Abstract

In the following model we propose a simple change to the nonlinear Hicksian trade cycle model of 1950 through just internalizing capital stock. This brings no alien elements into the model, it just makes explicit what is there already, i.e., investment, considering that capital is the cumulative sum of successive investments. This makes it possible to tie the “floor” disinvestment to capital stock through its depreciation rate. The consequence is that one can dispense with the exogenous floor (constant, or growing) altogether. Through capital accumulation the model produces an endogenous growth trend, more explicitly, growth cycles around a trend. Thus also the Hicksian autonomous growth trend can be dispensed with, and the model becomes self contained. A problem then may seem to be that without these exogenous trends the growing variables, income and capital, cannot be reduced to stationarity through trend elimination. A new method, proposed by the author 55 years ago, which we call relative dynamics, replaces the growing income by the income growth factor and the growing capital by the capital to income ratio, and these appear as stationary time series, predominantly periodic The change removes arbitrary assumptions, such as equality of growth rates for the exogenous trends, in autonomous expenditures and the investment floor. This seems to be good as at second thought the floor level apparently must be decreasing rather than growing when capital accumulates. The change also produces both trend and cycles on its own, which the original multiplier-accelerator model cannot, and further reduces periodic growth rates from 50–100% in the original model to more realistic 0.2–10%.

Access this chapter

Tax calculation will be finalised at checkout

Purchases are for personal use only

Notes

- 1.

National income, for instance, according to Erik Lindahl “Studies in the Theory of Money and Capital” 1939, was considered as current interest on total wealth, itself the sum of the discounted values of all future incomes of every asset in society. A totally useless theoretical construct.

- 2.

Economic flow originally entered economics through Fracois Quenay’s “Tableau Économique” in 1759 to illustrate goods and money circulating among social classes.

- 3.

Palander (1953) in his sole English publication, launches severe critique against the absence of explanations for transactions and pricing in disequilibrium, which might explain how entities such as involuntary investment are determined.

- 4.

Actually Keynes’s reasoning about this is the most ingenious part of the work, but we have no need to enter the details, because the conclusion is that monetary factors are inessential.

- 5.

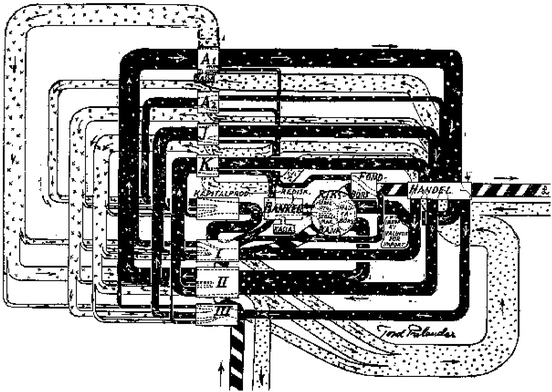

The present author’s supervisor, professor Tord Palander, who draw the picture Fig. 9.1, wanted a MONIAC also in Sweden, but he was outvoted in the research council by political scientists who claimed that if economists got an “economy machine” then they must also have a “state machine”. As there was no such thing, the project collapsed.

Fig. 9.1

Textbook illustration by Tord F. Palander from 1947 of the circulation of commodities and money in a Keynesian flow, adapted to actual Swedish national income data of that year

- 6.

Hicks and Samuelson were competitors in a sense. In “Foundations of Economic Analysis” 1947 Samuelson improved the stability analysis in Hicks’s “Value and Capital” 1939. In reverse, Hicks, as mentioned, in 1950 improved Samuelson’s linear business cycle model to a non-linear format. The present author had the pleasure of meeting both, though Hicks wanted to discuss his interest in Portuguese Jesuit architecture in Western India, whereas Samuelson enquired about the author’s supervisor Tord F. Palander, though not his scientific work but about his younger brother who was a well known medium who blindfolded could read unopened letters from unknown senders.

- 7.

We write “so called” because it was not in Alfred Nobel’s will. It appeared when the Bank of Sweden, one of the oldest central banks, had a 300 years anniversary. The bank had been a commercial bank as well and accumulated some handsome funds. Some people close to the government were also close to the academic discipline of economics, and they suggested a new prize. The Nobel Foundation fearing degradation refused. However, some time later they discovered they could earn much more on the stock market than on a bank account. However, the will stated that the funds be invested in the safe mode of a bank account. The government only could reinterpret Nobel’s will, so the Foundation turned to the government. They answered, “yes, but on condition that you accept the prize”, which was agreed. Later handsome sums of money have been offered to the Nobel Foundation for different new prizes, but they always refused.

- 8.

