Abstract

This chapter focuses on the task of grouping consumers and, in so doing, revealing naturally existing or creating artificial market segments. The chapter covers algorithms falling into three categories: distance-based methods, model-based methods, and algorithms integrating variable selection with the task of extracting market segments. In addition, data structure analysis is introduced. Data structure analysis provides insight into whether the resulting market segments are naturally occurring in the market; created but stable; or created and unstable across repeated calculations. A series of questions are included in a checklist to assist with the implementation of this step.

You have full access to this open access chapter, Download chapter PDF

1 Grouping Consumers

Data-driven market segmentation analysis is exploratory by nature. Consumer data sets are typically not well structured. Consumers come in all shapes and forms; a two-dimensional plot of consumers’ product preferences typically does not contain clear groups of consumers. Rather, consumer preferences are spread across the entire plot. The combination of exploratory methods and unstructured consumer data means that results from any method used to extract market segments from such data will strongly depend on the assumptions made on the structure of the segments implied by the method. The result of a market segmentation analysis, therefore, is determined as much by the underlying data as it is by the extraction algorithm chosen. Segmentation methods shape the segmentation solution.

Many segmentation methods used to extract market segments are taken from the field of cluster analysis. In that case, market segments correspond to clusters. As pointed out by Hennig and Liao (2013), selecting a suitable clustering method requires matching the data analytic features of the resulting clustering with the context-dependent requirements that are desired by the researcher (p. 315). It is, therefore, important to explore market segmentation solutions derived from a range of different clustering methods. It is also important to understand how different algorithms impose structure on the extracted segments.

One of the most illustrative examples of how algorithms impose structure is shown in Fig. 7.1. In this figure, the same data set – containing two spiralling segments – is segmented using two different algorithms, and two different numbers of segments. The top row in Fig. 7.1 shows the market segments obtained when running k-means cluster analysis (for details see Sect. 7.2.3) with 2 (left) and 8 segments (right), respectively. As can be seen, k-means cluster analysis fails to identify the naturally existing spiral-shaped segments in the data. This is because k-means cluster analysis aims at finding compact clusters covering a similar range in all dimensions.

k-means and single linkage hierarchical clustering of two spirals

The bottom row in Fig. 7.1 shows the market segments obtained from single linkage hierarchical clustering (for details see Sect. 7.2.2). This algorithm correctly identifies the existing two spiralling segments, even if the incorrect number of segments is specified up front. This is because the single linkage method constructs snake-shaped clusters. When asked to return too many (8) segments, outliers are defined as micro-segments, but the two main spirals are still correctly identified. k-means cluster analysis fails to identify the spirals because it is designed to construct round, equally sized clusters. As a consequence, the k-means algorithm ignores the spiral structure and, instead, places consumers in the same market segments if they are located close to one another (in Euclidean space), irrespective of the spiral they belong to.

This illustration gives the impression that single linkage clustering is much more powerful, and should be preferred over other approaches of extracting market segments from data. This is not the case. This particular data set was constructed specifically to play to the strengths of the single linkage algorithm allowing single linkage to identify the grouping corresponding to the spirals, and highlighting how critical the interaction between data and algorithm is. There is no single best algorithm for all data sets. If consumer data is well-structured, and well-separated, distinct market segments exist, tendencies of different algorithms matter less. If, however, data is not well-structured, the tendency of the algorithm influences the solution substantially. In such situations, the algorithm will impose a structure that suits the objective function of the algorithm.

The aim of this chapter is to provide an overview of the most popular extraction methods used in market segmentation, and point out their specific tendencies of imposing structure on the extracted segments. None of these methods outperform other methods in all situations. Rather, each method has advantages and disadvantages.

So-called distance-based methods are described first. Distance-based methods use a particular notion of similarity or distance between observations (consumers), and try to find groups of similar observations (market segments). So-called model-based methods are described second. These methods formulate a concise stochastic model for the market segments. In addition to those main two groups of extraction methods, a number of methods exist which try to achieve multiple aims in one step. For example, some methods perform variable selection during the extraction of market segments. A few such specialised algorithms are also discussed in this chapter.

Because no single best algorithm exists, investigating and comparing alternative segmentation solutions is critical to arriving at a good final solution. Data characteristics and expected or desired segment characteristics allow a pre-selection of suitable algorithms to be included in the comparison. Table 7.1 contains the information needed to guide algorithm selection.

The size of the available data set indicates if the number of consumers is sufficient for the available number of segmentation variables, the expected number of segments, and the segment sizes. The minimum segment size required from a target segment has been defined as one of the knock-out criteria in Step 2. It informs the expectation about how many segments of which size will be extracted. If the target segment is expected to be a niche segment, larger sample sizes are required. Larger samples allow a more fine-grained extraction of segments. If the number of segmentation variables is large, but not all segmentation variables are expected to be key characteristics of segments, extraction algorithms which simultaneously select variables are helpful (see Sect. 7.4).

The scale level of the segmentation variables determines the most suitable variant of an extraction algorithms. For distance-based methods, the choice of the distance measure depends on the scale level of the data. The scale level also determines the set of suitable segment-specific models in the model-based approach. Other special structures of the data can restrict the set of suitable algorithms. If the data set contains repeated measurements of consumers over time, for example, an algorithm that takes this longitudinal nature of the data into account is needed. Such data generally requires a model-based approach.

We also need to specify the characteristics consumers should have in common to be placed in the same segment, and how they should differ from consumers in other segments. These features have, conceptually, been specified in Step 2, and need to be recalled here. The structure of segments extracted by the algorithm needs to align with these expected characteristics.

We distinguish directly observable characteristics from those that are only indirectly accessible. Benefits sought are an example of a directly observable characteristic. They are contained directly in the data, placing no restrictions on the segment extraction algorithm to be chosen. An example of an indirect characteristic is consumer price sensitivity. If the data contains purchase histories and price information, and market segments are based on similar price sensitivity levels, regression models are needed. This, in turn calls for the use of a model-based segment extraction algorithm.

In the case of binary segmentation variables, another aspect needs to be considered. We may want consumers in the same segments to have both the presence and absence of segmentation variables in common. In this case, we need to treat the binary segmentation variables symmetrically (with 0s and 1s treated equally). Alternatively, we may only care about segmentation variables consumers have in common. In this case, we treat them asymmetrically (with only common 1s being of interest). An example of where it makes sense to treat them asymmetrically is if we use vacation activities as the segmentation variables. It is very interesting if two tourists both engage in horse-riding during their vacation. It is not so interesting if two tourists do not engage in horse-riding. Biclustering (see Sect. 7.4.1) uses binary information asymmetrically. Distance-based methods can use distance measures that account for this asymmetry, and extract segments characterised by common 1s.

2 Distance-Based Methods

Consider the problem of finding groups of tourists with similar activity patterns when on vacation. A fictitious data set is shown in Table 7.2. It contains seven people indicating the percentage of time they spend enjoying beach, action, and culture when on vacation. Anna and Bill only want to relax on the beach, Frank likes beach and action, Julia and Maria like beach and culture, Michael wants action and a little bit of culture, and Tom does everything.

Market segmentation aims at grouping consumers into groups with similar needs or behaviour, in this example: groups of tourists with similar patterns of vacation activities. Anna and Bill have exactly the same profile, and should be in the same segment. Michael is the only one not interested in going to the beach, which differentiates him from the other tourists. In order to find groups of similar tourists one needs a notion of similarity or dissimilarity , mathematically speaking: a distance measure.

2.1 Distance Measures

Table 7.2 is a typical data matrix. Each row represents an observation (in this case a tourist), and every column represents a variable (in this case a vacation activity). Mathematically, this can be represented as an n × p matrix where n stands for the number of observations (rows) and p for the number of variables (columns):

The vector corresponding to the i-th row of matrix X is denoted as xi = (xi1, xi2, …, xip)′ in the following, such that \(\mathcal {X} = \{{\mathbf {x}}_1, {\mathbf {x}}_2, \ldots {\mathbf {x}}_p\}\) is the set of all observations. In the example above, Anna’s vacation activity profile is vector x1 = (100, 0, 0)′ and Tom’s vacation activity profile is vector x7 = (50, 20, 30)′.

