Abstract

The present work aims at contributing to the recent stream of literature which attempts to link the Neo-Schumpeterian/Evolutionary and the Post-Keynesian theory. The paper adopts the Post-Keynesian Stock Flow Consistent modeling approach to analyze the process of development triggered by the emergence of a new-innovative productive sector into the economic system. The model depicts a multi-sectorial economy composed of consumption and capital goods industries, a banking sector and two households sectors: capitalists and wage earners. Furthermore, it provides an explicit representation of the stock market. In line with the Schumpeterian tradition, our work highlights the cyclical nature of the development process and stresses the relevance of the finance-innovation nexus, analyzing the feed-back effects between the real and financial sides of the economic system. In this way we aim at setting the basis of a comprehensive and coherent framework to study the relationship between technological change, demand and finance along the structural change process triggered by technological innovation.

Similar content being viewed by others

Notes

Schumpeter in fact argued that ”the carrying into effect of an innovation involves, not primarily an increase in existing factors of production, but the shifting of existing factors from old to new uses” (Schumpeter 1964/1939, p.110). Production of the innovative good takes time to come into effect. Hence the first effect of the appearance of entrepreneurial demand is an increase in the demand for traditional capital goods.

We adopt the convention of using capital letters to refer to nominal variables and lowercase letters for real variables.

Following Foley (1975) and many PK-SFC authors, the level of financial assets held might not be equal to their desired level, due to discrepancies between expected income, on which consumption is based, and actual income. We thus need one asset which will absorb the difference between aggregate level and aggregate desired level. In our model, as in most PK-SFC models, cash is the buffer stock asset.

In the model, we fix only λ 10 while λ 20,λ 30,λ 40 are endogenously determined, each one being defined equal to the ratio between the potential output of the related sector and total potential output. Hence, these parameters roughly reflect the changing weight of each industry on the whole economy. Furthermore, in order to satisfy the horizontal adding-up constraints on the 4 × 4 matrix of coefficients λ 11 to λ 44, we adopt a more stringent symmetry constraint (see Godley and Lavoie 2007, p. 145).

In fact, the overall capital stock of the innovative sector includes both kinds of capital, till the stock of traditional capital bought when entering the market depreciated.

Since firms invest in both capital goods, rr l,x is defined as the nominal interest rate r l,x deflated by capital price inflation.

For an extended review of the empirical literature in this field, see Lazonick et al. (2010).

We follow Bhaduri (1972) and use a non-linear depreciation function: d(k,t) = k e (t−n).

Indeed, contrary to most mainstream works in which money is exogenous and credit is conceived as a multiplier of deposits (i.e., of money already in the system), the theory of endogenous money argues that money is created ex novo by the banking sector, dependent on demand for credit coming from the economy. This new amount of monetary means must ends up in a rise of deposits so that the reversal causal link “loans make deposits” holds. See Graziani (2003)

Of course, the opposite choice could affect the results of the simulations, as the emergence of entrepreneurs could exert a different initial impact on the demand of each sector, and thus on employment, wealth and stock market prices. However, notice that in order to investigate such a case, we would only have to change our assumption concerning the initial finance of the innovative sector, while the model’s structure and behavioral equations would remain unaffected.

The innovative firms use both type of capital until the traditional capital bought in the first period of their life is fully depreciated.

This is a standard result of a pure credit money system like the one described in our model (Graziani 2003).

The product of the leverage ratio for the real interest rate charged on loans is roughly constant in this phase and thus plays a minor role.

This assumption is very reasonable since the innovative sector, when entering the market, used only bank credit to buy its initial stock of capital and to hire workers. Consequently, its leverage ratio was initially equal to one, by far the highest in the system (almost five times that of other sectors).

It is interesting to note that in these three cases, the preferences of the innovative sectors move from external equity finance to bank loans as a consequence of the gradual reduction in the interest rate charged by banks.

The interest rate increases by approximately 40 % compared to that charged at steady state, while the leverage ratio increases up to ten times between period 100 and period 153.

