among others, use a dynamic factor model to study the driving forces behind the apparent comovement of international inflation rates. Based on Consumer Price Index (CPI) data for 22 OECD countries over the period 1960-2008 they find that indeed almost 70 % of inflation variability is explained by just one common factor driving all inflation series. The remaining share of inflation volatility is due to country-specific determinants. The title of their paper is instructive: “global inflation”. Other papers such as Neely and Rapach (2011) and Mumtaz and Surico (2012), whose contributions will be sketched below, support this view. They even find an increase in the degree of international comovement in inflation since the 1980s.

In this paper, we use an alternative empirical model, a dynamic hierarchical factor model recently developed by Moench et al. (2013), to revisit the comovement of inflation over the period 1996-2011.Footnote 1 Our results are striking: rather than being driven by a single global factor, inflation is predominately explained by idiosyncratic determinants. According to our results, “local inflation” is a much better characterization of the evidence than “global inflation”.

How do we arrive at this conclusion? We use the dynamic hierarchical factor model that is able to decompose CPI inflation rates in a large panel of countries into (i) a global factor common to all inflation series and all countries, (ii) a factor specific to a given sub-section of the CPI, i.e. energy price inflation, food price inflation and CPI inflation net of food and energy items, (iii) a country group factor driving the particular CPI basket in either industrial or emerging economies and (iv) a country-specific component. With its pyramidal structure, the model allows for the possibility that the global factor affects the country-group factor and other subordinated factors but not vice versa. To illustrate this property of our model, consider the emergence of China as a major trading partner of almost all countries in our sample which affected inflation rates around the globe and would be reflected by the global factor. This effect, however, is different across CPI components. While increased competition from Chinese exports dampened core inflation, additional demand from Chinese households and firms might have accelerated global food and energy price inflation, respectively.Footnote 2 Hence, a change in the global factor has a differentiated impact on the alternative CPI type-specific factors. This cannot be captured by conventional dynamic factor models.

Using data for industrialized and emerging economies from 1996 to 2011 we establish three core findings: First, with the exception of energy price inflation, about three fourths of inflation volatility is due to country-specific determinants. For CPI inflation net of food and energy, often referred to as a measure of core inflation, the global factor and the factor specific to this CPI sub-basket account for 10 % of the variance in industrialized economies and for less than 1 % in emerging markets. Second, energy price inflation, at least in industrial economies, is indeed dominated by common factors. This suggests that the “global inflation”-findings of the literature mentioned before are an artifact of not allowing for energy price to be driven by a specific factor and the non-hierarchical structure of conventional dynamic factor models. Moreover, determinants specific to industrial or emerging market economies matter most for the dynamics of energy price inflation. Third, about 22 % (16 %) of the variance of food price inflation in industrial (emerging) economies is explained by the global food price factor. Again, however, the bulk of food price inflation is due to idiosyncratic driving forces. This is particularly interesting given recent concerns about accelerating food price inflation caused by “speculative” forces over which a single country has no control.

Our contribution is threefold.Footnote 3 First, we apply a novel factor model that explicitly takes account of the hierarchical structure of the data. This allows for global factors to affect CPI basket-specific, country group-specific as well as country-specific factors. The opposite, however, is not possible. Second, we split overall CPI inflation used in other studies into energy price inflation, food price inflation and inflation based on the remaining CPI items. Given the swings in energy and food prices seen over the last decade, it is not an innocuous assumption to restrict these series to be driven by one single global factor. Our model identifies a global energy price and a global food price factor that coexist with a global factor for the remaining CPI items. In our pyramidal structure, all three of these CPI basket-specific factors are potentially driven by a single world factor, while they can affect all subordinated economy group-specific factors belonging to a certain CPI type. Third, we assess whether the inclusion of the Great Recession since mid-2008 changes the pattern of international comovement.

Our results question the policy conclusions drawn by Ciccarelli and Mojon (2010) and others, who stress the role of monetary policy coordination for successfully stabilizing idiosyncratic inflation dynamics. In fact, the period between 1984 and 2007, also known as the Great Moderation, saw an unprecedented convergence towards a consensus view on monetary policy. According to this paradigm, monetary policy should aim at keeping inflation low and stable by appropriately steering the short-term nominal interest rate. Often this view was implemented by pursuing a medium-term numerical inflation objective. Although cross-country differences in the definition of price stability and the weights attached to conflicting policy objectives remained, the importance of stable prices was widely acknowledged. If there is less comovement in inflation than previously thought, either the monetary policy stance across countries was less homogenous or shocks were less global in nature than previously thought. Our results stress the primary responsibility of domestic monetary policy for controlling domestic inflation.