Numerous approaches to measuring the distance between two vectors exist; several are used routinely in cluster analysis and market segmentation. A distance is a function d(⋅, ⋅) with two arguments: the two vectors x and y between which the distance is being calculated. The result is the distance between them (a nonnegative value). A good way of thinking about distance is in the context of geography. If the distance between two cities is of interest, the location of the cities are the two vectors, and the length of the air route in kilometres is the distance. But even in the context of geographical distance, other measures of natural distance between two cities are equally valid, for example, the distance a car has to drive on roads to get from one city to the other.

A distance measure has to comply with a few criteria. One criterion is symmetry, that is:

A second criterion is that the distance of a vector to itself and only to itself is 0:

In addition, most distance measures fulfil the so-called triangle inequality:

The triangle inequality says that if one goes from x to z with an intermediate stop in y, the combined distance is at least as long as going from x to z directly.

Let x = (x1, …, xp)′ and y = (y1, …, yp)′ be two p-dimensional vectors. The most common distance measures used in market segmentation analysis are:

- Euclidean distance: :

-

$$\displaystyle \begin{aligned} d(\mathbf{x}, \mathbf{y}) = \sqrt{\sum_{j=1}^p (x_j - y_j)^2} \end{aligned}$$

- Manhattan or absolute distance: :

-

$$\displaystyle \begin{aligned} d(\mathbf{x}, \mathbf{y}) = \sum_{j=1}^p |x_j - y_j| \end{aligned}$$

- Asymmetric binary distance: :

-

applies only to binary vectors, that is, all xj and yj are either 0 or 1.

$$\displaystyle \begin{aligned} d(\mathbf{x}, \mathbf{y}) = \left\{ \begin{array}{l} 0, \quad \mathbf{x} = \mathbf{y} = \mathbf{0} \\ (\#\{j| x_j=1 \mbox{ and } y_j=1\})/ (\#\{j| x_j=1 \mbox{ or } y_j=1\}) \end{array}\right. \end{aligned}$$In words: the number of dimensions where both x and y are equal to 1 divided by the number of dimensions where at least one of them is 1.

Euclidean distance is the most common distance measure used in market segmentation analysis. Euclidean distance corresponds to the direct “straight-line” distance between two points in two-dimensional space, as shown in Fig. 7.2 on the left. Manhattan distance derives its name from the fact that it gives the distance between two points assuming that streets on a grid (like in Manhattan) need to be used to get from one point to another. Manhattan distance is illustrated in Fig. 7.2 on the right. Both Euclidean and Manhattan distance use all dimensions of the vectors x and y.

A comparison of Euclidean and Manhattan distance

The asymmetric binary distance does not use all dimensions of the vectors. It only uses dimensions where at least one of the two vectors has a value of 1. It is asymmetric because it treats 0s and 1s differently. Similarity between two observations is only concluded if they share 1s, but not if they share 0s. The dissimilarity between two observations is increased if one has a 1 and the other not. This has implications for market segmentation analysis. Imagine, for example, that the tourist vacation activity profiles not only include common vacation activities, but also unusual activities, such as horseback riding and bungee jumping. The fact that two tourists have in common that they do not ride horses or that they do not bungee jump is not very helpful in terms of extracting market segments because the overall proportion of horse riders and bungee jumpers in the tourist population is low. If, however, two tourists do horse ride or bungee jump, this represents key information about similarities between them.

The asymmetric binary distance corresponds to the proportion of common 1s over all dimensions where at least one vector contains a 1. In the tourist example: the number of common vacation activities divided by the number of vacation activities at least one of the two tourists engages in. A symmetric binary distance measure (which treats 0s and 1s equally) emerges from using the Manhattan distance between the two vectors. The distance is then equal to the number of vacation activities where values are different.

The standard R function to calculate distances is called dist(). It takes as arguments a data matrix x and – optionally – the distance method. If no distance method is explicitly specified, Euclidean distance is the default. The R function returns all pairwise distances between the rows of x.

Using the vacation activity data in Table 7.2, we first need to load the data:

R> data("annabill", package = "MSA")

Then, we can calculate the Euclidean distance between all tourists with the following command:

R> D1 <- dist(annabill) R> round(D1, 2)

Anna Bill Frank Julia Maria Michael Bill 0.00 Frank 56.57 56.57 Julia 42.43 42.43 50.99 Maria 28.28 28.28 48.99 14.14 Michael 134.91 134.91 78.74 115.76 120.83 Tom 61.64 61.64 37.42 28.28 37.42 88.32

The distance between Anna and Bill is zero because they have identical vacation activity profiles. The distance between Michael and all other people in the data set is substantial because Michael does not go to the beach where most other tourists spend a lot of time.

Manhattan distance – which is also referred to as absolute distance – is very similar to Euclidean distance for this data set:

R> D2 <- dist(annabill, method = "manhattan") R> D2

Anna Bill Frank Julia Maria Michael Bill 0 Frank 80 80 Julia 60 60 80 Maria 40 40 80 20 Michael 200 200 120 180 180 Tom 100 100 60 40 60 140

No rounding is necessary because the Manhattan distance is automatically integer if all values in the data matrix are integer.

The printout contains only six rows and columns in both cases. To save computer memory, dist() does not return the full symmetric matrix of all pairwise distances. It only returns the lower triangle of the matrix. If the full matrix is required, it can be obtained by coercing the return object of dist() to the full 7 × 7 matrix:

R> as.matrix(D2)

Anna Bill Frank Julia Maria Michael Tom Anna 0 0 80 60 40 200 100 Bill 0 0 80 60 40 200 100 Frank 80 80 0 80 80 120 60 Julia 60 60 80 0 20 180 40 Maria 40 40 80 20 0 180 60 Michael 200 200 120 180 180 0 140 Tom 100 100 60 40 60 140 0

Both Euclidean and Manhattan distance treat all dimensions of the data equally; they take a sum over all dimensions of squared or absolute differences. If the different dimensions of the data are not on the same scale (for example, dimension 1 indicates whether or not a tourist plays golf, and dimension 2 indicates how many dollars the tourist spends per day on dining out on average), the dimension with the larger numbers will dominate the distance calculation between two observations. In such situations data needs to be standardised before calculating distances (see Sect. 6.4.2).

Function dist can only be used if the segmentation variables are either all metric or all binary. In R package cluster (Maechler et al. 2017), function daisy calculates the dissimilarity matrix between observations contained in a data frame. In this data frame the variables can be numeric, ordinal, nominal and binary. Following Gower (1971), all variables are rescaled to a range of [0, 1] which allows for a suitable weighting between variables. If variables are metric, the results are the same as for dist:

R> library("cluster") R> round(daisy(annabill), digits = 2)

Dissimilarities : Anna Bill Frank Julia Maria Michael Bill 0.00 Frank 56.57 56.57 Julia 42.43 42.43 50.99 Maria 28.28 28.28 48.99 14.14 Michael 134.91 134.91 78.74 115.76 120.83 Tom 61.64 61.64 37.42 28.28 37.42 88.32 Metric : euclidean Number of objects : 7

2.2 Hierarchical Methods

Hierarchical clustering methods are the most intuitive way of grouping data because they mimic how a human would approach the task of dividing a set of n observations (consumers) into k groups (segments). If the aim is to have one large market segment (k = 1), the only possible solution is one big market segment containing all consumers in data \(\mathcal {X}\). At the other extreme, if the aim is to have as many market segments as there are consumers in the data set (k = n), the number of market segments has to be n, with each segment containing exactly one consumer. Each consumer represents their own cluster. Market segmentation analysis occurs between those two extremes.

Divisive hierarchical clustering methods start with the complete data set \(\mathcal {X}\) and splits it into two market segments in a first step. Then, each of the segments is again split into two segments. This process continues until each consumer has their own market segment.