Capitalists consumption does not fall at once since it is a function of wealth (which remains positive) and of expected disposable income (defined as the average of disposable income over the last 4 periods). Consumption remains thus roughly constant in period 153 and shrinks only in the following periods.

Or rather, the consumption sector q converges to its original value, the innovative sector Tobin’s q converges to the original value of the traditional capital sector.

Remember that, since we adopted an exponential depreciation function over 20 periods, rather than a less realistic linear one, the portion of capital depreciating in each period is exponentially increasing with its age.

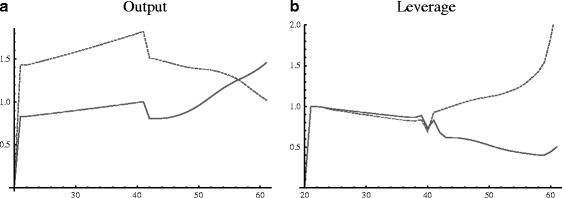

Fig. 5

a - Innovative sector output and b - leverage in the Baseline (solid) and BaF (dashed) scenarios

References

Aghion P, Howitt PW (2009) The economics of growth. The MIT Press, Cambridge

Bhaduri A (1972) Unwanted amortisation funds. Econ J 82(326):674–677

Brainard WC, Tobin J (1968) Am Econ Rev 58(2):99–122

Brown JR, Fazzari SM, Petersen BC (2009) Financing innovation and growth: cash flow, external Equity, and the 1990s R&D boom. J Finance 64(1):151–185

Brown JR, Petersen B (2009) Why has the investment-cash flow sensitivity declined so sharply? rising r&d and equity market developments. J Bank Finance 33-5:971–984

Castellacci F (2008) Innovation and the competitiveness of industries: comparing the mainstream and the evolutionary approaches. Technol Forecast Soc Chang 75(7):984–1006

Caverzasi E, Godin A (2013) Stock-flow consistent modeling trough the ages. Working Papers 745, Levy Economics Institute of Bard Callege

Ciarli T, Lorentz A, Savona M, Valente M (2010) The effect of consumption and production structure growth and distribution. A micro to macro model. Metroeconomica 61(1):180–218

Dosi G (1982) Technological paradigms and technological trajectories: a suggested interpretation of the determinants and directions of technical change. Res Policy 11(3):147–162

Dosi G (1990) Finance, innovation and industrial change. J Econ Behav Organ 13(3)

Dosi G, Fagiolo G, Napoletano M, Roventini A (2013) Income distribution, credit and fiscal policies in an agent-based keynesian model. J Econ Dyn Control 37-8:1598–1625

Dosi G, Fagiolo G, Roventini A (2010) Schumpeter meeting keynes: a policy-friendly model of endogenous growth and business cycles. J Econ Dyn Control 34(9):1748–1767

Farmer J, Geanakoplos J (2009) The virtues and vices of equilibrium and the future of financial economics. Complexity 14-3:11–38

Foley D (1975) On two specifications of asset equilibrium in macroeconomic models. J Polit Econ 83-2(2):303–324

Freeman C, Perez C (1988) Structural crises of adjustment, business cycles and investment behaviour. In: Dosi G, Freeman C, Nelson R, Silverberg G, Soete L (eds) Technical change and economic theory. Pinter, London and New York, pp 38–66

Godley W, Lavoie M (2007) Monetary economics an integrated approach to credit, money, income, production and wealth. Palgrave MacMillan, New York

Graziani A (2003) The monetary theory of production. Cambridge University Press, Cambridge

Greenwald BC, Stiglitz JE (1993) Financial market imperfections and business cycles. Q J Econ 108(1):77–114

Hakim C (1989) Identifying fast growth small firms. Employment Gazette 27:29–41

Hubbard R (1998) Capital-market imperfections and investment. J Econ Lit 36-1:193–225

Jarvis R (2000) Finance and the small firm. In: Carter S, Jones-Evans D (eds) Enterprise and small business: principles, practice and policy. FT Prentice Hall

King R, Levine R (1993a) Finance and growth: Schumpeter might be right. Q J Econ 108:717–738

King R, Levine R (1993b) Finance, entrepreneurship, and growth: Theory and evidence. J Monet Econ 32:513–542

