Abstract

Style analysis models aim to decompose the performance of a financial portfolio with respect to a set known indexes. Quantile regression offers a different point of view on the style analysis problem as it allows the extraction of information at different parts of the portfolio returns distribution. Moreover, the quantile regression results are useful in order to estimate the portfolio conditional returns distribution.

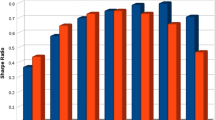

All computation and graphics were done in the R language (www.r-project.org) [R07] using the basic packages and the additional mgcv [WOO06] and quantreg packages [KOE07].

Access this chapter

Tax calculation will be finalised at checkout

Purchases are for personal use only

Preview

Unable to display preview. Download preview PDF.

Similar content being viewed by others

References

Attardi, L., Vistocco D.: Comparing financial portfolios style through quantile regression, Statistica Applicata, 18(2) (2006)

Basset, G. W., Chen, H. L.: Portfolio Style: Return-Based Attribution Using Quantile Regression. In: Fitzenberger B., Koenker R. and Machado J. A. R (eds) Economic Applications of Quantile Regression (Studies in Empirical Economics). Physica-Verlag, 293–305 (2001)

Elton, E. J., Gruber, M.J.: Modern Portfolio Theory and Investment Analysis. John Wiley & Sons, Chichester (1995)

Koenker, R.: Quantile Regression. Econometric Soc. Monographs (2005)

Koenker, R.: quantreg: Quantile Regression. R package version 4.06. http://www.rproject.org (2007)

R Development Core Team: R: A language and environment for statistical computing. R Foundation for Statistical Computing, Vienna, Austria. ISBN 3-900051-07-0, URL http://www.R-project.org (2007)

Merril Lynch: MLIndex System, http://www.mlindex.ml.com (2006)

Sharpe, W.: Asset Allocation: Management Styles and Performance Measurement. The Journal of Portfolio Management (1992)

Sharpe, W.: Determining a Fund’s Effective Asset Mix. Investment Management Review, vol. 2, no. 6, December: 59–69 (1998)

Wood, S. N.: Generalized Additive Models: An Introduction with R. Chapman and Hall/ CRC (2006)

Author information

Authors and Affiliations

Editor information

Editors and Affiliations

Rights and permissions

Copyright information

© 2008 Springer, Milan

About this paper

Cite this paper

Attardi, L., Vistocco, D. (2008). Estimating Portfolio Conditional Returns Distribution Through Style Analysis Models. In: Perna, C., Sibillo, M. (eds) Mathematical and Statistical Methods in Insurance and Finance. Springer, Milano. https://doi.org/10.1007/978-88-470-0704-8_2

Download citation

DOI: https://doi.org/10.1007/978-88-470-0704-8_2

Publisher Name: Springer, Milano

Print ISBN: 978-88-470-0703-1

Online ISBN: 978-88-470-0704-8

eBook Packages: Business and EconomicsEconomics and Finance (R0)