Abstract

The Indonesian financial system has a long story. Financial system hardly existed before 1966 that is when the commercial banks faced the emergence time. After 1966 under Soeharto governance, central banking and banking sector regulation as the basis of the current financial system in Indonesia was introduced and implemented. After 17 years later, financial structure of Indonesia had the first reformation. In total, there are five phases in Indonesian financial system development between 1966 and the present time (Hamada in Transformation of the Financial Sector in Indonesia, 2003). The first phase, called as formative period, started from 1966 until 1972. The second phase, started from 1973 until 1982, is the period of policy-based finance under soaring oil prices. The third phase, started from 1983 until 1991, is financial-reform period. The fourth phase, started from 1992 until 1997, is the period of financial system’s expansion. The last phase, started from 1998 until present, is the period of financial restructuring, which is in this period the government more concern about consumer protection in financial industry. Financial consumer protection is necessary to increase access and usage of financial services. It can build trust between consumer and financial system, hence in encouraging financial inclusion.

Similar content being viewed by others

The Indonesian financial system has a long story. Financial system hardly existed before 1966 that is when the commercial banks faced the emergence time. After 1966 under Soeharto governance, central banking and banking sector regulation as the basis of the current financial system in Indonesia was introduced and implemented. After 17 years later, financial structure of Indonesia had the first reformation. In total, there are five phases in Indonesian financial system development between 1966 and the present time (Hamada 2003). The first phase, called as formative period, started from 1966 until 1972. The second phase, started from 1973 until 1982, is the period of policy-based finance under soaring oil prices. The third phase, started from 1983 until 1991, is financial-reform period. The fourth phase, started from 1992 until 1997, is the period of financial system’s expansion. The last phase, started from 1998 until present, is the period of financial restructuring, which is in this period the government more concern about consumer protection in financial industry. Financial consumer protection is necessary to increase access and usage of financial services. It can build trust between consumer and financial system, hence in encouraging financial inclusion.

1 Characteristics of Indonesian Financial Industry

The Financial service sector in Indonesia is one of the primary determinants of economic dynamics. It can be divided into three main subsectors, namely banking industry, capital market and the nonbank financial industry. Banking intermediation dominated the financial system compare to other subsectors, e.g. capital market and nonbank financial industry. The volume of the Indonesian capital market continues to be very small, carrying around 539 listed companies.

1.1 Recent Demographic Trends in Indonesia

Indonesia is one of populous country in the world and become the fourth largest country. It has the multitude of ethnic, cultural and linguistic varieties that can be found within the boundaries of a nation state that is the world’s largest archipelago. This section will discuss about a number of important aspects regarding Indonesia’s demographic composition include the recent demographic trends in Indonesia.

1.1.1 Total Population

The total populations of Indonesia increased to 258.32 million people in 2016 from 255.46 million people in 2015. This number represents 40% of the ASEAN countries’ total population (Graph 1) and 3.51% of the world’s total population. The total population of Indonesia continually increases every year and The United Nation (UN) was estimated that the total population of Indonesia will reach exceed 270 million people by 2025, exceed 285 million people by 2035 and exceed 290 million people by 2045. But UN estimated that this number would start decline after 2050.

Source tradingeconomics

ASEAN countries population in 2016. Note Data in million people.

The annual population growth rate of Indonesia stood at an average of 1.51% for the last 10 years, reaching an all time high of 2.66% in 2008 and record low of 1.27% in 2016 (Graph 2).

Source Indonesia Central Bureau of Statistic

Annual population growth of Indonesia in 2006–2016.

Based on data from Indonesia Central Bureau of Statistic, Indonesia faces the demographic transition towards a lower fertility rate and a lower mortality rate. Indonesians are now living longer, as indicated by a rise in life expectancy at birth from 70.8 in 2010, 72.7 in 2016 and expected to reach 73.3 in 2025.

1.1.2 Age Structure

A young population dominates the Indonesia’s demographic composition. This condition can be one of the strength for Indonesia, because this young population implies a potentially large workforce. Indonesia’s total median age is estimated 29.9 years. This indicates that one half of the population is older than 29.9 years, while the other half is younger than this figure. When divided in sexes the female median age is one year older (30.5 years) as compared to the male counterpart (29.3 years). Table 1 indicates the percentage shares of the Indonesian people categorized in five age groups and the corresponding division in sexes (in absolute numbers).

Moreover, the age and sex structure from Table 1 is illustrated as the population pyramid as the following picture (Fig. 1).

Figure 1 shows that in 2016, Indonesian population was relatively young with a dominant proportion of economically productive population aged between 15 and 64, whereas the old-age population was small in proportion.

Source CIA World Factbook

Population pyramid of Indonesia in 2016.