King RG, Rebelo ST (1999) Resuscitating real business cycles. Handb Macroecon 1:927–1007

Lavoie M (1992) Foundations of Post-Keynesian economic analysis. Edward Elgar, Aldershot

Lazonick W, Mazzucato M, Nightingale P, Parris S (2010) Finance, innovation & growth - state of art report. Finnov Discussion Paper 1.6:44

Le Heron E, Rochon L-P, Olawoye SY (2012) Financial crisis, state of confidence and economic policies in a post-keynesian stock-flow consistent model Monetary policy and central banking - new directions in post-keynesian theory. Edward Elgar

Levine R (2005) Finance an growth: theory and evidence. In: Aghion P, Durlauf SN (eds) Handbook of economic growth. Elsevier

Mankiw NG, Romer DH (1991) New Keynesian economics, vol 2. MIT press, Cambridge

Mayer G (1990) Financial systems, corporate finance, and economic development. In: Hubbard R (ed) Asymmetric information, corporate finance, and investment. University of Chicago Press

Mazzucato M (2003) Risk, variety and volatility: growth, innovation and stock prices in early industry evolution. J Evol Econ 13:491–512

Meyers S (1984) Capital structure puzzle. J Finance 39-3:575–592

Mina A, Lahr H, Hughes A (2011) The demand and supply of external finance for innovative firms. Finnov Discussion Paper 3.5:39

Nelson R, Winter SG (1982) An evolutionary theory of economic change. Harvard University Press, Cambridge

Pastor L, Veronesi P (2009) Technological revolutions and stock prices. Am Econ Rev 99-4:1451–1483

Perez C (2002) Technological revolutions and financial capital: the dynamics of bubbles and golden Ages. Elgar, Cheltenham

Perez C (2009) The double bubble at the turn of the century: technological roots and structural implications. Camb J Econ 33-4(4):779–805

Perez C (2010) Technological revolutions and techno-economic paradigms. Camb J Econ 34-1:185–202

Russo A, Catalano M, Gaffeo E, Gallegati M, Napoletano M (2007) Industrial dynamics, fiscal policy and r&d: Evidence from a computational experiment. J Econ Behav Organ 64(3):426–447

Saviotti PP, Pyka A (2004) Economic development by the creation of new sectors. J Evol Econ 14(1):1–35

Saviotti PP, Pyka A (2008) Product variety, competition and economic growth. J Evol Econ 18(3):323–347

Schumpeter JA (1912) The theory of economic development. Harvard University Press, Cambridge, MA

Schumpeter JA (1939) Business cycle. A theoretical, historical and statistical analysis of the capitalist process. Abridged Edn., McGraw Hill, New York

Stadler GW (1994) Real business cycles. J Econ Lit 32(4):1750–1783

van Treeck T (2009) A synthetic, stock-flow consistent macroeconomic model of Financialisation. Camb J Econ 33(3):467–493

Verspagen B (2002) Evolutionary macroeconomics: a synthesis between neo-schumpeterian and post-keynesian lines of thought. The Electronic Journal of Evolutionary Modeling and Economic Dynamics, p 1007

Vos E, Yeh Y, Carter S, Tagg S (2007) The happy story of small business financing. J Bank Finance 31-9:2648–2672

Zezza G (2008) U.S. Growth, the housing market, and the distribution of income. J Post Keynesian Econ 30(3):375–401

Author information

Authors and Affiliations

Corresponding author

Additional information

We want to thank Carlota Perez, Domenico Delli Gatti, Roberto Fontana, Gennaro Zezza and an anonymous referee for their valuable comments. All remaining errors are ours.

Appendix: Parameters

Appendix: Parameters

Rights and permissions

About this article

Cite this article

Caiani, A., Godin, A. & Lucarelli, S. Innovation and finance: a stock flow consistent analysis of great surges of development. J Evol Econ 24, 421–448 (2014). https://doi.org/10.1007/s00191-014-0346-8

Published:

Issue Date:

DOI: https://doi.org/10.1007/s00191-014-0346-8