Abstract

The previous section set out international experience in the development and evolution of natural gas markets. A key insight from the five country case studies is that liberalisation requires different regulatory approaches for different parts of the natural gas value chain.

* This chapter was overseen by Jigang Wei from the Development Research Center of the State Council and Taoliang Lee from Shell Eastern Trading Corporation. It was jointly completed by Yaodong Shi, Zifeng Song, Ren Miao from the Energy Research Institute of the National Development and Reform Commission and Cindy Wang from Shell China. Other members of the topic group participated in discussions and revisions.

You have full access to this open access chapter, Download chapter PDF

Similar content being viewed by others

The previous section set out international experience in the development and evolution of natural gas markets. A key insight from the five country case studies is that liberalisation requires different regulatory approaches for different parts of the natural gas value chain.

This section draws from international experience and takes a closer look at regulatory efforts at specific points of the value chain. In the upstream segment, countries have encouraged exploration and production by increasing competition, including through fiscal and licensing regimes, to encourage new entrants into the industry. In the midstream segment, where natural monopolies exist, third-party access to transmission and distribution infrastructure has been crucial. In addition, some degree of unbundling of companies integrated across the value chain has been essential, both to reduce anti-competitive behaviour with respect to midstream infrastructure and to encourage competition across the natural gas value chain. In the downstream segment, countries have encouraged greater competition in the wholesale and retail markets supplying end users. Countries with significant domestic natural gas resources have liberalised their wholesale markets by encouraging greater competition and the establishment of natural gas hubs.

1 The Upstream Segment: Fiscal Policies and Licensing Systems

In addition to furthering a government’s fiscal objectives, these regimes have important implications for the development of a country’s oil and natural gas resources, the natural gas regulatory environment, the relationship between various levels of government and various agencies, and the overall nature of the oil and natural gas industry.

Upstream fiscal and licensing regimes play a critical role in the development of a country’s oil and natural gas resources. The two of them work in unison to offer benefits by incentivising investments and strengthening market competitiveness. Through an analysis of the experiences of the United States, Australia, Argentina and Mexico, this section carries out an in-depth exploration of natural gas upstream sector financing and taxes, permit system arrangements, and co-ordination and contact between various levels of government, all of which can be useful as references as China formulates similar policies.

1.1 International Taxation and Licensing Systems Regulating Upstream Production

Our analysis of international experience in fiscal and licensing regimes to regulate the upstream produced four overarching observations.

-

Unconventional resources: International experience in crafting fiscal and licensing regimes shows that policy makers need to consider the fundamental differences between the exploration and development of conventional natural gas reserves and that of unconventional reserves. Unconventional natural gas developments have an ongoing need to explore, develop and produce on order to find the most productive areas, the so-called “sweet spots”. These are characterised by shorter plateaus and more rapid depletion of reserves than conventional natural gas wells. As a result, unconventional operations require ongoing capital expenditures, whereas the majority of capital costs for conventional operations occur at the start of a development. Moreover, unlike conventional operations, unconventional natural gas developments typically require significant quantities of water, potentially affecting water availability for other users in the area, as well as water quality from the run-off and discharge of water used in processes such as hydraulic fracturing. This requires appropriate policy frameworks and processes to manage and minimise these impacts.

-

Co-ordination across government tiers: Fiscal and licensing regimes should also take account of the interplay between national and regional authorities. Each level of government has an important role to play in the development of a country’s energy resources, in terms of taxation and wider policy development. A review of experiences in the United States, Australia and Argentina shows that national and regional governments typically share the revenues generated, both directly and indirectly. Co-ordination between national and regional authorities is also required in terms of regulatory policies. For example, in the United States and Australia, access to midstream infrastructure—essential for encouraging competition in the upstream and downstream segments—requires policy co-ordination and alignment between the national and state governments.

-

Looking across the value chain: Fiscal and licensing regimes have a direct impact on promoting upstream developments, but they are just one part of an overall energy approach. Efforts to stimulate other parts of the value chain, especially demand, can have a profound influence on upstream activities. In Australia, for example, regulatory support for a switch to natural gas in power generation created momentum for greater domestic exploration and production.

-

Balancing the need for foreign investment and expertise with domestic interests: Investment in upstream exploration and production is often supported by foreign direct investment (FDI). However, at times, increased FDI can also create tensions with national oil companies or concerns that national interests are being neglected. The experience of Mexico and its Bid Round Zero illustrates how countries can balance these interests, providing opportunities and safeguards for domestic companies while bringing in foreign funding and capabilities.