Agglomerative hierarchical clustering approaches the task from the other end. The starting point is each consumer representing their own market segment (n singleton clusters). Step-by-step, the two market segments closest to one another are merged until the complete data set forms one large market segment.

Both approaches result in a sequence of nested partitions. A partition is a grouping of observations such that each observation is exactly contained in one group. The sequence of partitions ranges from partitions containing only one group (segment) to n groups (segments). They are nested because the partition with k + 1 groups (segments) is obtained from the partition with k groups by splitting one of the groups.

Numerous algorithms have been proposed for both strategies. The unifying framework for agglomerative clustering – which was developed in the seminal paper by Lance and Williams (1967) – contains most methods still in use today. In each step, standard implementations of hierarchical clustering perform the optimal step. This leads to a deterministic algorithm. This means that every time the hierarchical clustering algorithm is applied to the same data set, the exactly same sequence of nested partitions is obtained. There is no random component.

Underlying both divisive and agglomerative clustering is a measure of distance between groups of observations (segments). This measure is determined by specifying (1) a distance measure d(x, y) between observations (consumers) x and y, and (2) a linkage method . The linkage method generalises how, given a distance between pairs of observations, distances between groups of observations are obtained. Assuming two sets \(\mathcal {X}\) and \(\mathcal {Y}\) of observations (consumers), the following linkage methods are available in the standard R function hclust() for measuring the distance \(l(\mathcal {X},\mathcal {Y})\) between these two sets of observations:

- Single linkage: :

-

distance between the two closest observations of the two sets.

$$\displaystyle \begin{aligned} l(\mathcal{X},\mathcal{Y}) = \min_{\mathbf{x}\in \mathcal{X}, \mathbf{y}\in \mathcal{Y}} d(\mathbf{x},\mathbf{y}) \end{aligned}$$ - Complete linkage: :

-

distance between the two observations of the two sets that are farthest away from each other.

$$\displaystyle \begin{aligned} l(\mathcal{X},\mathcal{Y}) = \max_{\mathbf{x}\in \mathcal{X}, \mathbf{y}\in \mathcal{Y}} d(\mathbf{x},\mathbf{y}) \end{aligned}$$ - Average linkage: :

-

mean distance between observations of the two sets.

$$\displaystyle \begin{aligned} l(\mathcal{X},\mathcal{Y}) = \frac 1{|\mathcal{X}||\mathcal{Y}|}\sum_{\mathbf{x}\in \mathcal{X}} \sum_{\mathbf{y}\in \mathcal{Y}} d(\mathbf{ x},\mathbf {y}), \end{aligned}$$where \(|\mathcal {X}|\) denotes the number of elements in \(\mathcal {X}\).

These linkage methods are illustrated in Fig. 7.3, and all of them can be combined with any distance measure. There is no correct combination of distance and linkage method. Clustering in general, and hierarchical clustering in specific, are exploratory techniques. Different combinations can reveal different features of the data.

A comparison of different linkage methods between two sets of points

Single linkage uses a “next neighbour” approach to join sets, meaning that the two closest consumers are united. As a consequence, single linkage hierarchical clustering is capable of revealing non-convex, non-linear structures like the spirals in Fig. 7.1. In situations where clusters are not well-separated – and this means in most consumer data situations – the next neighbour approach can lead to undesirable chain effects where two groups of consumers form a segment only because two consumers belonging to each of those segments are close to one another. Average and complete linkage extract more compact clusters.

A very popular alternative hierarchical clustering method is named after Ward (1963), and based on squared Euclidean distances. Ward clustering joins the two sets of observations (consumers) with the minimal weighted squared Euclidean distance between cluster centers. Cluster centers are the midpoints of each cluster. They result from taking the average over the observations in the cluster. We can intepret them as segment representatives.

When using Ward clustering we need to check that the correct distance is used as input (Murtagh and Legendre 2014). The two options are Euclidean distance or squared Euclidean distance. Function hclust() in R can deal with both kinds of input. The input, along with the suitable linkage method, needs to be specified in the R command as either Euclidean distance with method = "ward.D2", or as squared Euclidean distance with method = "ward.D" The result of hierarchical clustering is typically presented as a dendrogram . A dendrogram is a tree diagram. The root of the tree represents the one-cluster solution where one market segment contains all consumers. The leaves of the tree are the single observations (consumers), and branches in-between correspond to the hierarchy of market segments formed at each step of the procedure. The height of the branches corresponds to the distance between the clusters. Higher branches point to more distinct market segments. Dendrograms are often recommended as a guide to select the number of market segments. Based on the authors’ experience with market segmentation analysis using consumer data, however, dendrograms rarely provide guidance of this nature because the data sets underlying the analysis are not well structured enough.

As an illustration of the dendrogram, consider the seven tourists in Table 7.2 and the Manhattan distances between them. Agglomerative hierarchical clustering with single linkage will first identify the two people with the smallest distance (Anna and Bill with a distance of 0). Next, Julia and Maria are joined into a market segment because they have the second smallest distance between them (20). The single linkage distance between these two groups is 40, because that is the distance from Maria to Anna and Bill. Tom has a distance of 40 to Julia, hence Anna, Bill, Julia, Maria and Tom are joined to a group of five in the third step. This process continues until all tourists are united in one big group. The resulting dendrogram is shown in Fig. 7.4 on the left.

Single and complete linkage clustering of the tourist data shown in Table 7.2

The result of complete linkage clustering is provided in the right dendrogram in Fig. 7.4. For this small data set, the result is very similar. The only major difference is that Frank and Tom are first grouped together in a segment of two, before they are merged into a segment with all other tourists (except for Michael) in the data set. In both cases, Michael is merged last because his activity profile is very different. The result from average linkage clustering is not shown because the corresponding dendrogram is almost identical to that of complete linkage clustering.

The order of the leaves of the tree (the observations or consumers) is not unique. At every split into two branches, the left and right branch could be exchanged, resulting in 2n possible dendrograms for exactly the same clustering where n is the number of consumers in the data set. As a consequence, dendrograms resulting from different software packages may look different although they represent exactly the same market segmentation solution. Another possible source of variation between software packages is how ties are broken, meaning, which two groups are joined first when several have exactly the same distance .

Example: Tourist Risk Taking

A data set on “tourist disasters” contains survey data collected by an online research panel company in October 2015 commissioned by UQ Business School (Hajibaba et al. 2017). The target population were adult Australian residents who had undertaken at least one personal holiday in the past 12 months. The following commands load the data matrix:

R> library("MSA") R> data("risk", package = "MSA") R> dim(risk)

[1] 563 6

This data set contains 563 respondents who state how often they take risks from the following six categories:

-

1.

recreational risks: e.g., rock-climbing, scuba diving

-

2.

health risks: e.g., smoking, poor diet, high alcohol consumption

-

3.

career risks: e.g., quitting a job without another to go to

-

4.

financial risks: e.g., gambling, risky investments

-

5.

safety risks: e.g., speeding

-

6.

social risks: e.g., standing for election, publicly challenging a rule or decision

Respondents are presented with an ordinal scale consisting of five answer options (1=never, 5=very often). In the subsequent analysis, we assume equidistance between categories. Respondents, on average, display risk aversion with mean values for all columns close to 2 (=rarely):

R> colMeans(risk)

Recreational Health Career Financial 2.190053 2.396092 2.007105 2.026643 Safety Social 2.266430 2.017762

The following command extracts market segments from this data set using Manhattan distance and complete linkage :

R> risk.dist <- dist(risk, method = "manhattan") R> risk.hcl <- hclust(risk.dist, method = "complete") R> risk.hcl

Call: hclust(d = risk.dist, method = "complete") Cluster method : complete Distance : manhattan Number of objects: 563

plot(risk.hcl) generates the dendrogram shown in Fig. 7.5. The dendrogram visualises the sequence of nested partitions by indicating each merger or split. The straight line at the top of the dendrogram indicates the merger of the last two groups into a single group. The y-axis indicates the distance between these two groups. At the bottom each single observation is one line.