The remainder of this paper is organized as follows. Section 2 discusses the recent literature on international inflation dynamics in dynamic factor models. Section 3 introduces our dynamic hierarchical factor model and presents the data set. The main results are reported in Section 4. In Section 5 we analyze the robustness of our findings. The impact of the Great Recession on the synchronization of inflation rates is evaluated in Section 6. Section 7 concludes.

2 A Brief Review of the Related Literature

Recently, several papers elaborate on the international comovement of real and nominal variables. In this section we provide a selective review of the main contributions. As mentioned in the introduction, our paper adds to the debate about the degree of synchronization of inflation rates. Since we have to be silent on issues such as the convergence to a common level of inflation or the disinflation since the 1980s, we focus on this narrow strand of the literature here. As a matter of fact, there is an abundant literature on disinflation and convergence, respectively, mostly using sophisticated tests of the unit root properties of inflation.Footnote 4

With the development of the latest generation of dynamic factor models over the past decade an analysis of large panel data sets of macroeconomic variables became possible. Kose et al. 2003 and 2008 provide the first application of dynamic factor models to analyze the degree of international comovement of business cycles. While these early contributions focused on the international synchronization of real variables only, recent papers started to address also the comovement of inflation rates.

Borio and Filardo (2007) started this literature arguing that models of inflation determination neglect the increasing role of global determinants of domestic inflation. In a large cross-section of countries they show that measures of “global slack”, i.e. global inflationary pressure, add explanatory power to conventional Phillips curve-based inflation models.

Ciccarelli and Mojon (2010) collect data on CPI inflation for 22 OECD countries over the period 1960-2008. They establish an important finding that was later confirmed by others: almost 70 % of the variance in inflation is explained by a common factor. The authors devote the title of their paper to this “global inflation factor. The finding is striking as it implies either a large degree of synchronization of monetary policies or a dominant role for global shocks hitting individual economies simultaneously. In a second step, the authors show that the presence of a large common component improves the forecasting performance of augmented Phillips curve relations. Eickmeier and Pijnenburg (2013) study inflation in 24 OECD countries in a Phillips curve framework. The authors decompose the determinants of inflation, i.e. output gaps and changes in unit labour costs, into global and idiosyncratic components.

Based on annual data for 64 countries over the period 1950-2009, Neely and Rapach (2011) also point to an important role for world factors in the determination of inflation. In their model, which also allows for regional factors driving inflation, world and regional factors on average account for 35 and 16 %, respectively, of inflation variation. Thus, again less than 50 % of inflation variation is driven by country-specific factors. The authors also run a cross-sectional regression to relate the exposure to global, regional and country-specific factors to a set of explanatory variable such as openness, financial development and GDP per capita, among others. A subsample analysis reveals that the degree of comovement became even higher since 1980.

The latter point is supported by Mumtaz and Surico (2012), who estimate a time-varying dynamic factor model allowing for country-specific and common determinants of inflation. They find an increase in the comovement since the 1980s. In a companion paper, Mumtaz et al. (2011) develop that model further by including also a regional factor. Estimating the model over a long panel of real and nominal variables, the authors argue that the share of inflation variation due to the global factor has increased since 1985. Interestingly, they also find that since WWII the bulk of inflation volatility is driven by regional factors.

3 A Dynamic Hierarchical Factor Model for Inflation

We are interested in the common movements among CPI inflation rates, i.e. core inflation and the energy and food price components, across different countries. In general, a classical dynamic factor model is capable to extract latent variables and would thus be a tool applicable to analyze the synchronization between the different inflation series. One major shortcoming of the models used in the literature, however, is the absence of spillover effects from, say, global to regional factors or from global to CPI item-specific factors. Recent macroeconomic developments such as the flood of global liquidity, large fluctuations in energy and food prices, increased globalization of goods markets and financial markets and, above all, global shocks such as the 2008/09 financial crisis suggest that global forces should have an effect on subordinated factors within our factor model. Take the abundance of global liquidity as an example. This is mostly likely to be not only a common source of fluctuations in all inflation rates included in our sample, but will also have an effect on the behavior of the energy price inflation and food price inflation factor, respectively.

To address these issues, we use a dynamic hierarchical factor model developed by Moench et al. (2013). With its hierarchical structure of order four, we are able to obtain global, CPI subset-specific and country group-specific factors. At time t, let F t , G b t , and H b s t denote the factors that capture global inflation movements, fluctuations in the various CPI subsets (indexed by b) and variations common to country group s in CPI-specific block b, respectively. The pyramidal structure of the model states that

where Z b s n t represents an observation for country n in subblock s of block b at period t. For example, in 1999Q2 (t), France (n), belonging to the industrialized economies (s) category, declares its measured CPI for energy items (b). Λ Z b s n , Λ H b s and Λ G b are the constant factor loadings. Note that the total number of time series, N b s , can differ between blocks b and subblocks s.