At least Aftalion in “La réalité des surproductions gé nerales” 1909, and J.M. Clark in “Business acceleration and the law of demand” 1917 seem to have had a clear idea of it.

- 9.

This poem, first read at a British national conference about the Hicksian model illustrates how important the model was considered, in a sense the very quintessence of mathematical economics. Notable is also how clear the audience was about the nature of nonlinearity created by floor and ceiling. To make the poem justice it should be read loud with appropriate mispronunciations, such as “exogenaus”.

- 10.

But at that time it was even difficult to publish, it was rejected by at least Journal of Economic Theory and Review of Economic Studies, as being trivial until the Oxford journal showed mercy.

- 11.

The model was proposed repeatedly in the period 2004–2007, but nobody seemed to be interested. Maybe the present author is to blame as the first paper, written with two mathematicians, went under the name: “Tongues of periodicity in a family of two-dimensional maps of real Möbius type”.

- 12.

It is not obvious which agents cut their expenditures when the ceiling is reached. As an alternative one might incorporate it in the investment function, along with the floor, thereby implying that it is the investors who cut further investment when they realize that full employment is reached. This was the choice of Goodwin (1951) and many other students of the Hicksian business cycle machine, including the present author (see Puu 1987; Sushko et al. 2004).

- 13.

A later mathematical analysis of Gandolfo’s case may be found in Gallegati et al. (2003).

- 14.

For the mathematician this effect might be interesting to study as the twists in the periodicity tongues seem to occur where the order of applications of region regimes is changed.

- 15.

We may yet want to include autonomous expenditures, because such are not unrealistic, just in order to avoid the absurdity of negative income, but they no longer play any crucial role in providing a growth trend.

- 16.

In discrete time dynamics this is no big problem. The discontinuity in the pair of hyperbolas \(y_{t}=\left ( a+c\right ) -\frac {a}{y_{t-1}}\) may cause the orbit to very large jumps. However, the relative dynamics would not work in a differential equation system because then the relative variable would indeed become infinite.

References

Allen RGD (1956) Mathematical economics. Macmillan, London

Duesenberry J (1950) Hicks on the trade cycle. Q J Econ 64:464–476

Gallegati M, Gardini L, Puu T, Sushko I (2003) Hicks’s trade cycle revisited: cycles and bifurcations. Math Comput Simul 63:505–527

Gandolfo G (1985) Economic dynamics: methods and models. North-Holland, Amsterdam

Goodwin RM (1951) The nonlinear accelerator and the persistence of business cycles. Econometrica 19:1–17

Hicks JR (1950) A contribution to the theory of the trade cycle. Oxford University Press, Oxford

Hommes CH (1991) Chaotic dynamics in economic models. Wolters-Noodhoff, Groningen

Palander T (1953) On the concepts and methods of the “Stockholm School”. International economic papers no. 3, Macmillan

Puu T (1963) A graphical solution to second order homogeneous difference equations. Oxf Econ Pap 15:53–58

Puu T (1987) Complex dynamics in continuous models of the business cycle. In: Lecture notes in economics and mathematical systems, vol 293. Springer, Berlin, pp 227–259. ISBN 3-540-18183-0

Puu T (2007) The Hicksian trade cycle with floor and ceiling dependent on capital stock. J Econ Dyn Control 31:575–592

Puu T, Gardini L, Sushko I (2005) A multiplier-accelerator model with floor determined by capital stock. J Econ Behav Organ 56:331–348

Rau N (1974) Trade cycle: theory and evidence. Macmillan, London

Samuelson PA (1939) Interactions between the multiplier analysis and the principle of acceleration. Rev Econ Stat 21:75–78

Sushko I, Gardini L, Puu T (2004) Tongues of periodicity in a family of two-dimensional maps of real Möbius type. Chaos Solitons Fractals 21:403–412

Sushko I, Gardini L, Puu T (2010) Regular and chaotic growth cycles in a Neo-Hicksian floor/ceiling model. J Econ Behav Organ 75:77–99

von Haberler G (1937) Prosperity and depression. Harvard University Press, Cambridge

Author information

Authors and Affiliations

Rights and permissions

Copyright information

© 2018 Springer International Publishing AG, part of Springer Nature

About this chapter

Cite this chapter

Puu, T. (2018). Macroeconomics and the Trade Cycle. In: Disequilibrium Economics. Springer, Cham. https://doi.org/10.1007/978-3-319-74415-5_9

Download citation

DOI: https://doi.org/10.1007/978-3-319-74415-5_9

Published:

Publisher Name: Springer, Cham

Print ISBN: 978-3-319-74414-8

Online ISBN: 978-3-319-74415-5

eBook Packages: Economics and FinanceEconomics and Finance (R0)