Complete linkage hierarchical cluster analysis of the tourist risk taking data set

The dendrogram in Fig. 7.5 indicates that the largest additional distance between two clusters merged occurred when the last two clusters were combined to the single cluster containing all observations. Cutting the dendrogram at a specific height selects a specific partition. The boxes numbered 1–6 in Fig. 7.5 illustrate how this dendrogram or tree can be cut into six market segments. The reason that the boxes are not numbered from left to right is that the market segment labelled number 1 contains the first observation (the first consumer) in the data set. Which consumers have been assigned to which market segment can be computed using function cutree(), which takes an object as returned by hclust and either the height h at which to cut or the number k of segments to cut the tree into.

R> c2 <- cutree(risk.hcl, h = 20) R> table(c2)

c2 1 2 511 52

R> c6 <- cutree(risk.hcl, k = 6) R> table(c6)

c6 1 2 3 4 5 6 90 275 27 25 74 72

A simple way to assess the characteristics of the clusters is to look at the column-wise means by cluster.

R> c6.means <- aggregate(risk, list(Cluster = c6), mean) R> round(c6.means, 1)

Recreational Health Career Financial Safety Social 1 2.0 2.2 1.9 2.0 2.2 2.8 2 1.9 1.8 1.5 1.6 2.0 1.4 3 3.9 4.4 2.9 3.2 3.3 4.1 4 4.1 3.3 4.1 2.8 3.4 3.2 5 2.3 2.6 3.2 2.6 2.6 2.2 6 2.0 3.8 1.8 2.4 2.3 2.0

But it is much easier to understand the cluster characteristics by visualising the column-wise means by clusters using a barchart (Fig. 7.6). barchart(risk. hcl, risk, k=6) from R package flexclust results in such a barchart. (A refined version of this plot – referred to as the segment profile plot – is described in detail in Sect. 8.3). The dark red dots correspond to the total mean values across all respondents; the bars indicate the mean values within each one of the segments. Segments are interpreted by inspecting the difference between the total population (red dots) and the segments (bars). For the tourist risk taking data set, the largest segment is cluster 2. People assigned to this segment avoid all types of risks as indicated by all bars being lower than all the red dots. Segments 3 and 4 display above average risk taking in all areas, while segments 1, 5 and 6 have average risk taking values for 5 of the 6 categories, but are characterised by their willingness to take above average risk in one category. Members of segment 1 are more willing to accept social risks than the overall population, members of segment 5 are more willing to accept career risks, and members of segment 6 are more willing to accept health risks.

Bar chart of cluster means from hierarchical clustering for the tourist risk taking data set

2.3 Partitioning Methods

Hierarchical clustering methods are particularly well suited for the analysis of small data sets with up to a few hundred observations. For larger data sets, dendrograms are hard to read, and the matrix of pairwise distances usually does not fit into computer memory. For data sets containing more than 1000 observations (consumers), clustering methods creating a single partition are more suitable than a nested sequence of partitions. This means that – instead of computing all distances between all pairs of observations in the data set at the beginning of a hierarchical partitioning cluster analysis using a standard implementation – only distances between each consumer in the data set and the centre of the segments are computed. For a data set including information about 1000 consumers, for example, the agglomerative hierarchical clustering algorithm would have to calculate (1000 × 999)∕2 = 499, 500 distances for the pairwise distance matrix between all consumers in the data set.

A partitioning clustering algorithm aiming to extract five market segments, in contrast, would only have to calculate between 5 and 5000 distances at each step of the iterative or stepwise process (the exact number depends on the algorithm used). In addition, if only a few segments are extracted, it is better to optimise specifically for that goal, rather than building the complete dendrogram and then heuristically cutting it into segments.

2.3.1 k-Means and k-Centroid Clustering

The most popular partitioning method is k-means clustering. Within this method, a number of algorithms are available. R function kmeans() implements the algorithms by Forgy (1965), Hartigan and Wong (1979), Lloyd (1982) and MacQueen (1967). These algorithms use the squared Euclidean distance . A generalisation to other distance measures, also referred to as k-centroid clustering, is provided in R package flexclust.

Let \(\mathcal {X} = \{{\mathbf {x}}_1,\ldots ,{\mathbf {x}}_n\}\) be a set of observations (consumers) in a data set. Partitioning clustering methods divide these consumers into subsets (market segments) such that consumers assigned to the same market segment are as similar to one another as possible, while consumers belonging to different market segments are as dissimilar as possible. The representative of a market segment is referred to in many partitioning clustering algorithms as the centroid . For the k-means algorithm based on the squared Euclidean distance , the centroid consists of the column-wise mean values across all members of the market segment. The data set contains observations (consumers) in rows, and variables (behavioural information or answers to survey questions) in columns. The column-wise mean, therefore, is the average response pattern across all segmentation variables for all members of the segment (Fig. 7.6).

The following generic algorithm represents a heuristic for solving the optimisation problem of dividing consumers into a given number of segments such that consumers are similar to their fellow segment members, but dissimilar to members of other segments. This algorithm is iterative; it improves the partition in each step, and is bound to converge, but not necessarily to the global optimum .

It involves five steps with the first four steps visualised in a simplified way in Fig. 7.7:

-

1.

Specify the desired number of segments k.

Fig. 7.7

Simplified visualisation of the k-means clustering algorithm

-

2.

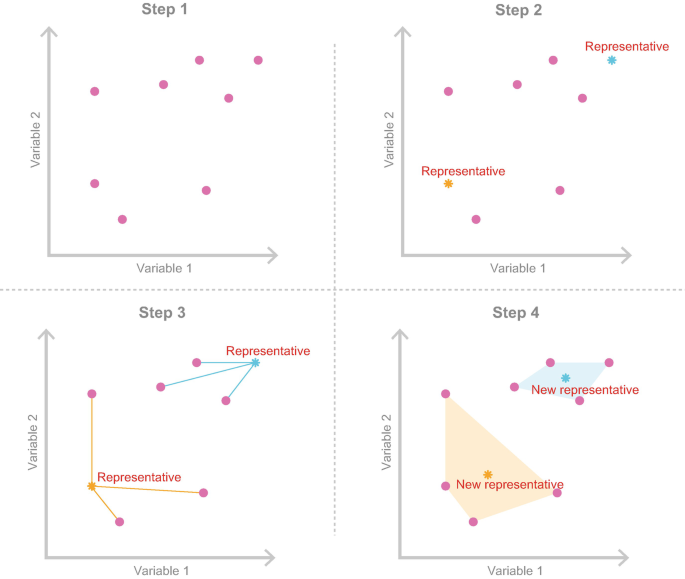

Randomly select k observations (consumers) from data set \(\mathcal {X}\) (see Step 2 in Fig. 7.7) and use them as initial set of cluster centroids \(\mathcal {C}=\{{\mathbf {c}}_1,\ldots ,{\mathbf {c}}_k\}\). If five market segments are being extracted, then five consumers are randomly drawn from the data set, and declared the representatives of the five market segments. Of course, these randomly chosen consumers will – at this early stage of the process – not be representing the optimal segmentation solution. They are needed to get the step wise (iterative) partitioning algorithm started.

-

3.

Assign each observation xi to the closest cluster centroid (segment representative, see Step 3 in Fig. 7.7) to form a partition of the data, that is, k market segments \(\mathcal {S}_1,\ldots ,\mathcal {S}_k\) where

$$\displaystyle \begin{aligned}\mathcal{S}_j = \{\mathbf{x}\in\mathcal{X}|d(\mathbf{x},{\mathbf{c}}_j)\le d(\mathbf{x},{\mathbf{c}}_h),\;1\le h\le k\}.\end{aligned} $$This means that each consumer in the data set is assigned to one of the initial segment representatives. This is achieved by calculating the distance between each consumer and each segment representative, and then assigning the consumer to the market segment with the most similar representative. If two segment representatives are equally close, one needs to be randomly selected. The result of this step is an initial – suboptimal – segmentation solution. All consumers in the data set are assigned to a segment. But the segments do not yet comply with the criterion that members of the same segment are as similar as possible, and members of different segments are as dissimilar as possible.

-

4.