1.2 Characteristics of Indonesian Banking Industry

Banking industry in Indonesia is classified into commercial and rural banks. Classifications of commercial and rural bank are in the payment system and restriction in operational area. Rural bank cannot provide payment transaction services, accept deposits in the form of demand deposits or conduct business in foreign exchange, and commercial banks can do all. Based on statistic data from Otoritas Jasa Keuangan (2016a), there are 118 commercial banks and 1632 rural banks in November 2016 (Figs. 2 and 3).

Source Otoritas Jasa Keuangan (2016a)

Numbers and classification of commercial bank.

Source Otoritas Jasa Keuangan (2016a)

Number and classification of rural bank.

Since 2012, commercial banks were classified based on core capital and stipulates permitted activities for each classification, known as BUKU (Commercial Bank Based on Business Activities). Based on this classification, banks are classified into four classes, explained in the Table 2.

The assets of commercial and rural banks as of August 2016 at IDR 6165.89 and IDR 111.32 trillion respectively. In banking industry, there is a concentration with the top 5 banks accounting for just fewer than 50% of the sector’s assets.

1.3 Characteristics of Indonesian Non-bank Financial Institutions

Even though financial sector of Indonesia is dominated by banking, but the growth of non-bank financial institutions are also attractive. Non-banking financial institutions are composed of multiple categories of institutions regulated and supervised by OJK (Otoritas Jasa Keuangan/Indonesia Financial Services Authority). Based on statistic data from OJK, there are 136 insurance companies, 252 pension funds, 269 finance companies, 26 special finance service companies, 236 non-banking supporting service companies and 89 microfinance companies (Graph 3).

Source Otoritas Jasa Keuangan 2016b

Composition of non-banking institution as of September 2016.

1.3.1 Insurance

Indonesia, as the largest population among the ASEAN countries, is a big market for insurance companies (Global Business Guide Indonesia 2012). Insurance companies in Indonesia are divided into five types, namely general insurance, life insurance, reinsurance, social insurance and mandatory insurance. The form of insurance companies in Indonesia must be a limited liability company, co-operative or an existing mutual business (this form only applies to AJB Bumiputera 1912) (Table 3).

In 2016, insurance premium reached 340.7 trillion rupiah.

1.3.2 Microfinance Institution

Microfinance institutions provide financial intermediation for small-scale borrower in Indonesia. Microfinance services in Indonesia have been provided not only from one company but several institutions that can be divided into four types. Those types are formal, semiformal, informal and microcredit programs (Fig. 4; Table 4).

Source Otoritas Jasa Keuangan 2016b

Types of microfinance institutions in Indonesia.

There are 89 operating licensed-microfinance institutions with total assets of 283.84 billion rupiah.

2 Soft Infrastructure of Indonesian Financial Consumer Protection System

2.1 Law and Regulation on Financial Consumer Protection

The authority to supervise the implementation of the consumer protection mechanism by all financial services business players in Indonesia is hold by The Indonesia FSA, called as Otoritas Jasa Keuangan (Otoritas Jasa Keuangan 2016c). OJK will request the information and/or data related to the implementation of the consumer protection mechanism at any time from the financial services business player concerned.

2.1.1 Consumer Protection Law

OJK as the supervisor and regulator in the financial services sector define the financial consumer as parties that put their funds and/or utilize the services available at the Financial Services Institutions. The financial consumers include banking customers, capital market investors, insurance policyholders, and Pension Fund participants, based on the laws and regulations in financial services sector.

On 6 August 2013, OJK issued regulation No. 1/POJK.07/2013 concerning Consumer Protection in the Financial Services Sector. This regulation is an implementing regulation for article 31 of law No. 21/2011 regarding on protecting of the public and consumer. It applies to all financial services business players, e.g. commercial banks, securities companies, insurance companies, and other financial institutions. The regulation describes definition and obligations of financial services business players in consumer protection, how to attend complaints and settlement mechanism, as well as the supervisory role of OJK in consumer protection.

Beside that, Central Bank of Indonesia has also issued regulation about consumer protection in the payment services system, namely the Governor of Indonesian Bank’s Regulation Number 16/1/PBI/2014.

2.1.2 Product and Price Regulation

The participation of government in competition is protecting public interest. Thus, the government needs to implant a full-fledged the public understanding about the fair competition in business. The Law Prohibiting Monopolistic Practice and Unfair Competition introduced in the beginning of 1998 and sponsored by the IMF. Law of the Republic of Indonesia No. 5/1999 concerning the Anti Monopoly Law was issued in March 1999. This law used to correct monopolistic abuses by private family-controlled conglomerates that rose during the new order (1966–1998) (Maarif 2001).

The entity in developing and applying the Law No. 5/1999 is The Business Competition Supervisory Commission, known as KPPU (Komisi Pengawas Persaingan Usaha). KPPU has an authority to issue guidelines on the application of specific article in the law.

