Abstract

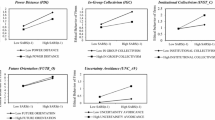

The International Federation of Accountants (IFAC) has issued a revised “Code of Ethics for Professional Accountants” (IFAC Code). The IFAC Code is intended to be a model code of ethics for national accounting organizations throughout the world. Prior research demonstrates that approximately 50% of IFAC member organizations have adopted the IFAC Code as their organizational code of conduct. There is therefore empirical evidence that international convergence of accounting ethical standards is occurring. We employ Hofstede’s (2008, http://www.geert-hofstede.com/hofstede_dimensions.php) cultural dimensions in an attempt to empirically explain accounting organizations’ decisions about whether to adopt the IFAC Code or to retain their organization-specific code. Our results indicate that accounting organizations in cultures with high levels of Individualism and Uncertainty Avoidance are less likely to adopt the model IFAC Code. Organizations in high Individualism and Uncertainty Avoidance societies are therefore less likely to surrender the setting of ethical standards to an outside, international organization.

Similar content being viewed by others

References

Arnold, D., Bernardi, R., Neidermeyer, P. and J. Schmee: 2006, ‘The Effect of Country and Culture on Perceptions of Appropriate Ethical Actions Prescribed by Codes of Conduct: A Western European Perspective among Accountants’, Journal of Business Ethics 70(4), 327-340.

Clements, C., J. Neill and O. Stovall: 2009, ‘An Analysis of International Accounting Codes of Conduct’, Journal of Business Ethics 87(Suppl. 1), 173–183.

Cohen, J., Pant, L. and D. Sharp: 1992, ‘Cultural and Socioeconomic Constraints on International Codes of Ethics: Lessons from Accounting’, Journal of Business Ethics 11(9), 687-700.

Farrell, B. and D. Cobbin: 2000, ‘A Content Analysis of Codes of Ethics from Fifty-seven National Accounting Organizations’, Business Ethics: A European Review 9(3), 180-190.

Hofstede, G.: 1980, Culture’s Consequences (Sage Publications, Beverly Hills, CA).

Hofstede, G.: 2008, ‘Geert Hofstede Cultural Dimenstions’, http://www.geert-hofstede.com/hofstede_dimensions.php.

Hofstede, G. and G. J. Hofstede: 2005, Cultures and Organizations, (McGraw-Hill: New York).

IFAC: 2005, ‘Code of Ethics for Professional Accountants’, http://www.ifac.org/Members/Downloads/2005_Code_of_Ethics.pdf.

IFAC: 2008, ‘Responses to the Member Body Compliance Program’, http://www.ifac.org/ComplianceAssessment/published_surveys.php.

Rallapalli, K.: 1999, “‘A Paradigm for Development and Promulgation of a Global Code of Marketing Ethics’, Journal of Business Ethics 18(1), 125-137.

Stovall, O., Neill, J. and Reid B.: 2006, ‘Institutional Impediments to Voluntary Ethics Measurement Systems’, Journal of Business Ethics 66(2/3), 169-175.

Vitell, S., Nwachukwu, S. and J. Barnes: 1993, ‘The Effects of Culture on Ethical Decision- Making: An Application of Hofstede’s Typology’, Journal of Business Ethics 12(10), 753-760.

Williams, G. and J. Zinkin: 2008, ‘The Effect of Culture on Consumers’ Willingness to Punish Irresponsible Corporate Behaviour: Applying Hofstede’s Typology to the Punishment Aspect of Corporate Social Responsibility’, Business Ethics: A European Review 17(2), 210-226.

Author information

Authors and Affiliations

Corresponding author

Rights and permissions

About this article

Cite this article

Clements, C.E., Neill, J.D. & Stovall, O.S. The Impact of Cultural Differences on the Convergence of International Accounting Codes of Ethics. J Bus Ethics 90 (Suppl 3), 383–391 (2009). https://doi.org/10.1007/s10551-010-0417-1

Published:

Issue Date:

DOI: https://doi.org/10.1007/s10551-010-0417-1