Recompute the cluster centroids (segment representatives) by holding cluster membership fixed, and minimising the distance from each consumer to the corresponding cluster centroid (representative see Step 4 in Fig. 7.7):

$$\displaystyle \begin{aligned}{\mathbf{c}}_j = \arg\min_{\mathbf{c}} \sum_{\mathbf{x}\in\mathcal{S}_j} d(\mathbf{x},\mathbf{ c}).\end{aligned}$$For squared Euclidean distance , the optimal centroids are the cluster-wise means, for Manhattan distance cluster-wise medians, resulting in the so-called k-means and k-medians procedures, respectively. In less mathematical terms: what happens here is that – acknowledging that the initial segmentation solution is not optimal – better segment representatives need to be identified. This is exactly what is achieved in this step: using the initial segmentation solution, one new representative is “elected” for each of the market segments. When squared Euclidean distance is used, this is done by calculating the average across all segment members, effectively finding the most typical, hypothetical segment members and declaring them to be the new representatives.

-

5.

Repeat from step 3 until convergence or a pre-specified maximum number of iterations is reached. This means that the steps of assigning consumers to their closest representative, and electing new representatives is repeated until the point is reached where the segment representatives stay the same. This is when the stepwise process of the partitioning algorithm stops and the segmentation solution is declared to be the final one.

The algorithm will always converge: the stepwise process used in a partitioning clustering algorithm will always lead to a solution. Reaching the solution may take longer for large data sets, and large numbers of market segments, however. The starting point of the process is random. Random initial segment representatives are chosen at the beginning of the process. Different random initial representatives (centroids) will inevitably lead to different market segmentation solutions. Keeping this in mind is critical to conducting high quality market segmentation analysis because it serves as a reminder that running one single calculation with one single algorithm leads to nothing more than one out of many possible segmentation solutions. The key to a high quality segmentation analysis is systematic repetition, enabling the data analyst to weed out less useful solutions, and present to the users of the segmentation solution – managers of the organisation wanting to adopt target marketing – the best available market segment or set of market segments.

In addition, the algorithm requires the specification of the number of segments. This sounds much easier than it is. The challenge of determining the optimal number of market segments is as old as the endeavour of grouping people into segments itself (Thorndike 1953). A number of indices have been proposed to assist the data analyst (these are discussed in detail in Sect. 7.5.1). We prefer to assess the stability of different segmentation solutions before extracting market segments. The key idea is to systematically repeat the extraction process for different numbers of clusters (or market segments), and then select the number of segments that leads to either the most stable overall segmentation solution, or to the most stable individual segment. Stability analysis is discussed in detail in Sects. 7.5.3 and 7.5.4. In any case, partitioning clustering does require the data analyst to specify the number of market segments to be extracted in advance.

What is described above is a generic version of a partitioning clustering algorithm. Many variations of this generic algorithm are available; some are discussed in the subsequent subsections. The machine learning community has also proposed a number of clustering algorithms. Within this community, the term unsupervised learning is used to refer to clustering because groups of consumers are created without using an external (or dependent) variable. In contrast, supervised learning methods use a dependent variable. The equivalent statistical methods are regression (when the dependent variable is metric), and classification (when the dependent variable is nominal). Hastie et al. (2009) discuss the relationships between statistics and machine learning in detail. Machine learning algorithms essentially achieve the same thing as their statistical counterparts. The main difference is in the vocabulary used to describe the algorithms.

Irrespective of whether traditional statistical partitioning methods such as k-means are used, or whether any of the algorithms proposed by the machine learning community is applied, distance measures are the basic underlying calculation. Not surprisingly, therefore, the choice of the distance measure has a significant impact on the final segmentation solution. In fact, the choice of the distance measure typically has a bigger impact on the nature of the resulting market segmentation solution than the choice of algorithm (Leisch 2006). To illustrate this, artificial data from a bivariate normal distribution are clustered three times using a generalised version of the k-means algorithm. A different distance measure is used for each calculation: squared Euclidean distance, Manhattan distance, and the difference between angles when connecting observations to the origin.

Figure 7.8 shows the resulting three partitions. As can be seen, squared Euclidean and Manhattan distance result in similarly shaped clusters in the interior of the data. The direction of cluster borders in the outer region of the data set, however, are quite different. Squared Euclidean distance results in diagonal borders, while the borders for Manhattan distance are parallel to the axes. Angle distance slices the data set into cake piece shaped segments. Figure 7.8 shows clearly the effect of the chosen distance measure on the segmentation solution. Note, however, that – while the three resulting segmentation solutions are different – neither of them is superior or inferior, especially given that no natural clusters are present in this data set.

Artificial Gaussian data clustered using squared Euclidean distance (left), Manhattan distance (middle) and angle distance (right)

2.3.1.1 Example: Artificial Mobile Phone Data

Consider a simple artificial data set for a hypothetical mobile phone market. It contains two pieces of information about mobile phone users: the number of features they want in a mobile phone, and the price they are willing to pay for it. We can artificially generate a random sample for such a scenario in R. To do this, we first load package flexclust which also contains a wide variety of partitioning clustering algorithms for many different distance measures:

R> library("flexclust") R> set.seed(1234) R> PF3 <- priceFeature(500, which = "3clust")

Next, we set the seed of the random number generator to 1234. We use seed 1234 throughout the book whenever randomness is involved to make all results reproducible. After setting the seed of the random number generator, it always produces exactly the same sequence of numbers. In the example above, function priceFeature() draws a random sample with uniform distribution on three circles. Data sets drawn with different seeds will all look very similar, but the exact location of points is different.

Figure 7.9 shows the data. The x-axis plots mobile phone features. The y-axis plots the price mobile phone users are willing to pay. The data contains three very distinct and well-separated market segments. Members of the bottom left market segment want a cheap mobile phone with a limited set of features. Members of the middle segment are willing to pay a little bit more, and expect a few additional features. Members of the small market segment located in the top right corner of Fig. 7.9 are willing to pay a lot of money for their mobile phone, but have very high expectations in terms of features.

Artificial mobile phone data set

Next, we extract market segments from this data. Figure 7.9 shows clearly that three market segments exist (when working with empirical data it is not known how many, if any, natural segments are contained in the data). To obtain a solution containing three market segments for the artificially generated mobile phone data set using k-means , we use function cclust() from package flexclust. Compared to the standard R function kmeans(), function cclust() returns richer objects, which are useful for the subsequent visualisation of results using tools from package flexclust. Function cclust() implements the k-means algorithm by determining the centroids using the average values across segment members, and by assigning each observation to the closest centroid using Euclidean distance.

R> PF3.km3 <- cclust(PF3, k = 3) R> PF3.km3

kcca object of family ’kmeans’ call: cclust(x = PF3, k = 3) cluster sizes: 1 2 3 100 200 200

The cluster centres (centroids, representatives of each market segment), and the vector of cluster memberships (the assignment of each consumer to a specific market segment) can be extracted using

R> parameters(PF3.km3)

features / performance / quality price [1,] 7.976827 8.027105 [2,] 5.021999 4.881439 [3,] 1.990105 2.062453

R> clusters(PF3.km3)[1:20]

[1] 1 2 3 3 2 3 2 3 1 1 3 1 3 2 2 3 2 1 2 1

The term [1:20] in the above R command asks for the segment memberships of only the first 20 consumers in the data set to be displayed (to save space). The numbering of the segments (clusters) is random; it depends on which consumers from the data set have been randomly chosen to be the initial segment representatives. Exactly the same solution could be obtained with a different numbering of segments; the market segment labelled cluster 1 in one calculation could be labelled cluster 3 in the next calculation, although the grouping of consumers is the same.