Law No. 5/1999 article 5 defines some prohibited agreement and one of them is pricing agreement, i.e. price-fixing agreement and other pricing practices between competing business players. Price-fixing may exempt if the price within the framework of a joint venture or mandated by law. Also, competing business players are prohibited to set prices below the market price or impose a predatory price (KPPU guideline No. 6/2011) as if it causes unfair business competition or monopolistic practices. Minimum resale price maintenance is also prohibited if it caused unfair competition (KPPU guideline No. 8/2011).

2.1.3 Anti-trust Competition Laws

Indonesia’s principal competition law No. 5/1999 concerning Prohibition of Monopolistic Practices and Unfair Business Competition has proposed to be amended by parliamentary in June 2016. Antitrust enforcement has targeted domestic cartels and transactions. Competing business players are not allowed to establish a cartel to regulate the production and/or marketing of product or a trust if it may cause unfair competition and/or monopolistic practices. According to KPPU guideline on cartel No. 04/2010, there are several indicators may lead a cartel:

-

(a)

Small number of business actors and high concentration market

-

(b)

Comparable size of those business actors

-

(c)

Homogeneous products

-

(d)

Multiple contacts between competitors

-

(e)

Overstock/oversupply of products

-

(f)

Affiliation between competitors

-

(g)

High entry barriers

-

(h)

Stable and inelastic demand

-

(i)

Buyers have no counter-vailing power

-

(j)

There is regular information exchange between competitors

-

(k)

There is a regulated price or contract.

2.2 Policies on Financial Consumer Protection

2.2.1 Customer Account Management

Financial service institutions need to provide their customer about their consumer’s account but as permission of their customer. Banks currently do not have an obligation to issue or provide a monthly statement for customer unless they give an authorization to the bank. Financial Services Authority regulation No. 1/POJK.07/2013 concerning consumer protection in financial sector article 27 stated that the financial service providers have to send reports to the consumers regarding the balance position and deposit movements, funds, assets, or liabilities of the Consumers accurately, on timely basis and in the manners or means according to the agreement with the Consumers.

2.2.2 Disclosure and Sales Practices

There are no specific items of information that should be included for the different types of financial products or any requirement of a product even though there are some provisions requiring disclosure of terms and conditions of products. The disclosure requirements in financial consumer protection law do not adequately deal with these issues given the generality of the requirements in provisions e.g. articles 4 and 8.

In banking industry, the banking regulation allows exceptions to maintain secrecy regarding the deposits of any depositor. It includes provisions allowing certain disclosures for tax purposes in relation to deposit and depositor information, to settle a bank’s claims (in respect of a depositor) that have been transferred to the Agency for State Loan Settlement and Auction or to the Committee for State Loan Settlement; and to assist in respect of a criminal case involving the depositor; for or the purposes of civil suits; as required by the Anti-Money Laundering Law and a board of directors of a bank may disclose a customer’s financial information to other banks.

In capital market industry, capital market institutions can give an impact to investor in investment decision and performance. Therefore, disclosure about these entities is important to give full information about investors’ investment and the entity with whom they are doing business. It is recognized in the rule V.H.1 related to investment advisors that need to disclose the information if other entities or parties prepared research reports to their clients.

Related to disclosure and sales practice, financial service institutions should sell their product with accurate, honest, clear and not misleading information about its products and/or services. It is stated in Financial Services Authority regulation No. 1/POJK.07/2013 concerning consumer protection in financial sector article 4. Further, information shall be delivered to the customers regarding their rights and obligations when giving an explanation and making an agreement. Thus, various media through advertisement in print or electronic media should state the information. Still the same regulation article 17, it states that The Financial Services Providers are prohibited to use marketing strategy of the products and/or services that can harm the Consumers by taking advantage of the Consumers’ condition which does not have other choice when making a decision.

2.2.3 Financial Literacy and Education

OJK issued Circular Letter PUJK. SEOJK No. 1/SEOJK.7/2014 concerning the Education Implementation Plan to Enhance Financial Literacy towards the Consumer and/or Society stipulates that every financial service institutions have to include education plans in their annual business plan and obliges them to report its implementation to OJK. According to the OJK Commissioner in charge of Consumer Education and Protection, the arrangement of an education plan needs to refer to the Strategy of National Financial Literacy published by the President of Indonesia in November 2013 (Otoritas Jasa Keuangan 2015). All education plans together with annual business plans have to be submitted to the supervisory board of OJK in 2015.

2.2.4 Dispute Resolution Mechanism

There are two statutory dispute settlement systems in financial service sectors, the Consumer Dispute Resolution Board/Badan Penyelesaian Sengketa Konsumen (BPSK) and Central Bank of Indonesia mediation service. BPSK operates under regulation of Ministry of Trade and Industry no. 350/2001 and BI mediation service operates under the Banking Mediation Regulation No. 8/2006.