The model is dynamic with regard to the global factor F t that is assumed to follow an AR(1) process

We restrict our model to one global component only, so that ρ F is a scalar. Furthermore, we make the following assumptions in order to match the persistence of the data

with \(\epsilon _{jt} \sim N\left (0,\sigma ^2_{j}\right )\) for j = Z b s n, H b s, G b, F. All residuals 𝜖 j t are uncorrelated across j and t. Henceforth, we refer to the 𝜖 j t error terms as idiosyncratic, country-group, CPI subset and global disturbances. For identification, the first entries of Λ i , i = Z b s, H b s, G b, are set to 1. This is sufficient since we restrict the number of factors to one on each stage and category. In addition, we fix the variances \(\sigma ^2_{Hbs}\), \(\sigma ^2_{Gb}\) and \(\sigma ^2_F\) to 0.1.Footnote 5

Since the dynamic hierarchical factor model formulates a vertical dependency of the factors as well as, thanks to Eqs. 5–7, a time-varying intercept, we rely on Markov Chain Monte Carlo methods in combination with Kalman filter techniques.Footnote 6 First, each factor is drawn based upon the parameters and all other variables, i.e. all other factors and, at the subblock level, the observations. Second, we draw the factor loadings, autoregressive parameters and subblock-level variances \(\sigma ^2_{Zbsn}\) given our factors determined in the first step. For our analysis we keep 1,000 draws (every 50th of 50,000 after a warm-up sample of 50,000 draws).Footnote 7

Equations 1–3 constitute a top-down approach to the factor estimates. For every factor, innovations will only affect factors on subordinated levels while factors at a higher level are independent from such disturbances. Putting it differently, spillover effects can only emerge from global events. An advantage over the approaches of Neely and Rapach (2011) and Mumtaz and Surico (2012), thus, is the explicit modeling of the asymmetric interdependencies between global and country-group factors and its explicit consideration in the estimation. Moreover, our model does not impose orthogonality among factors, which seems more natural than uncorrelated factors, e.g. CPI energy in industrialized or emerging countries are at least to some extent correlated with global inflation. Furthermore, the one-directional relationship within the model’s hierarchical structure offers the possibility to analyze the contribution of disturbances on different stages to the variance of a particular time series.

Our data consists of three different subsets of the overall CPI. First, we collect data on CPI net of food and energy items. The second set of series consists of the energy component of the CPI. The third set comprises the food component of the CPI. Hence, we do not include headline inflation but instead decompose CPI inflation in three subsets. For our empirical analysis the data is then split into two country-groups, industrialized and emerging economies. We use quarterly data ranging from 1996Q1 to 2011Q4. CPI indices are transformed into year-on-year inflation rates by taking the annual difference of the observations divided by last year’s price level. Using quarter-on-quarter inflation rates would entail excess volatility due to single deflation spikes in core CPI and other short-term shocks to energy and food price inflation such as wars in the Middle East or the SARS pandemic. Besides the elimination of this effect, we aim to work with year-on-year inflation rates since it is the measure monetary policy typically focuses on. Our effective estimation sample begins with the first observation in 1997Q1 and ends in 2011Q4. The data is taken from the FRED database of the Federal Reserve Bank of St. Louis. We augment this data set with CPI series provided by Thomson Financial Datastream (TFD). If not indicated otherwise, the source of a time series is FRED. All time series are normalized to have a mean of zero and a variance of unity.

Initially, we choose the following ordering for our factor analysis: on the block level we let CPI excluding food and energy be the first group, CPI energy the second and CPI food the last block. Regarding the subblock level, the group of industrialized countries comes before emerging economies. In Section 5 we check the impact of the specific type of ordering on our results.

We include relatively affluent countries only and have to exclude developing countries for which data was unavailable. This is unfortunate as the impact of global food and energy price shocks might be particularly severe for these countries. Table 1 provides the list of countries covered by the data set as well as the composition of the industrial economies and the emerging markets blocks. The appearance in Table 1 corresponds to the ordering in the estimation. Within the subblocks, the time series are ordered by the squared correlation with the highest correlation taking first rank. With this procedure we take into account a note in Moench et al. (2013), saying that the first series ought to be the most representative one. This is owed to the identification scheme as the first entries in the loading vectors are unity. In addition, this in combination with the rank order might also affect our overall estimation results since the block factor and global factor depend on the subblock factor estimates. For this reason, in Section 4 we present the results of combining all draws from twelve estimations with different orderings among block and subblock categories.