The information about segment membership can be used to plot market segments in colour, and to draw circles around them. These circles are referred to as convex hulls. In two-dimensional space, the convex hull of a set of observations is a closed polygon connecting the outer points in a way that ensures that all points of the set are located within the polygon. An additional requirement is that the polygon has no “inward dents”. This means that any line connecting two data points of the set must not lie outside the convex hull. To generate a coloured scatter plot of the data with convex hulls for the segments – such as the one depicted in Fig. 7.10 – we can use function clusterhull() from package MSA:

Three-segment k-means partition for the artificial mobile phone data set

R> clusterhulls(PF3, clusters(PF3.km3))

Figure 7.10 visualises the segmentation solution resulting from a single run of the k-means algorithm with one specific set of initial segment representatives. The final segmentation solution returned by the k-means algorithm differs for different initial values. Because each calculation starts with randomly selected consumers serving as initial segment representatives, it is helpful to rerun the process of selecting random segment representatives a few times to eliminate a particularly bad initial set of segment representatives. The process of selecting random segment representatives is called random initialisation .

Specifying the number of clusters (number of segments ) is difficult because, typically, consumer data does not contain distinct, well-separated naturally existing market segments. A popular approach is to repeat the clustering procedure for different numbers of market segments (for example: everything from two to eight market segments), and then compare – across those solutions – the sum of distances of all observations to their representative. The lower the distance, the better the segmentation solution because members of market segments are very similar to one another.

We now calculate 10 runs of the k-means algorithm for each number of segments using different random initial representatives (nrep = 10), and retain the best solution for each number of segments. The number of segments varies from 2 to 8 (k = 2:8):

R> PF3.km28 <- stepcclust(PF3, k = 2:8, nrep = 10)

2 : ∗ ∗ ∗ ∗ ∗ ∗ ∗ ∗ ∗ ∗ 3 : ∗ ∗ ∗ ∗ ∗ ∗ ∗ ∗ ∗ ∗ 4 : ∗ ∗ ∗ ∗ ∗ ∗ ∗ ∗ ∗ ∗ 5 : ∗ ∗ ∗ ∗ ∗ ∗ ∗ ∗ ∗ ∗ 6 : ∗ ∗ ∗ ∗ ∗ ∗ ∗ ∗ ∗ ∗ 7 : ∗ ∗ ∗ ∗ ∗ ∗ ∗ ∗ ∗ ∗ 8 : ∗ ∗ ∗ ∗ ∗ ∗ ∗ ∗ ∗ ∗

R> PF3.km28

stepFlexclust object of family ’kmeans’ call: stepcclust(PF3, k = 2:8, nrep = 10) iter converged distsum 1 NA NA 1434.6462 2 5 TRUE 827.6455 3 3 TRUE 464.7213 4 4 TRUE 416.6217 5 11 TRUE 374.4978 6 11 TRUE 339.6770 7 12 TRUE 313.8717 8 15 TRUE 284.9730

In this case, we extract market segmentation solutions containing between 2 and 8 segments (argument k = 2:8). For each one of those solutions, we retain the best out of ten random initialisations (nrep = 10), using the sum of Euclidean distances between the segment members and their segment representatives as criterion.

Function stepcclust() enables automated parallel processing on multiple cores of a computer (see help("stepcclust") for details). This is useful because the repeated calculations for different numbers of segments and different random initialisations are independent. In the example above 7 × 10 = 70 segment extractions are required. Without parallel computing, these 70 segment extractions run sequentially one after the other. Parallel computing means that a number of calculations can run simultaneously. Parallel computing is possible on most modern standard laptops, which can typically run at least four R processes in parallel, reducing the required runtime of the command by a factor of four (e.g., 15 s instead of 60 s). More powerful desktop machines or compute servers allow many more parallel R processes. For single runs of stepcclust() this makes little difference, but as soon as advanced bootstrapping procedures are used, the difference in runtime can be substantial. Calculations which would run for an hour, are processed in 15 min on a laptop, and in 1.5 min on a computer server running 40 parallel processes. The R commands used are exactly the same, but parallel processing needs to be enabled before using them. The help page for function stepcclust() offers examples on how to do that.

The sums of within-cluster distances for different numbers of clusters (number of market segments ) are visualised using plot(PF3.km28). Figure 7.11 shows the resulting scree plot. The scree plot displays – for each number of segments – the sum of within-cluster distances. For clustering results obtained using stepcclust, this is the sum of the Euclidean distances between each segment member and the representative of the segment. The smaller this number, the more homogeneous the segments; members assigned to the same market segment are similar to one another. Optimally, the scree plot shows distinct drops in the sum of within-cluster distances for the first numbers of segments, followed only by small decreases afterwards. The number of segments where the last distinct drop occurs is the optimal number of segments. After this point, homogeneous segments are split up artificially, resulting in no major decreases in the sum of within-cluster distances.

Scree plot for k-means partitions with k = 1, …, 8 segments for the artificial mobile phone data set

The point of the scree plot indicating the best number of segments is where an elbow occurs. The elbow is illustrated in Fig. 7.12. Figure 7.12 contains the scree plot as well as an illustration of the elbow. The elbow is visualised by the two intersecting lines with different slopes. The point where the two lines intersect indicates the optimal number of segments. In the example shown in Fig. 7.12, large distance drops are visible when the number of segments increases from one to two segments, and then again from two to three segments. A further increase in segments leads to small reductions in distance.

Scree plot for k-means partitions with k = 1, …, 8 segments for the artificial mobile phone data set including a visualisation of the elbow consisting of two intersecting lines with different slopes

For this simple artificial data set – constructed to contain three distinct and exceptionally well-separated market segments – the scree plot in Fig. 7.11 correctly points to three market segments being a good choice. The scree plot only provides guidance if market segments are well-separated. If they are not, stability analysis – discussed in detail in Sects. 7.5.3 and 7.5.4 – can inform the number of segments decision.

2.3.1.2 Example: Tourist Risk Taking

To illustrate the difference between an artificially created data set (containing three textbook market segments), and a data set containing real consumer data, we use the tourist risk taking data set. We generate solutions for between 2 and 8 segments (k = 2, …, 8 clusters) using the following command:

R> set.seed(1234) R> risk.km28 <- stepcclust(risk, k = 2:8, nrep = 10)

We use the default seed of 1234 for the random number generator, and initialise each k-means run with a different set of k random representatives. To make it possible for readers to get exactly the same results as shown in this book, the seed is actively set. Figure 7.13 contains the corresponding sum of distances . As can be seen immediately, the drops in distances are much less distinct for this consumer data set than they were for the artificial mobile phone data set. No obvious number of segments recommendation emerges from this plot. But if this plot were the only available decision tool, the two-segment solution would be chosen. We obtain the corresponding bar chart using

Scree plot for k-means partitions with k = 1, …, 8 segments for the tourist risk taking data set

R> barchart(risk.km28[["2"]])

(Figure not shown). The solution containing two market segments splits the data into risk-averse people and risk-takers, reflecting the two main branches of the dendrogram in Fig. 7.5.

Figure 7.14 show the six-segment solution. It is similar to the partition resulting from the hierarchical clustering procedure, but not exactly the same. The six-segment solution resulting from the partitioning algorithm contains two segments of low risk takers (segments 1 and 4), two segments of high risk takers (segments 2 and 5), and two distinctly profiled segments, one of which contains people taking recreational and social risks (segment 3), and another one containing health risk takers (segment 6). Both partitions obtained using either hierarchical or partitioning clustering methods are reasonable from a statistical point of view. Which partition is more suitable to underpin the market segmentation strategy of an organisation needs to be evaluated jointly by the data analyst and the user of the segmentation solution using the tools and methods presented in Sect. 7.5 and in Steps 6, 7 and 8.

Bar chart of cluster means from k-means clustering for the tourist risk taking data set

2.3.2 “Improved” k-Means

Many attempts have been made to refine and improve the k-means clustering algorithm. The simplest improvement is to initialise k-means using “smart” starting values, rather than randomly drawing k consumers from the data set and using them as starting points. Using randomly drawn consumers is suboptimal because it may result in some of those randomly drawn consumers being located very close to one another, and thus not being representative of the data space. Using starting points that are not representative of the data space increases the likelihood of the k-means algorithm getting stuck in what is referred to as a local optimum. A local optimum is a good solution, but not the best possible solution. One way of avoiding the problem of the algorithm getting stuck in a local optimum is to initialise it using starting points evenly spread across the entire data space. Such starting points better represent the entire data set.

