Abstract

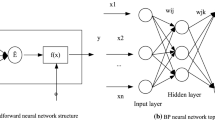

Due to the complexity of economic system, the interactive effects of economic variables or factors on Chinese foreign trade make the prediction of China’s foreign trade extremely difficult. To analyze the relationship between economic variables and foreign trade, this study proposes a novel nonlinear ensemble learning methodology hybridizing nonlinear econometric model and artificial neural networks (ANN) for Chinese foreign trade prediction. In this proposed learning approach, an important econometrical model, the co-integration-based error correction vector auto-regression (EC-VAR) model is first used to capture the impacts of the economic variables on Chinese foreign trade from a multivariate analysis perspective. Then an ANN-based EC-VAR model is used to capture the nonlinear patterns hidden between foreign trade and economic factors. Subsequently, for introducing the effects of irregular events on foreign trade, the text mining and expert’s judgmental adjustments are also incorporated into the nonlinear ANN-based EC-VAR model. Finally, all economic variables, the outputs of linear and nonlinear EC-VAR models and judgmental adjustment model are used as another neural network inputs for ensemble prediction purpose. For illustration, the proposed ensemble learning methodology integrating econometric techniques and artificial intelligence (AI) methods is applied to Chinese export trade prediction problem.

Chapter PDF

Similar content being viewed by others

Keywords

References

China’s Future. Fortune. (September 29, 1999)

Center of China Study: Development, Cooperation, Reciprocal and Mutual Benefit: The Evaluation of International Monetary Fund on Chinese Loan (1981-2002). Research Report (2004)

Engle, R.F., Granger, C.W.J.: Co-integration and Error-correction: Representation, Estimation and Testing. Econometrica 55, 251–276 (1987)

Hendry, D.F., Ericsson, N.R.: An Econometric Analysis of U.K Money Demand in Monetary Trends in the United States and the United Kingdom by Milton Friedman and Anna J. Schwartz. American Economic Review 81, 8–38 (1991)

Hornik, K., Stinchocombe, M., White, H.: Multilayer Feedforward Networks are Universal Approximators. Neural Networks 2, 359–366 (1989)

White, H.: Connectionist Nonparametric Regression: Multilayer Feedforward Networks can Learn Arbitrary Mappings. Neural Networks 3, 535–549 (1990)

Yu, L., Wang, S.Y., Lai, K.K.: A rough-Set-Refined Text Mining Approach for Crude Oil Market Tendency Forecasting. International Journal of Knowledge and Systems Sciences 2(1), 33–46 (2005)

Sullivan, D.: Document Warehousing and Text Mining: Techniques for Improving Business Operations, Marketing, and Sales. Wiley, New York (2001)

Yu, L., Wang, S.Y., Lai, K.K.: A Novel Nonlinear Ensemble Forecasting Model Incorporating GLAR and ANN for Foreign Exchange Rates. Computers & Operations Research 32, 2523–2541 (2005)

Author information

Authors and Affiliations

Editor information

Rights and permissions

Copyright information

© 2007 Springer Berlin Heidelberg

About this paper

Cite this paper

Yu, L., Wang, S., Lai, K.K. (2007). A Hybrid Econometric-AI Ensemble Learning Model for Chinese Foreign Trade Prediction. In: Shi, Y., van Albada, G.D., Dongarra, J., Sloot, P.M.A. (eds) Computational Science – ICCS 2007. ICCS 2007. Lecture Notes in Computer Science, vol 4490. Springer, Berlin, Heidelberg. https://doi.org/10.1007/978-3-540-72590-9_14

Download citation

DOI: https://doi.org/10.1007/978-3-540-72590-9_14

Publisher Name: Springer, Berlin, Heidelberg

Print ISBN: 978-3-540-72589-3

Online ISBN: 978-3-540-72590-9

eBook Packages: Computer ScienceComputer Science (R0)