Our sample includes member countries of the European Monetary Union (EMU) for which a common monetary policy affects inflation. Nevertheless, we refrain from specifying a separate factor for those countries besides the factors driving inflation in industrial economies and emerging markets. The reasons for this are twofold: First, despite common monetary policy inflation dynamics in EMU countries were sufficiently heterogenous to subsume those countries in the industrial economies category. Second, allowing for a third group of countries would make each group too small to reasonably estimate the factor model.

The factor model presented before rests on the assumption of the data series being stationary. Whether or not inflation rates are stationary is subject to a large literature. Table 2 presents the numbers of stationary variables in our data set for different tests. The Augmented Dickey-Fuller test (ADF) clearly rejects the hypothesis under the null, i.e. that the time series have a unit-root, at both critical values. This statement remains regardless of the adopted lag structure. The Kwiatkowski-Phillips-Schmidt-Shin (KPSS) approach tests whether the observations are stationary. As opposed to ADF, KPSS is not so clear about stationarity. Although it shows some concerns about the data properties, it does not primarily classify the data as unit-root processes. As DeJong et al. (1992), Nelson et al. (2001), and Perron (1989), amongst others, point out, the tests have difficulties judging correctly near unit-root processes and structural instability, especially in rather short samples as in our case. Since we deal with international inflation rates which converged to relatively low and stable levels over the past 15 years, the trustworthiness of those tests for stationarity is at least doubtful.

A visual inspection of the data set, see Figs. 1, 2 and 3, confirms the impression of stable time series. For food and energy inflation we see a pattern that is similar to standard autoregressive processes. Taking the results and the asymptotic properties of the unit-root tests into account plus visually inspecting the data series, we think the requirement of stationary time series is met in our data set.

Data for CPI excluding food and energy

Data for CPI energy

Data for CPI food

4 Results

We start the interpretation of the results by examining the evolution of the extracted factors. Our factor estimates are shown in Figs. 4, 5 and 6. Plotted are median values over group means for all retained draws. The global factor, which is shown as a solid line in all three sets of figures, fluctuates moderately, peaks around the boom periods in the early 2000s and in 2007 but sharply drops eventually at the height of the recent financial crisis. We also see the brief deflationary episodes around 2009. Since then, the global factor quickly recovered.

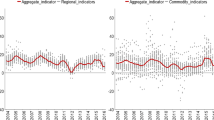

Decomposition of CPI excluding food and energy: benchmark hierarchical ordering. Depicted are estimated median values of global (solid lines), CPI subset (dashed) and country group (dotted) factors

Decomposition of CPI energy: benchmark hierarchical ordering. Depicted are estimated median values of global (solid lines), CPI subset (dashed) and country group (dotted) factors

Decomposition of CPI food: benchmark hierarchical ordering. Depicted are estimated median values of global (solid lines), CPI-specific (dashed) and market-specific (dotted) factors

Figure 4 shows the factor decomposition of core inflation. The core inflation factor is more volatile than the global factor but also peaks at the global boom periods mentioned before. While the factor specific to core inflation in industrial countries is the most volatile factor in this set of figures, the corresponding factor for emerging market economies is remarkably smooth. This reflects that emerging economies were hit less by the Great Recession than many industrial economies. The energy price factor, see Fig. 5, is much more volatile than the global factor. Accelerating global inflation was accompanied by a higher energy factor. Likewise, the sharp fall in the global factor went along with an even more drastic fall in the energy price factor. Surprisingly, in industrial economies the estimated energy factor varies more than in emerging markets.

The food price factor, see Fig. 6, is again much more volatile than the global factor and tracks the recent episodes of steeply rising food prices in 2010/11 after the crisis. Note also that the peaks of the food price factor become higher over time. Furthermore, while our energy factor moves in tandem with the global inflation factor, the estimated food factor lags the global factor.

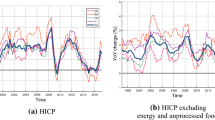

To highlight the close connection between the revealed factors and global developments, in Figs. 7 and 8 we plot our estimated factors against the global indices for prices of energy and food as provided by the International Monetary Fund (IMF) as a consistency check.Footnote 8 For energy, we observe a strong comovement between our factor and the IMF index, which is underlined by a correlation coefficient of 0.85. Throughout the sample, our estimate of the latent energy factor tracks the energy price index very well, even during the financial crisis and its aftermath. Our global food factor catches international developments in food prices quite well, albeit the synchronization between these two is not as excellent as it is for the energy series. We obtain a correlation coefficient of 0.62. Nevertheless, the factor captures the long trend in food price inflation preceeding the financial crisis and its strong decline afterwards as well as its recovery since.