Steinley and Brusco (2007) compare 12 different strategies proposed to initialise the k-means algorithm. Based on an extensive simulation study using artificial data sets of known structure, Steinley and Brusco conclude that the best approach is to randomly draw many starting points, and select the best set. The best starting points are those that best represent the data. Good representatives are close to their segment members; the total distance of all segment members to their representatives is small (as illustrated on the left side of Fig. 7.15). Bad representatives are far away from their segment members; the total distance of all segment members to their representatives is high (as illustrated on the right side of Fig. 7.15).

Examples of good (left) and bad (right) starting points for k-means clustering

2.3.3 Hard Competitive Learning

Hard competitive learning, also known as learning vector quantisation (e.g. Ripley 1996), differs from the standard k-means algorithm in how segments are extracted. Although hard competitive learning also minimises the sum of distances from each consumer contained in the data set to their closest representative (centroid), the process by which this is achieved is slightly different. k-means uses all consumers in the data set at each iteration of the analysis to determine the new segment representatives (centroids). Hard competitive learning randomly picks one consumer and moves this consumer’s closest segment representative a small step into the direction of the randomly chosen consumer.

As a consequence of this procedural difference, different segmentation solutions can emerge, even if the same starting points are used to initialise the algorithm. It is also possible that hard competitive learning finds the globally optimal market segmentation solution, while k-means gets stuck in a (or the other way around). Neither of the two methods is superior to the other; they are just different. An application of hard competitive learning in market segmentation analysis can be found in Boztug and Reutterer (2008), where the procedure is used for segment-specific market basket analysis. Hard competitive learning can be computed in R using function cclust(x, k, method = "hardcl") from package flexclust.

2.3.4 Neural Gas and Topology Representing Networks

A variation of hard competitive learning is the neural gas algorithm proposed by Martinetz et al. (1993). Here, not only the segment representative (centroid) is moved towards the randomly selected consumer. Instead, also the location of the second closest segment representative (centroid) is adjusted towards the randomly selected consumer. However, the location of the second closest representative is adjusted to a smaller degree than that of the primary representative. Neural gas has been used in applied market segmentation analysis (Dolnicar and Leisch 2010, 2014). Neural gas clustering can be performed in R using function cclust(x, k, method = "neuralgas") from package flexclust. An application with real data is presented in Sect. 7.5.4.1.

A further extension of neural gas clustering are topology representing networks (TRN, Martinetz and Schulten 1994). The underlying algorithm is the same as in neural gas. In addition, topology representing networks count how often each pair of segment representatives (centroids) is closest and second closest to a randomly drawn consumer. This information is used to build a virtual map in which “similar” representatives – those which had their values frequently adjusted at the same time – are placed next to one other. Almost the same information – which is central to the construction of the map in topology representing networks – can be obtained from any other clustering algorithms by counting how many consumers have certain representatives as closest and second closest in the final segmentation solution. Based on this information, the so-called segment neighbourhood graph (Leisch 2010) is generated. The segment neighbourhood graph is part of the default segment visualisation functions of package flexclust. Currently there appears to be no implementation of the original topology representing network (TRN) algorithm in R, but using neural gas in combination with neighbourhood graphs achieves similar results. Function cclust() returns the neighbourhood graph by default (see Figs. 7.19, 7.41, 8.4 and 8.6 for examples). Neural gas and topology representing networks are not superior to the k-means algorithm or to hard competitive learning ; they are different. As a consequence, they result in different market segmentation solutions. Given that data-driven market segmentation analysis is exploratory by very nature, it is of great value to have a larger toolbox of algorithms available for exploration.

2.3.5 Self-Organising Maps

Another variation of hard competitive learning are self-organising maps (Kohonen 1982, 2001), also referred to as self-organising feature maps or Kohonen maps. Self-organising maps position segment representatives (centroids) on a regular grid, usually a rectangular or hexagonal grid. Examples of grids are provided in Fig. 7.16.

Rectangular (left) and hexagonal (right) grid for self-organising maps

5 × 5 self-organising map of the tourist risk taking data set

Schematic representation of an auto-encoding neural network with one hidden layer

The self-organising map algorithm is similar to hard competitive learning: a single random consumer is selected from the data set, and the closest representative for this random consumer moves a small step in their direction. In addition, representatives which are direct grid neighbours of the closest representative move in the direction of the selected random consumer. The process is repeated many times; each consumer in the data set is randomly chosen multiple times, and used to adjust the location of the centroids in the Kohonen map. What changes over the many repetitions, however, is the extent to which the representatives are allowed to change. The adjustments get smaller and smaller until a final solution is reached. The advantage of self-organising maps over other clustering algorithms is that the numbering of market segments is not random. Rather, the numbering aligns with the grid along which all segment representatives (centroids) are positioned. The price paid for this advantage is that the sum of distances between segment members and segment representatives can be larger than for other clustering algorithms. The reason is that the location of representatives cannot be chosen freely. Rather, the grid imposes restrictions on permissible locations. Comparisons of self-organising maps and topology representing networks with other clustering algorithms, such as the standard k-means algorithm, as well as for market segmentation applications are provided in Mazanec (1999) and Reutterer and Natter (2000).

Many implementations of self-organising maps are available in R packages. Here, we use function som() from package kohonen (Wehrens and Buydens 2007) because it offers good visualisations of the fitted maps. The following R commands load package kohonen, fit a 5 × 5 rectangular self-organising map to the tourist risk taking data, and plot it using the colour palette flxPalettte from package flexclust:

R> library("kohonen") R> set.seed(1234) R> risk.som <- som(risk, somgrid(5, 5, "rect")) R> plot(risk.som, palette.name = flxPalette, main = "")

The resulting map is shown in Fig. 7.17. As specified in the R code, the map has the shape of a five by five rectangular grid, and therefore extracts 25 market segments. Each circle on the grid represents one market segment. Neighbouring segments are more similar to one another than segments located far away from one another. The pie chart provided in Fig. 7.17 for each of the market segments contains basic information about the segmentation variables. Members of the segment in the top left corner take all six kinds of risks frequently. Members of the segment in the bottom right corner do not take any kind of risk ever. The market segments in-between display different risk taking tendencies. For example, members of the market segment located at the very centre of the map take financial risks and career risks, but not recreational, health, safety and social risks.

k-means clustering of the artificial mobile phone data set into 30 clusters

2.3.6 Neural Networks

Auto-encoding neural networks for cluster analysis work mathematically differently than all cluster methods presented so far. The most popular method from this family of algorithms uses a so-called single hidden layer perceptron. A detailed description of the method and its usage in a marketing context is provided by Natter (1999). Hruschka and Natter (1999) compare neural networks and k-means.

Figure 7.18 illustrates a single hidden layer perceptron. The network has three layers. The input layer takes the data as input. The output layer gives the response of the network. In the case of clustering this is the same as the input. In-between the input and output layer is the so-called hidden layer. It is named hidden because it has no connections to the outside of the network. The input layer has one so-called node for every segmentation variable. The example in Fig. 7.18 uses five segmentation variables. The values of the three nodes in the hidden layer h1, h2 and h3 are weighted linear combinations of the inputs

for a non-linear function fj. Each weight αij in the formula is depicted by an arrow connecting nodes in input layer and hidden layer. The fj are chosen such that 0 ≤ hj ≤ 1, and all hj sum up to one (h1 + h2 + h3 = 1).

In the simplest case, the outputs \(\hat x_i\) are weighted combinations of the hidden nodes

where coefficients βji correspond to the arrows between hidden nodes and output nodes. When training the network, the parameters αij and βji are chosen such that the squared Euclidean distance between inputs and outputs is as small as possible for the training data available (the consumers to be segmented). In neural network vocabulary, the term training is used for parameter estimation. This gives the network its name auto-encoder; it is trained to predict the inputs xi as accurately as possible. The task would be trivial if the number of hidden nodes would be equal to the number available as inputs. If, however, fewer hidden nodes are used (which is usually the case), the network is forced to learn how to best represent the data using segment representatives.