Further, Indonesia OJK as a regulator provides a procedure to dispute resolution mechanism. On 23 January 2014, OJK issued regulation No. 1/POJK.07/2014 concerning alternative dispute settlement institutions in the financial service sector. This regulation governs the function and the establishment of independent institutions that are appointed by OJK to solve any dispute that has occurred between consumers and Financial Services Institutions or through alternative dispute resolution mechanism. Indonesia also participates in ASEAN committee on Consumer Protection that gives an avenue for consumers to complain and seek compensation for loss.

There are six alternative agencies to manage mediation in financial services sector mandated under OJK regulation No. KEP-01/D.07/2016 dated on 21 January 2016 (Pengumuman 2016), namely Alternative Dispute Resolution (ADR) agencies. The official list of ADR agencies are as follows:

-

1.

The Insurance Arbitration and Mediation Agency (Badan Mediasi dan Arbitrase Asuransi Indonesia—BMAI) is one of service provided by the Life and General Insurance Associations to give a comprehensive mediation and adjudication service.

-

2.

The Indonesian Capital Markets Arbitration Agency (Badan Arbitrase Pasar Modal Indonesia—BAPMI) provides mediation and adjudication service in capital market.

-

3.

The Pension Fund Mediation Agency (Badan Mediasi Dana Pensiun—BMDP) provides mediation service in pension fund.

-

4.

The Indonesian Alternative Dispute Resolution Institution for The Banking Sector (Lembaga Alternatif Penyelesaian Sengketa Perbankan Indonesia—LAPSPI) provides mediation service in banking sector.

-

5.

The Indonesian Arbitration and Mediation Agency for Underwriting Companies (Badan Arbitrase dan Mediasi Perusahaan Penjaminan Indonesia—BAMPPI) provides mediation and arbitration service in underwriting companies.

-

6.

The Indonesian Financing and Pawnshop Mediation Agency (Badan Mediasi Pembiayaan dan Pegadaian Indonesia—BMPPI) provides mediation service in financing and pawnshop companies.

ADR agencies above have their own distinct legal characteristics and implications. These agencies provide mediation, adjudication and arbitration to resolve complaints from consumers. In general, there are two mechanisms to handle the complaints from financial consumers, i.e. Internal Dispute Resolution (IDR) and External Dispute Resolution (EDR).

-

1.

Internal Dispute Resolution (IDR) Mechanism

This mechanism obliges financial services business players to solve their consumers’ complaints through giving the functions or units to deal with the complaints.

-

2.

External Dispute Resolution (EDR) Mechanism

EDR is needed when consumers fail to reach agreements with financial services business players over their complaints. In this mechanism, consumers can contact one of the following institutions:

-

(a)

The OJK

Since 2013, OJK has handled 3832 complaints and resolved 3574 complaints as the following (Table 5):

Table 5 Complaints handled by FSA in 2016 -

(b)

Alternative Dispute Resolution Agencies (ADR agencies)

Consumers can contact ADR agencies to mediate, adjudicate and arbitrage their cases. Since January 2016 to June 2016, ADR agencies has handled 47 cases and resolved 29 cases with the detail as the following (Table 6).

Table 6 Cases handled by ADR agencies in 2016 The procedure to handle complaints are visualized as the Graph 4.

Graph 4

Source Author, OJK and other sources

Complaint and dispute resolution procedures.

Under OJK regulation No. 1/POJK.07/2014, every financial services business players have to take further steps and settle all complaints from customers within 20 business days. In some cases, the settlement of complaints may be extended for further 20 business days and consumers must get notification about the time extension. The financial services business players are also required to report to OJK every quarter all complaints received from their consumers and also mechanism used to settle the complaints.

-

(a)

2.2.5 Guarantee Schemes and Insolvency

Indonesia already has a depositor protection scheme. Since 1 January 2014, OJK and The Indonesia Deposit Insurance Corporation (IDIC) became the parties who have empowered to take all measures to protect depositors when a bank proved unable to meet its obligations. Based on IDIC law act No. 24/2004, IDIC has two key functions: to insure customer deposits and to carry out the resolution of failed banks. Moreover, the IDIC law states that IDIC is designated as the insurer, and every commercial and rural bank must be a member of the deposit insurance program and pay a yearly membership fee from its own equity at the end of the previous fiscal year.

Based on IDIC regulation No. 2/PLPS/2010 deposit insurance covers a total of 2 billion rupiah on deposit by any individual in any member bank and maximum fair interest rate on deposit account at 7% for an account denominated in rupiah and 1.5% for an account denominated in foreign currency. The guarantee covers demand deposits, certificates of deposits, saving accounts, time deposits and deposits in other equivalent form on a per customer, per account basis for each bank (Fig. 5).

Source OJK

Financial system coordination forum.

Related to insolvency, the law No. 24/2004 concerning Indonesia Deposit Insurance Corporation states that depositor will enjoy higher priority compared to other unsecured creditors in the liquidation process of a bank. If the coverage given by IDIC is inadequate, the IDIC law sets out the hierarchy of payments to creditors from the disposal of assets and/or the collection of receivables. The order, stated in article 54, is as follows:

-

1.