Estimated CPI energy factor and IMF fuel (energy) price index. Depicted are the CPI energy factor (solid line) as well as the IMF Fuel (Energy) Price Index (dashed line)

Estimated CPI food factor and IMF food price index. Depicted are the CPI food factor (solid line) as well as the IMF Food Price Index (dashed line)

The relative role of the hierarchical factors can best be summarized in terms of the variance decomposition of inflation presented in Table 3, where we show for each inflation and each country group the fraction of volatility due to the global factor, the CPI basket-specific factor, the country group-specific factor and the idiosyncratic factor. We observe the following key findings:

First, with the exception of energy price inflation, inflation is predominantly driven by idiosyncratic factors. The share of variation of core inflation in industrial and emerging market economies, for example, due to local factors is 87 and 67 %, respectively. At the same time, the global factor is negligible with an explanatory power of at most 3.5 %. For emerging markets the country-group factor matters and explains 33 % of inflation volatility. Hence, the international comovement of core inflation, if any, is mostly due to country group-specific determinants but certainly not explained at a global level. The fact that the idiosyncratic factors, among them being domestic demand, matter most for core inflation might support the notion that central banks in small open economies should primarily be concerned with stabilizing inflation net of food and energy items. We discuss this issue again in the concluding section.

Second, energy price inflation, at least in industrial economies, is indeed dominated by common factors. The global factor and the energy factor together account for more than 50 % of inflation dynamics. Nevertheless, more than 30 % are still left to be explained at the idiosyncratic level. Moreover, determinants specific to industrial or emerging market economies matter most for the dynamics of energy price inflation. These findings suggest that the “global inflation”-findings of the literature mentioned before are an artifact of not allowing for energy prices to be driven by a separate factor. Here we clearly see that the determination of energy price inflation in industrial economies, the set of countries most other papers focus on, is indeed different from that of the remaining CPI components. For emerging economies, however, the group-specific factor is the second most important source of fluctuations in energy prices following idiosyncratic factors.

Third, about 22 % (16 %) of the variance of food price inflation in industrial (emerging) economies is explained by the global food price factor. Again, however, the largest fraction of food price inflation is due to idiosyncratic driving forces. This is particularly interesting given recent concerns about accelerating food price inflation caused by “speculative” forces over which a single country has no control. To our surprise, the explanatory power of the food inflation factor is larger for industrial than for emerging countries. With the share of expenditures on food being higher in emerging countries, the effect of the food price factor would certainly be more important if we were to consider inflation based on the total CPI.Footnote 9 For the food items considered here, however, the fact that emerging countries import fewer food products than industrial countries leads to a smaller role for the common food price factor. In addition, the pass-through from the global food price factor to domestic food price inflation becomes weaker if the country’s exchange rate appreciates against the U.S. dollar.Footnote 10

The methodology adopted in this paper allows us to generate counterfactual inflation dynamics for each country, i.e. the path of a particular inflation series that would have been observed had inflation only been driven by global, CPI-type or regional factors, respectively. To preserve space, Fig. 9 presents the counterfactual courses of inflation for selected countries only. We choose the U.S., France and Korea for that exercise. For each of these countries we provide counterfactual inflation dynamics for a different inflation rate.Footnote 11 The first panel shows counterfactual paths for core inflation in the U.S. economy. In the absence of idiosyncratic influences, i.e. with either global, regional or CPI subset-specific factors, U.S. core inflation would have been much smoother. A different pattern emerges for the case of France in the second panel. French energy price inflation would have been similar to the actual outcome had inflation been driven only by regional or CPI-type factors. Put differently, idiosyncratic influences played a negligible role in this case. Finally, the third panel provides the counterfactual paths for Korean food price inflation. Again the picture reveals the dominant role of a large idiosyncratic component. The global food price factor seems to lead Korean food price inflation, at least in the second half of the sample. Taken together, these selected case studies underline the overall findings discussed before.

Actual and counterfactual inflation for selected countries. The figures show series for the actual normalized data (solid green line) as well as for the counterfactual courses implied by the global factor (dashdot black line), CPI subset factors (dashed black line) and regional factors (solid black line)

5 Robustness

The results presented so far may be an artifact of the specific ordering of the groups on the block and subblock level of our model. Remember the restrictions on the vector of loadings, i.e. the first entry is set to unity. Besides the covariance matrix of the idiosyncratic components, this in turn affects our factor estimates since the first factor will inevitably exhibit characteristics of the time series in the first rank within each subblock. Even though this circumstance shapes our estimated factors and the analysis, it is necessary to make assumptions regarding the matrices of a factor model in order to identify factors and factor loadings.

