Summary

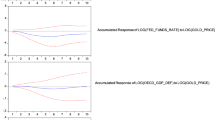

This paper estimates the response of consumer prices to a monetary policy shock in Switzerland. We find that there is no evidence of a price puzzle at the aggregate level. This is because our factor-augmented vector autoregression (FAVAR) avoids misspecification by including more information than a traditional VAR. However, the response is still delayed by at least four quarters, partly because there is a price puzzle in some sectors. In particular, rents tend to rise after a monetary policy tightening because there are legal provisions in Switzerland which link them to interest rates. But durable goods prices also rise, which is consistent with the existence of a cost channel of monetary policy.

Article PDF

Similar content being viewed by others

References

Assenmacher-Wesche, Katrin (2008), “Modeling Monetary Transmission in Switzerland with a Structural Cointegrated VAR Model”, Swiss Journal of Economics and Statistics, 144(2), pp. 197–246.

Bai, Jushan, and Serena Ng (2002), “Determining the Number of Factors in Approximate Factor Models”, Econometrica, 70(1), pp. 191–221.

Bai, Jushan, and Serena Ng (2004), “Confidence Intervals for Diffusion Index Forecasts with a Large Number of Predictors”, Mimeo.

Barth, Marvin J., and Valerie A. Ramey (2002), “The Cost Channel of Monetary Transmission”, in NBER Macroeconomics Annual, Ben S. Bernanke and Kenneth Rogoff, eds, vol. 16, chap. 4, pp. 199–256, Cambridge: MIT Press.

Bernanke, Ben, Jean Boivin and Piotr S. Eliasz (2005), “Measuring the Effects of Monetary Policy: A Factor-Augmented Vector Autoregressive (FAVAR) Approach”, The Quarterly Journal of Economics, 120(1), pp. 387–422.

Boivin, Jean, Marc P. Giannoni and Ilian Mihov (2009), “Sticky Prices and Monetary Policy: Evidence from Disaggregated US Data”, American Economic Review, 99(1), pp. 350–384.

Castelnuovo, Efrem, and Paolo Surico (2010), “Monetary Policy, Inflation Expectations and the Price Puzzle”, The Economic Journal, 120(549), pp. 1262–1283.

Chowdhury, Ibrahim, Mathias Hoffmann, and Andreas Schabert (2006), “Inflation Dynamics and the Cost Channel of Monetary Transmission”, European Economic Review, 50(4), pp. 995–1016.

Dickey, David A., and Wayne A. Fuller (1979), “Distribution of the Estimators for Autoregressive Time Series with a Unit Root”, Journal of the American Statistical Association, 74(366), pp. 427–431.

Eichenbaum, Martin (1992), “‘Interpreting the Macroeconomic Time Series Facts: The Effects Of Monetary Policy’: by Christopher Sims”, European Economic Review, 36(5), pp. 1001–1011.

Giordani, Paolo (2004), “An Alternative Explanation of the Price Puzzle”, Journal of Monetary Economics, 51(6), pp. 1271–1296.

Hamilton, James D. (1994), Time Series Analysis, Princeton: Princeton University Press.

Henzel, Steffen, Oliver Hülsewig, Eric Mayer and Timo Wollmershäuser (2009), “The Price Puzzle Revisited: Can the Cost Channel Explain a Rise in Inflation after a Monetary Policy Shock?”, Journal of Macroeconomics, 31(2), pp. 268–289.

Jordan, Thomas J., Michel Peytrignet and Enzo Rossi (2010), “Ten Years’ Experience with the Swiss National Bank’s Monetary Policy Strategy”, Swiss Journal of Economics and Statistics, 146(1), pp. 9–90.

Kaufmann, Daniel (2009), “Price-Setting Behaviour in Switzerland: Evidence from CPI Micro Data”, Swiss Journal of Economics and Statistics, 145(3), pp. 293–349.

Kilian, Lutz (1998), “Small-Sample Confidence Intervals for Impulse Response Functions”, The Review of Economics and Statistics, 80(2), pp. 218–230.

Kwiatkowski, Denis, Peter C. B. Phillips, Peter Schmidt and Yongcheol Shin (1992), “Testing the Null Hypothesis of Stationarity against the Alternative of a Unit Root: How Sure Are We that Economic Time Series Have a Unit Root?”, Journal of Econometrics, 54(1–3), pp. 159–178.

Leeper, Eric M., and Tao Zha (2001), “Assessing Simple Policy Rules: A View from a Complete Macroeconomic Model”, Federal Reserve Bank of St. Louis Review, 83(4), pp. 83–110.

Rabanal, Pau (2007), “Does Inflation Increase after a Monetary Policy Tightening? Answers Based on an Estimated DSGE model”, Journal of Economic Dynamics and Control, 31(3), pp. 906–937.

Ravenna, Federico, and Carl E. Walsh (2006), “Optimal Monetary Policy with the Cost Channel”, Journal of Monetary Economics, 53(2), pp. 199–216.

Sims, Christopher A. (1992), “Interpreting the Macroeconomic Time Series Facts: The Effects of Monetary Policy”, European Economic Review, 36(5), pp. 975–1000.

Stalder, Peter (2003), “The Decoupling of Rents from Mortgage Rates: Implications of the Rent Law Reform for Monetary Policy”, Swiss National Bank Quarterly Bulletin, 3, pp. 44–57.

Stock, James H., and Mark W. Watson (2002), “Macroeconomic Forecasting using Diffusion Indexes”, Journal of Business & Economic Statistics, 20(2), pp. 147–162.

Stock, James H., and Mark W. Watson (2005), “Implications of Dynamic Factor Models for VAR Analysis”, NBER Working Paper No. 11467, National Bureau of Economic Research.

Tillmann, Peter (2008), “Do Interest Rates Drive Inflation Dynamics? An Analysis of the Cost Channel of Monetary Transmission”, Journal of Economic Dynamics and Control, 32(9), pp. 2723–2744.

Walsh, Carl E. (2003), Monetary Theory and Policy, 2nd edn., Cambridge: MIT Press.

Author information

Authors and Affiliations

Corresponding author

Additional information

We thank Gregor Bäurle, Sandra Eickmeier, Marc Giannoni, Sylvia Kaufmann, Carlos Lenz, Matthias Lutz, Klaus Neusser, Barbara Rudolf, Frank Schmid, Peter Tillmann, Mathias Zurlinden, two anonymous referees, participants of the YSEM meeting, the SSES annual meeting, the BuBa-OeNB-SNB workshop and the SNB Brown Bag workshop for helpful discussions and suggestions. An earlier version was published as SNB Working Paper 2011–7 titled “Sectoral Inflation Dynamics, Idiosyncratic Shocks and Monetary Policy”. Andreas Bachmann and Andrea Schnell provided excellent research assistance. The views expressed in this paper are those of the authors and not necessarily those of the Swiss National Bank.

Rights and permissions

Open Access This article is distributed under the terms of the Creative Commons Attribution 2.0 International License ( https://creativecommons.org/licenses/by/2.0 ), which permits unrestricted use, distribution, and reproduction in any medium, provided the original work is properly cited.

About this article

Cite this article

Kaufmann, D., Lein, S. Is there a Swiss price puzzle?. Swiss J Economics Statistics 148, 57–75 (2012). https://doi.org/10.1007/BF03399360

Published:

Issue Date:

DOI: https://doi.org/10.1007/BF03399360