Accrued and unpaid remuneration for staff

-

2.

Severance payment for staff

-

3.

Judicial fees and court charges, cost unpaid auction expenses and cost of operational expenses

-

4.

Resolution cost incurred by the IDIC

-

5.

Unpaid taxes

-

6.

Uninsured portion of deposits and ineligible deposits

-

7.

Other creditors.

Moreover, the IDIC law gives expeditious, cost effective and equitable provisions to enable the maximum timely refund of deposits to depositors.

3 Hard Infrastructure of Indonesian Financial Consumer Protection System

3.1 Indonesia Financial Service Authority (Otoritas Jasa Keuangan)

Otoritas Jasa Keuangan (OJK, hereinafter) is an independent state agency responsible for conducting integrated regulation and supervision system of all activities in the financial service sector including banking, capital market, insurance, pension fund, financing companies, and other type of financial institutions. Since the establishment of OJK by Law Number 21 Year 2011 (Law 21/2011), the capital market and non-bank financial institutions supervision duty has been transferred from Ministry of Finance to OJK on 31 December 2012. Meanwhile, Central Bank’s authority to conduct banking supervision has been fully shifted to OJK by 31 December 2013. OJK started to regulate and supervise microfinance institutions since 2015.

The establishment of OJK is expected to improve nation’s competitiveness by supporting the development of Indonesia financial service sector. According to Article 4 Law 21/2011, OJK shall be established to create a well organized, fair, transparent, accountable financial service sector and capable to implement a sustainable and stable financial system, as well as to be able to protect the interest of consumers and the community. OJK performs its duties and responsibilities based on good governance principles, namely independency, accountability, responsibility, transparency, and fairness. The consumer protection term is relatively new in the financial sector supervision. OJK is the first financial supervision body in Indonesia that included consumer protection into its main purpose.

OJK implements consumer protection through market conduct regulation and supervision. Market conduct supervision balances the financial sector development and the fulfillment of consumer’s right and obligation in order to increase consumer confidence. Market conduct itself is the behavior of financial service providers (PUJK, hereinafter) in designing, setting, disseminating information, offering, making agreement related to products and/or services as well as dispute resolution and complaint handling. Regarding that matter, consumer protection program led to achieve two main objectives. First, is to increase market confidence in all business activities in the financial service sector. Second, provide opportunities for a fair, efficient and transparent development of financial while also ensuring consumer understanding of their rights and obligations related to financial products and/or services. These two objectives are required to maintain financial stability, growth, efficiency, and innovation in long term.

Several factors underlying the need of market conduct supervision in Indonesia. Low financial literacy index reflects consumer in financial sector have a low level of knowledge regarding financial products and services. In this case, consumers are very prone to asymmetric information problem because financial institutions and consumer are not in the same level of playing field. The probability of misconduct by PUJK is usually higher when consumer has a low financial knowledge, in the end leads to higher probability of default. Some misconduct cases in financial service sector are quite often to be found in Indonesia such as predatory lending, personal information theft, and misleading advertisement. The next part of this chapter will discuss about some sample cases of financial service misconduct in Indonesia. OJK Regulation Number 1 Year 2013 on Consumer Protection in Financial Service Sector (POJK No. 1/2013) and OJK Regulation Number 1 Year 2014 on Alternative Dispute Resolution Body in Financial Service Sector (POJK No. 1/2014) along with OJK form letters on consumer protection are the regulatory frameworks of consumer protection in the financial service sector.

Apart from setting up the regulatory frameworks, Education and Consumer Protection Division in OJK also undertakes financial literacy program. The objectives of conducting education for financial services consumer is to increase the level of consumer understanding of financial products and services. Financial well-literate consumer is a substantial element to increase market confidence and consumer’s utility in the financial service sector. PUJK are required to submit financial education activity report to OJK. Financial education activities shall not only include product information but also include education on financial planning, investment planning, preparation of financial statements, or any other type of financial education.

POJK No. 1/2013 also emphasizes on complaint handling and dispute resolution mechanism. Regarding that matter, PUJK are obliged to:

-

a.

Create a division/unit to handle consumer complaints, equipped with reliable adequate personnel and standard operating procedures

-

b.

Submit quarterly report regarding consumer complaint handling

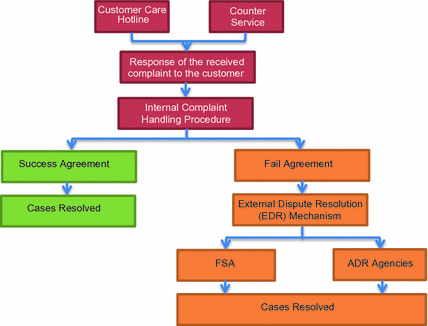

OJK also regulates complain handling through OJK Form Letter Number 2/SEOJK.07/2014 (SE No. 2/SEOJK.07/2014) as follows (Fig. 6).