Once the network is trained, parameters connecting the hidden layer to the output layer are interpreted in the same way as segment representatives (centroids) resulting from traditional cluster algorithms. The parameters connecting the input layer to the hidden layer can be interpreted in the following way: consider that for one particular consumer h1 = 1, and hence h2 = h3 = 0. In this case \(\hat x_i = \beta _{1i}\) for i = 1, …, 5. This is true for all consumers where h1 is 1 or close to 1. The network predicts the same value for all consumers with h1 ≈ 1. All these consumers are members of market segment 1 with representative β1i. All consumers with h2 ≈ 1, are members of segment 2, and so on.

Consumers who have no hj value close to 1 can be seen as in-between segments. k-means clustering and hard competitive learning produce crisp segmentations, where each consumer belongs to exactly one segment. Neural network clustering is an example of a so-called fuzzy segmentation with membership values between 0 (not a member of this segment) and 1 (member of only this segment). Membership values between 0 and 1 indicate membership in multiple segments. Several implementations of auto-encoding neural networks are available in R. One example is function autoencode() in package autoencoder (Dubossarsky and Tyshetskiy 2015). Many other clustering algorithms generate fuzzy market segmentation solutions, see for example R package fclust (Ferraro and Giordani 2015).

2.4 Hybrid Approaches

Several approaches combine hierarchical and partitioning algorithms in an attempt to compensate the weaknesses of one method with the strengths of the other. The strengths of hierarchical cluster algorithms are that the number of market segments to be extracted does not have to be specified in advance, and that similarities of market segments can be visualised using a dendrogram. The biggest disadvantage of hierarchical clustering algorithms is that standard implementations require substantial memory capacity, thus restricting the possible sample size of the data for applying these methods. Also, dendrograms become very difficult to interpret when the sample size is large.

The strength of partitioning clustering algorithms is that they have minimal memory requirements during calculation, and are therefore suitable for segmenting large data sets. The disadvantage of partitioning clustering algorithms is that the number of market segments to be extracted needs to be specified in advance. Partitioning algorithms also do not enable the data analyst to track changes in segment membership across segmentation solutions with different number of segments because these segmentation solutions are not necessarily nested.

The basic idea behind hybrid segmentation approaches is to first run a partitioning algorithm because it can handle data sets of any size. But the partitioning algorithm used initially does not generate the number of segments sought. Rather, a much larger number of segments is extracted. Then, the original data is discarded and only the centres of the resulting segments (centroids, representatives of each market segment) and segment sizes are retained, and used as input for the hierarchical cluster analysis. At this point, the data set is small enough for hierarchical algorithms, and the dendrogram can inform the decision how many segments to extract.

2.4.1 Two-Step Clustering

IBM SPSS (IBM Corporation 2016) implemented a procedure referred to as two-step clustering (SPSS 2001). The two steps consist of run a partitioning procedure followed by a hierarchical procedure. The procedure has been used in a wide variety of application areas, including internet access types of mobile phone users (Okazaki 2006), segmenting potential nature-based tourists based on temporal factors (Tkaczynski et al. 2015), identifying and characterising potential electric vehicle adopters (Mohamed et al. 2016), and segmenting travel related risks (Ritchie et al. 2017).

The basic idea can be demonstrated using simple R commands. For this purpose we use the artificial mobile phone data set introduced in Sect. 7.2.3. First we cluster the original data using k-means with k much larger than the number of market segments sought, here k = 30:

R> set.seed(1234) R> PF3.k30 <- stepcclust(PF3, k = 30, nrep = 10)

The exact number of clusters k in this first step is not crucial. Here, 30 clusters were extracted because the original data set only contains 500 observations. For large empirical data sets much larger numbers of clusters can be extracted (100, 500 or 1000). The choice of the original number of clusters to extract is not crucial because the primary aim of the first step is to reduce the size of the data set by retaining only one representative member of each of the extracted clusters. Such an application of cluster methods is often also referred to as vector quantisation . The following R command plots the result of running k-means to extract k = 30 clusters:

R> plot(PF3.k30, data = PF3)

This plot is shown in Fig. 7.19. The plot visualises the cluster solution using a neighbourhood graph. In a neighbourhood graph, the cluster means are the nodes, and are plotted using circles with the cluster number (label) in the middle. The edges between the nodes correspond to the similarity between clusters. In addition – if the data is provided – a scatter plot of the data with the observations coloured by cluster memberships and cluster hulls is plotted.

As can be seen, the 30 extracted clusters are located within the three segments contained in this artificially created data set. But because the number of clusters extracted is ten times larger (30) than the actual number of segments (3), each naturally existing market segment is split up into a number of even more homogeneous segments. The top right market segment – willing to pay a high price for a mobile phone with many features – has been split up in eight subsegments.

The representatives of each of these 30 market segments (centroids, cluster centres) as well as the segment sizes serve as the new data set for the second step of the procedure, the hierarchical cluster analysis. To achieve this, we need to extract the cluster centres and segment sizes from the k-means solution:

R> PF3.k30.cent <- parameters(PF3.k30) R> sizes <- table(clusters(PF3.k30))

Based on this information, we can extract segments with hierarchical clustering using the following R command:

R> PF3.hc <- hclust(dist(PF3.k30.cent), members = sizes)

Figure 7.20 contains the resulting dendrogram produced by plot(PF3.hc). The three long vertical lines in this dendrogram clearly point to the existence of three market segments in the data set. It cannot be determined from the hierarchical cluster analysis, however, which consumer belongs to which market segment. This cannot be determined because the original data was discarded. What needs to happen in the final step of two-step clustering , therefore, is to link the original data with the segmentation solution derived from the hierarchical analysis. This can be achieved using function twoStep() from package MSA which takes as argument the hierarchical clustering solution, the cluster memberships of the original data obtained with the partitioning clustering method, and the number k of segments to extract:

Hierarchical clustering of the 30 k-means cluster centres of the artificial mobile phone data set

R> PF3.ts3 <- twoStep(PF3.hc, clusters(PF3.k30), k = 3) R> table(PF3.ts3)

PF3.ts3 1 2 3 200 100 200

As can be seen from this table (showing the number of members in each segment), the number of segment members extracted matches the number of segment members generated for this artificial data set. That the correct segments were indeed extracted is confirmed by inspecting the plot generated with the following R command: plot(PF3, col = PF3.ts3). The resulting plot is not shown because it is in principal identical to that shown in Fig. 7.10.

The R commands presented in this section may be slightly less convenient to use than the fully automated two-step procedure within SPSS. But they illustrate the key strength of R: the details of the algorithms used are known, and the data analyst can choose from the full range of hierarchical and partitioning clustering procedures available in R, rather than being limited to what has been implemented in a commercial statistical software package.

2.4.2 Bagged Clustering

Bagged clustering (Leisch 1998, 1999) also combines hierarchical clustering algorithms and partitioning clustering algorithms, but adds bootstrapping (Efron and Tibshirani 1993). Bootstrapping can be implemented by random drawing from the data set with replacement. That means that the process of extracting segments is repeated many times with randomly drawn (bootstrapped) samples of the data. Bootstrapping has the advantage of making the final segmentation solution less dependent on the exact people contained in consumer data.

In bagged clustering, we first cluster the bootstrapped data sets using a partitioning algorithm. The advantage of starting with a partitioning algorithm is that there are no restrictions on the sample size of the data. Next, we discard the original data set and all bootstrapped data sets. We only save the cluster centroids (segment respresentatives) resulting from the repeated partitioning cluster analyses. These cluster centroids serve as our data set for the second step: hierarchical clustering. The advantage of using hierarchical clustering in the second step is that the resulting dendrogram may provide clues about the best number of market segments to extract.

Bagged clustering is suitable in the following circumstances (Dolnicar and Leisch 2004; Leisch 1998):

-

If we suspect the existence of niche markets .

-

If we fear that standard algorithms might get stuck in bad local solutions.

-

If we prefer hierarchical clustering , but the data set is too large.