The question is whether our findings are robust to different assumptions regarding the rank order of the series. For this reason, we not only present results for one particular ordering, but also investigate whether a pool of twelve different specifications yields similar results. We do so by estimating the factors with all twelve possible combinations of the CPI subsets (six combinations) and then letting in all subblocks either industrialized or emerging economies rank first (two combinations). The procedure is the same as for the benchmark ordering, i.e. we end up with 1,000 retained draws for each of the twelve variations, resulting in a set of 12,000 draws overall left for further analyses.

When looking at Figs. 10, 11 and 12, the factor estimates are similar to the ones obtained when applying our benchmark ordering (Figs. 4–6). All time series show the same pattern, supporting the robustness of our results for the chosen rank of categories. As expected, the factors belonging to the categories ordered first, i.e. core inflation and global CPI, differ from our benchmark specification. While the global factor changes only slightly, strengthening the contemporary inflationary pressure during the boom before the financial crisis, the factor measuring international core inflation displays more strongly the persistent decline in core inflation around the globe.

Decomposition of CPI excluding food and energy: all hierarchical orderings. Depicted are estimated median values of global (solid lines), CPI subset (dashed) and country group (dotted) factors

Decomposition of CPI energy: all hierarchical orderings. Depicted are estimated median values of global (solid lines), CPI-specific (dashed) and market-specific (dotted) factors

Decomposition of CPI food: all hierarchical orderings. Depicted are estimated median values of global (solid lines), CPI-specific (dashed) and market-specific (dotted) factors

Regarding the variance decomposition, a rotation of the ordering does not affect our main qualitative results, see Table 4. The idiosyncratic component is still the dominant part. In fact, most variance shares are affected very little by the alternative specifications. Remarkable differences occur for the country group factors, whose relative shares change a bit, and the overall influence of the global factors on CPI net of food and energy. None of these changes, however, compromises our main findings of “local inflation”.

6 The Impact of the Great Recession

The recent financial crisis in 2008 and the subsequent global recession hit several industrial economies at the same time. Thus, it is likely that these events strengthened the comovement of inflation rates. Put differently, without the occurrence of the Great Recession the synchronization of inflation might even be smaller than suggested by the results presented before. To isolate the effect of the crisis, we estimate the model again but exclude the period after 2008Q3, i.e. we truncate the sample immediately after the Lehman collapse in September 2008. The results for the pre-crisis sample are reported in Table 5.

Our main conjecture is confirmed for industrial economies: Whereas in the full sample 87 % of the volatility of core inflation in industrial economies is due to idiosyncratic factors, this number increases to 91 % in the pre-crisis sample. Thus, the Great Recession biases our estimates of the explanatory power of the idiosyncratic factor downwards. Without the Great Recession, the evidence would be even more in favor of our “local inflation” interpretation of international inflation dynamics.

For emerging markets, however, excluding the Great Recession reduces the variance share explained by idiosyncratic factors while at the same time the share of the emerging markets-factor increases. This supports the notion of a mild “decoupling” of emerging economies from development in mature economies during the financial crisis. In addition, the global factor is more relevant for fluctuations in our CPI series during the Great Moderation (averaged variance share of 7.8 %) prior to 2008 than it is in the sample with the recent financial turmoil (5.2 %).

Finally, the relevance of the energy and core price factors declines when we shorten the sample, reflecting the pronounced swings in energy prices over the course of the financial crisis since 2008. The relevance of the food price factor strongly increases in the truncated sample.

Taken together, the results from the shorter sample confirm our main findings. The explanatory shares for food and energy price inflation shift across factors, while core inflation seems to be even better described as “local inflation”.

7 Conclusions

In this paper we reconsidered the nature of comovement of international inflation rates. An estimated dynamic hierarchical factor model showed that the bulk of inflation dynamics can be attributed to idiosyncratic, i.e. country- and basket-specific, determinants. Global factors play only a minor role in the determination of individual inflation rates. This holds for CPI inflation rates net of food and energy prices as well as the individual food and energy price inflation series. Although global factors play a larger role for food and energy prices than for the prices of all other CPI items, their overall role is still limited. This stands in stark contrast to the existing literature whose consensus view is reflected in Ciccarelli and Mojon (2010) “global inflation” paper. Our findings, instead, support the notion of inflation being “local inflation” rather than “global inflation”.