Source OJK

Complaint handling mechanism according to SE No. 2/SEOJK.07/2014.

3.2 Central Bank of Indonesia (Bank Indonesia/BI)

Bank Indonesia in an independent central bank as enacted by the new Central Bank Act Number 23 Year 1999 (UU No. 23/1999). As and independent state institution, Bank Indonesia is fully autonomous and free from interference by the government or any other external parties in conducting and implementing its task and policy. Bank Indonesia has a single objective of achieving and maintaining stability of Rupiah. The stability of nation’s currency consists of two aspects, currency stability against goods and services, and currency stability against other currencies. The first aspect is reflected in the rate of inflation, while the second aspect is depicted by the Rupiah exchange rate against other currencies. In pursuing its single objective, Bank Indonesia is supported by three main pillars that represent task division. The pillars are formulating and implementing monetary policy, regulating and ensuring a smooth payment system, and financial system stability. Bank Indonesia integrates these three pillars in maintaining a stable value of Rupiah effectively and efficiently (Fig. 7).

Source Bank Indonesia (2017a)

Objectives and function of Bank Indonesia.

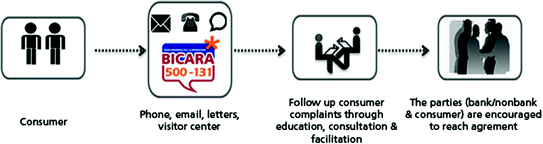

This chapter focuses on the second pillar, regulating and ensuring a smooth payment system. In the pursuit of smooth, safe, efficient, and reliable payment system, Bank Indonesia shall also maintain access expansion, consumer protection, and national interest. Bank Indonesia focuses its consumer protection aspect in payment system while OJK focuses in market conduct supervision. The current rapid technological development creates various ranges of innovations that enable people to conduct payment system transactions anywhere and anytime. At the same time, consumer should be provided with adequate and accurate information regarding the benefit and risk of payment system to mitigate misconduct risks. In response to those needs, Bank Indonesia established Payment System Consumer Protection Division in August 2013 and issued the regulatory framework on consumer protection in payment system is PBI No/16/1/PBI/2014 in 2014.

The payment system services and/or products within the scope of payment system consumer protection are: (a) issuance of fund transfer instruments and/or withdrawal of funds; (b) funds transfer; (c) card based payment instrument (ATM/debit card and credit card); (d) electronic money; (e) providing and/or depositing Rupiah banknotes; and (f) other payment system services determined in BI regulations. Payment system consumer protection division has three functions as explained below:

-

a.

Education

Bank Indonesia conducts education program on payment system products through various media. The education program aimed at academics, students, housewives, payment system providers, and public in general.

-

b.

Consultation

Bank Indonesia provides consultation on payment system issues from public and payment system providers via telephone, email, mail, and Bank Indonesia offices.

-

c.

Facilitation

Bank Indonesia facilitates dispute resolution between consumer and payment system provider through mediation between two parties to resolve the problem (Fig. 8).

Fig. 8

Payment system consumer protection mechanism

3.3 Indonesia Deposit Insurance Corporation (Lembaga Penjamin Simpanan)

Deposit insurance plays an important role as an element of financial safety net. Deposit insurance acts as a “lender of last resort”, to minimize financial and social impact of in the time of banking crisis. The existence of explicit deposit insurance can significantly decrease the likelihood of bank runs or even put an end to runs altogether in countries with solid institutions (McCoy 2007). In addition to that, deposit insurance also provide compensations to small-scale depositors in the case of bank failures (Hoelscher et al. 2006). Many countries in almost all regions have adopted depositor insurance, with a significant increase in the number of adopters in the 1990s and 2000s (Bank Indonesia 2017a, Demirgüç-Kunt et al. 2008).

Prior to the 1997/1998 Asian Financial Crisis, Indonesia government adopted an implicit deposit guarantee. There was no specific institution/agency assigned as deposit insurance at that moment, it was believed that the financial industry was quite strong after the economic boom in 1970s. Under Soeharto’s centralized regime, government would provide assistance to save troubled banks in order to maintain country’s financial stability. The Asian Financial Crisis apparently has provided valuable lessons for Indonesia. The provision of blanket guarantee, not only created serious moral hazard but also burden for state budget. Considering those two major drawbacks of blanket guarantee schemes and as a part of IMF assistance in rescuing the national financial system, Indonesia implemented an explicit deposit protection schemes in early 2000s. There is a clear difference between implicit and explicit deposit protection schemes. Under the implicit deposit protection schemes, there are no stated rules but only obvious intention by the government to save financial institutions from crisis. On the contrary, explicit deposit protection schemes clearly state terms and conditions of the scheme.

Indonesia government enacted the Indonesia Deposit Corporation (IDIC) Law on 22nd September 2004 after the approval of the parliament. The IDIC was established on 22nd September 2005 with two main responsibilities, providing guarantee of bank’s depositors and actively participating in maintaining the stability of the banking system. After its establishment, the level of IDIC coverage was gradually adjusted as follows:

IDIC insures deposits in all conventional banks and Islamic banks operating in the Republic of Indonesia. The IDIC membership is mandatory to all banks including foreign bank branches and subsidiaries. However, IDIC does not cover overseas branches of Indonesian banks. IDIC’s coverage including all type of deposits such as saving account, current account, certificate of deposit, and time deposit denominated in Indonesian Rupiah and foreign currencies. IDIC funding comes from initial capital contributed by Indonesia government, membership contribution paid once when a bank becomes IDIC member, and insurance premiums paid twice a year. Until December 2016, there are 104 conventional banks and 13 Islamic banks registered as IDIC members.

The following Table 7 shows deposit distribution in Indonesia based on the amount of deposits in Rupiah. Based on the deposit distribution data on December 2016, 97.84% of the bank accounts in Indonesia have less than Rp100 million in their deposits. This figure shows the characteristic of depositors in Indonesia banking industry that is dominated by small-scale depositors. More than 99% of bank accounts, with deposit up to Rp2 billion, are insured by the IDIC. As of December 2016, the amount of deposit covered by the IDIC reached Rp2.180.713 billion. The deposit guarantee scheme by the IDIC is expected to provide consumer protection, particularly small-scale depositors, in case of a troubled bank.

In order to be eligible-to-be-paid insured deposit, deposit has to meet three main criteria. Firstly, it has to be recorded on bank’s book. Secondly, interest rate on the deposit should not be higher than IDIC maximum interest rate limit. IDIC adjusts its interest rate limit frequently to response the changing macroeconomic conditions. Thirdly, the account holder should not be engaged in an action that cause any harm to the bank. In the event of a bank declared as a failed bank IDIC has options to rescue the bank or pay insured deposits. IDIC will do verification and aggregation in 90 days or less to determine eligible depositors and amounts to be paid. Depositors start to receive their payment after the fifth day of verification and aggregation process (Table 8).

3.4 Indonesia Securities Investor Protection Fund

As part of OJK’s responsibility to create a fair, well-regulated, and efficient capital market and to implement consumer protection in capital market, Indonesia Securities Investor Protection Fund (Indonesia SIPF) was established in 2012. Prior to Indonesia SIPF establishment, a study conducted by OJK recommended that the existence of investor protection fund could boost investor confidence in Indonesia capital market. Investor confidence is one of the important elements in the development of a capital market. Indonesia SIPF was established by three shareholders, consist of Indonesia Stock Exchange, Kliring Penjamin Efek Indonesia, and Kustodian Sentral Efek Indonesia. All of Indonesia SIPF shareholders are self-regulatory organizations in Indonesia capital market. The Indonesia SIPF membership is mandatory to all brokers, dealers, and custodian banks. Members are obliged to pay initial membership fee Rp100 million (only paid once during the registration) and annual membership fee 0.001% of monthly average of investor’s assets in the prior year.

Indonesia SIPF’s core mission is to intensify the capital market investment security by establishing investor protection fund. Indonesia SIPF protects investors from losing their assets if the custodian banks or brokers/dealers failed to return the assets to the investors. Investors are not charged any fee by Indonesia SIPF to be covered under this protection scheme. In the case of Indonesia SIPF member failed to return investor’s asset, investors reserve the right to get up to Rp100 million per investor and custodian banks entitled to claim up to Rp50 billion per bank. Indonesia SIPF sets three main criteria to determine eligible investor in the protection scheme as follows:

-

a.

Investor invests their fund and has an account at SIPF member

-

b.

Investor is registered by SIPF member on a sub-account at KSEI

-

c.

Investors has a single investor identification number from SIPF member.

Indonesia SIPF covers investor assets regardless of investor’s nationality or country of residence. As long as investor assets are registered in Indonesia SIPF member account. Indonesia SIPF protection scheme is not applicable to investor that falls into one of these criteria:

-

a.

Investor is engaged in any action that causing the loss of assets;

-

b.

Investor is majority shareholder, board of directors, board of commissioners, or one level below board of directors officials of custodians; and

-

c.

Investor is affiliated to any parties as mentioned in point a and b.

Investors and Indonesia SIPF should report any loss events to OJK, because all SIPF members (brokers/dealers and custodian banks) are under OJK’s supervision. OJK verifies the asset loss report using three criteria as follows:

-

a.

Investor asset loss occurs;

-

b.

Custodian failed to repay the lost assets;

-

c.

Custodian is unable to continue its operation and its business license is under consideration to be revoked.