If inflation is predominantly a local phenomenon, the case for international monetary coordination appears less compelling. While Ciccarelli and Mojon (2010) stress the benefits of coordination, the results presented here suggest that the monetary authorities covered by our sample have been successful in shielding the economies from global inflation spillovers.

A number of potential explanations might be behind the divergence of our findings from the literature. First, shocks hitting the economies could have been less common across countries than previously thought. Second, compared to other contributions to the literature our study focuses on a fairly recent sample period in which a larger share of countries allowed the exchange rate to float. A floating exchange rate should better insulate the economies from international inflation spillovers. To assess these competing interpretations a structural model would be needed, which goes beyond the scope of this paper and is left for future research.

The results are also important for the design of monetary policy.Footnote 12 While many countries included in our sample follow an inflation targeting strategy for monetary policy,Footnote 13 they did not reach a consensus about the appropriate definition of specific inflation rate to be targeted. While some central banks, e.g. the Bank of Thailand, specify the inflation target in terms of a measure of core inflation that typically excludes food and energy prices, others, most notably the Bank of England and many other central banks in advanced economies, focus on headline inflation. The “local inflation” finding, however, does not necessarily endorse targeting core inflation. Koech and Wynne (2013) study forecasting models for core import price inflation. Our result suggests that variables reflecting domestic conditons might have more predictive power for overall inflation than global variables. Only if monetary policy enjoys sufficient credibility to contain second-round effects of food and energy price shocks on domestic prices a narrowly defined inflation target might be preferable.Footnote 14 If this condition is not met, targeting a broader inflation measure might still be welfare-superior despite the bulk of inflation being determined locally.Footnote 15 Nevertheless, the results presented here strongly support the use of core inflation as an indicator of underlying inflationary pressure.

Notes

The dynamic hierarchical factor model is employed by Moench and Ng (2011) and Förster et al. (2012) for an analysis of the dynamics in the U.S. housing market and the comovement of international capital flows, respectively, and serves our needs for an investigation into international inflation comovement best.

For the effects of the emergence of China on commodity price dynamics see Roache (2012). Auer and Fischer (2010) investigate the impact of import competition from China on U.S. inflation rates. The recent study by Eickmeier and Kühnlenz (2013) evaluates the role of Chinese supply and demand shocks for global inflation dynamics.

Note that this paper focuses on the comovement of inflation, not on the global disinflation or the convergence of inflation, which is a separate literature. Since we use demeaned data, we have to be silent on the level of inflation series and, hence, cannot add to explaining the global fall in inflation after since the early 1980s.

Robustness exercises showed that the results do not change when we set the variance to different values.

Moench et al. (2013) provide a full description of the specific Markov Chain Monte Carlo approach as well as the application of the filter method.

The estimation of the dynamic hierarchical factor model is carried out with the help of the MATLAB codes from Serena Ng’s website.

We use data from the IMF about primary commodity prices, namely the Food Price Index (PFOOD_Index) and the Fuel (Energy) Index (PNRG_Index), available on the IMF’s website, http://www.imf.org/external/np/res/commod/index.aspx.

According to the International Monetary Fund (2011), the median food share in advanced economies’ CPI is only 17 %, whereas in emerging economies the median is 31 %.

Jongwanich and Park (2011) show a limited pass-through from food and oil price shocks to domestic CPI inflation in Asia. They argue that government subsidies, tariffs and price controls might be responsible for that finding.

See De Gregorio (2012) for a review of the key issues in the design of monetary policy in the presence of commodity price inflation.

Most countries in our sample indeed target inflation. They are either officially claiming to be inflation targeters, adopted an inflation target (e.g. the Federal Reserve, the ECB, Switzerland) or de facto aim at keeping inflation stable (e.g. Malaysia). The only exceptions are probably Japan and Singapore.

Cecchetti and Moessner (2008) argue that core inflation has not tended to revert to headline inflation suggesting that second-round effects are absent.

Catão and Chang (2010) use an open-economy sticky-price model to show that broad CPI targeting is welfare superior to alternative policies since CPI targeting also partly stabilizes real exchange rate fluctuations and thus helps stabilizing consumption.