If the event meets those criteria, OJK will issue a legal written statement to Indonesia SIPF. The next step is internal verification by Indonesia SIPF before making payments for asset loss claims. Indonesia SIPF has set the formula to determine the lost asset value as follows:

-

Assets in the form of equity

= number of securities (in unit) * average closing price (where transaction exists for the last six months prior to the issuance of OJK written statement

-

Assets in the form of debt instrument or Sukuk

= number of securities (in unit) * average fair market price issued by the bond pricing agency in the last six months

-

The value of asset in any form other than the aforementioned is calculated using fair asset pricing method

As of February 3, 2017, Indonesia SIPF has been managing Rp126 billion in investor protection fund. The investor asset value covered by Indonesia SIPF has reached Rp3.576 billion. Indonesia SIPF members consist of 19 custodian banks and 108 brokers/dealers with 660.796 securities sub-accounts (SIPF 2017).

References

Bank Indonesia. 2017a. “Objectives and Tasks of Bank Indonesia.” Retrieved from http://www.bi.go.id/en/tentang-bi/fungsi-bi/tujuan/Contents/Default.aspx

Bank Indonesia. 2017b. “Payment System Services Consumer Protection.” Retrieved from http://www.bi.go.id/en/sistem-pembayaran/di-indonesia/perlindungan/Contents/Default.aspx

Berlinawati, Santi. 2016. Emerging Insurance Market in Indonesia. http://www.globalindonesianvoices.com/28734/emerging-insurance-market-in-indonesia/

Demirgüç-Kunt, A., Kane, E. J., & Laeven, L. (2008). Determinants of deposit-insurance adoption and design. Journal of Financial Intermediation, 17(3), 407–438.

Financial Services Authority Regulation No. 1/POJK.07/2013 concerning consumer protection in financial services sector.

Garcia, Gillian G. H. 1999. “Deposit Insurance: A Survey of Actual and Best Practices.” IMF Working Paper No. 99/54.

Global Business Guide Indonesia. 2012. The Prospects for Indonesia’s Insurance Industry.

Hamada, Miki. 2003. Transformation of the Financial Sector in Indonesia. IDE Research Paper No. 6

Hoelscher, David S., Michael Taylor and Ulrich H. Klueh. 2006. The design and implementation of deposit insurance systems. Washington, D.C.: International Monetary Fund.

Indonesia SIPF. 2017. “Investor Protection Fund Statistics as of February 3, 2017.” Retrieved from www.indonesiasipf.co.id

Law of The Republic of Indonesia No. 5/1999 concerning the ban on monopolistic practices and unfair business competition.

Lembaga Penjamin Simpanan. 2017. “Deposit Distribution of Indonesian Commercial Banks as of December 2016.” Retrieved from http://www.lps.go.id/documents/830952/0/Statistik+%28Website%29-Desember+2016.pdf/92be6225-e599-4f6f-ad6e-951a8f0a9040www.ojk.go.id

Maarif, Syamsul. 2001. Competition Law and Policy in Indonesia. Jakarta

McCoy, Patricia A. 2007. “The Moral Hazard Implications of Deposit Insurance: Theory and Evidence.” Presented in Seminar on Current Developments in Monetary and Financial Law Washington, D.C., October 23–27,2006

Otoritas Jasa Keuangan. 2015. “Pemberdayaan Konsumen dan Peningkatan Kapasitas Perlindungan Konsumen di Sektor Jasa Keuangan.” Presented in Jakarta, 10 Maret 2015

Otoritas Jasa Keuangan. 2016a. Laporan Triwulanan: Triwulan III - 2016

Otoritas Jasa Keuangan. 2016b. Statistik Perbankan Indonesia. Vol. 14 No. 012.

Otoritas Jasa keuangan. 2016c. Indonesian Financial Services Sector Master Plan 2015–2016: Fostering Growth and Addressing Challenges in the Financial Services Sector, Today and Tomorrow.

Pengumuman No. PENG-1/D-07/2016 tentang Daftar Lembaga Alternatif Penyelesaian Sengketa di Sektor Jasa Keuangan

Author information

Authors and Affiliations

Corresponding author

Editor information

Editors and Affiliations

Rights and permissions

Copyright information

© 2018 Springer Nature Singapore Pte Ltd.

About this chapter

Cite this chapter

Rokhim, R., Adawiyah, W., Faradynawati, I.A.A. (2018). Financial Consumer Protection in Indonesia: Towards Fair Treatment for All. In: Chen, TJ. (eds) An International Comparison of Financial Consumer Protection. Springer, Singapore. https://doi.org/10.1007/978-981-10-8441-6_7

Download citation

DOI: https://doi.org/10.1007/978-981-10-8441-6_7

Published:

Publisher Name: Springer, Singapore

Print ISBN: 978-981-10-8440-9

Online ISBN: 978-981-10-8441-6

eBook Packages: Economics and FinanceEconomics and Finance (R0)