References

Auer R, Fischer AM (2010) The effect of low-wage import competition on U.S. inflationary pressure. J Monet Econ 57(4):491–503. doi:10.1016/j.jmoneco.2010.02.007. http://www.sciencedirect.com/science/article/pii/S030439321000019X

Borio CEV, Filardo A (2007) Globalisation and inflation: New cross-country evidence on the global determinants of domestic inflation. BIS Working Paper No. 227, Bank for International Settlements. http://ideas.repec.org/p/bis/biswps/227.html

Busetti F, Fabiani S, Harvey A (2006) Convergence of prices and rates of inflation*. Oxf Bull Econ Stat 68:863–877. doi:10.1111/j.1468-0084.2006.00460.x

Catão L, Chang R (2010) World food prices and monetary policy. IMF Working Paper 10/161, International Monetary Fund

Cecchetti SG, Moessner R (2008) Commodity prices and inflation dynamics. BIS Q Rev:55–66. http://ideas.repec.org/a/bis/bisqtr/0812f.html

Ciccarelli M, Mojon B (2010) Global inflation. Rev Econ Stat 92(3):524–535

De Gregorio J (2012) Commodity prices, monetary policy and inflation. Unpublished manuscript, Universidad de Chile

DeJong DN, Nankervis JC, Savin NE, Whiteman CH (1992) Integration versus trend stationary in time series. Econometrica 60(2):423–433. http://www.jstor.org/stable/2951602

Eickmeier S, Kühnlenz M (2013) China’s role in global inflation dynamics. Deutsche Bundesbank Discussion Paper No. 07/2013, Deutsche Bundesbank

Eickmeier S, Pijnenburg K (2013) The global dimension of inflation evidence from factor-augmented phillips curves. Oxf Bull Econ Stat 75(1):103–122. doi:10.1111/obes.12004

Förster M, Jorra M, Tillmann P (2012) The dynamics of international capital flows: results from a dynamic hierarchical factor model. MAGKS Discussion Papers on Economics No. 21-2012, Philipps-Universitt Marburg

International Monetary Fund (2011) World economic outlook September 2011 – target what you can hit: commodity price swings and monetary policy http://www.imf.org/external/pubs/ft/weo/2011/01/index.htm

Jongwanich J, Park D (2011) Inflation in developing asia: pass-through from global food and oil price shocks. Asian-Pac Econ Lit 25(1):79–92. 10.1111/j.1467-8411.2011.01275.x

Koech J, Wynne M (2013) Core import price inflation in the United States. Open Econ Rev 24(4):717–730. doi:10.1007/s11079-012-9264-2

Kose MA, Otrok C, Whiteman CH (2003) International business cycles: world, region, and country-specific factors. Am Econ Rev 93(4):1216–1239. http://www.jstor.org/stable/3132286

Kose MA, Otrok C, Whiteman CH (2008) Understanding the evolution of world business cycles. J Int Econ 75(1):110–130

Moench E, Ng S (2011) A hierarchical factor analysis of u.s. housing market dynamics. Econ J 14(1):C1–C24. doi:10.1111/j.1368-423X.2010.00319.x

Moench E, Ng S, Potter S (2013) Dynamic hierarchical factor models. Rev Econ Stat 95(5):1811–1817

Mumtaz H, Surico P (2012) Evolving international inflation dynamics: World and country-specific factors. J Eur Econ Assoc 10(4):716–734. http://ideas.repec.org/a/bla/jeurec/v10y2012i4p716-734.html

Mumtaz H, Simonelli S, Surico P (2011) International comovements, business cycle and inflation: a historical perspective. Rev Econ Dyn 14(1):176–198. http://ideas.repec.org/a/red/issued/09-235.html

Neely CJ, Rapach DE (2011) International comovements in inflation rates and country characteristics. J Int Money Financ 30(7):1471–1490. doi:10.1016/j.jimonfin.2011.07.009. http://www.sciencedirect.com/science/article/pii/S0261560611001148

Nelson CR, Piger J, Zivot E (2001) Markov regime switching and unit-root tests. J Bus Econ Stat 19(4):404–415. doi:10.1198/07350010152596655. http://www.tandfonline.com

Perron P (1989) The great crash, the oil price shock, and the unit root hypothesis. Econometrica 57(6):1361–1401. http://www.jstor.org/stable/1913712

Roache SK (2012) China’s impact on world commodity markets. IMF Working Paper 12/115, International Monetary Fund. http://ideas.repec.org/p/imf/imfwpa/12-115.html

Rogoff K (2003) Globalization and global disinflation. Monetary policy and uncertainity: adapting to a changing economy, Federal Reserve Bank of Kansas City

Acknowledgments

We thank the editor and two anonymous referees for very helpful comments.

Author information

Authors and Affiliations

Corresponding author

Rights and permissions

About this article

Cite this article

Förster, M., Tillmann, P. Reconsidering the International Comovement of Inflation. Open Econ Rev 25, 841–863 (2014). https://doi.org/10.1007/s11079-014-9312-1

Published:

Issue Date:

DOI: https://doi.org/10.1007/s11079-014-9312-1