1.2 Case Study 1: The United States—Leasing, Taxation and Development of Information Sharing

Under the United States federal system, most regulations for the oil and natural gas industry are enacted and enforced by the individual states. The US upstream investment regime uniquely is underpinned by ownership of mineral resources by the owner of the land. This means that onshore ownership of the resources is by private individuals, and private leases can be negotiated without a licensing authority. The exception to this norm concerns federal and state land, where the relevant government authority issues leases through tenders. For federal land, the Bureau of Land Management is responsible for issuing leases (Fig. 19.1). For federal waters—typically beyond three miles of the coastline—the Bureau of Ocean Management is responsible for issuing leases. Federal leases typically have a term of 5–10 years and can be renewed as long as production attributable to the lease continues.

US federal public land surface and underground levels. Source US Bureau of Land Management

With regard to the mining of natural gas, federal and state governments in the United States primarily use a tax and royalty regime. Onshore rates range from 12.5 to 30%, while the offshore rate is 18.75%. Most states also charge a severance tax, with its structure and level varying by state. For example, the Texas severance tax is 7.5% of the market value of the natural gas, while in neighbouring Louisiana, the severance tax is set each year based on NYMEX Henry Hub settled prices and on spot prices in the state. In 2014, this was 16.3 cents per thousand cubic feet.

The regime in the United States is also characterised by significant information sharing around the development of tight and shale natural gas, often cited as a reason behind the country’s successful development of unconventional oil and natural gas resources. Data on permits, drilling, testing and production is required to be made available in a timely manner, although the details vary from state to state. Interested parties can obtain the information directly from the state or from consulting companies that collect such data. In addition to legal disclosure requirements, companies also have incentives to disclose information—occasionally including details on individual wells—to support their share price and their efforts to raise capital. Publicly traded companies are also required to submit detailed quarterly and annual reports to the federal government, which are publicly available. In addition, several federal government agencies, including the US Geological Survey, the Department of Energy and the Energy Information Administration, monitor and publish key statistics weekly, quarterly and annually. Adding to the data flow, industry associations, technical and business journals, investment reports and conferences provide a platform for upstream companies, investment banks, academics and government to exchange information.

1.3 Case Study 2: Australia—Licensing, Finance and Taxation, and Third-Party Access

According to forecasts, in the near future Australia will become the largest LNG exporter in the world. It has liquefaction capacity of about 26 million metric tonnes a year in operation, and is expected to add about 62 million metric tonnes in additional capacity over the next several years. The new projects include three projects in Queensland, primarily using coalbed methane to produce LNG. A diverse range of companies are involved in onshore Queensland natural gas production, including PetroChina, Sinopec and the China National Offshore Oil Corp. (CNOOC).

Australia’s domestic natural gas system comprises the East Coast market, covering Queensland, New South Wales, South Australia, the Australian Capital Territory and Victoria, and the Western Australian market, covering the rest of the country. Australia does not have an extensive pipeline network, especially compared to Europe or the United States, because demand is highly concentrated in the various state and territory capitals and because supply has historically come primarily from two basins, Cooper and Gippsland (Fig. 19.2).

Australia’s natural gas basins and major transmission pipelines. Source Australia Energy Regulator

Alongside fiscal and licensing measures to stimulate upstream exploration and production, Australia also provided demand incentives to increase the share of natural gas in the energy mix. The Queensland Gas Scheme illustrates the success of such measures in driving coalbed methane production. Introduced by the Queensland government in 2005, the scheme required all electricity retailers to acquire 15% of the power they sold from natural gas-fired generation plants. Accredited power producers generated Gas Electricity Certificates (GEC) for each MWh of eligible natural gas-fired electricity they produced. These GECs are then sold to the electricity retailers, providing an alternative revenue source for power producers to offset the higher cost of natural gas-fired power generation compared to coal. The scheme ended in 2013 when the state government declared that its goals of promoting the state’s natural gas industry and reducing greenhouse natural gas emissions had been achieved. During this time, natural gas-fired power generation had gone from 5% of total power in 2005 to 20% in 2013, and the state’s unconventional natural gas production had grown from 1 billion m3 in 2004–05 to 6 billion m3 in 2010–11 (Fig. 19.3).

Natural gas production in Queensland, Australia. Source Queensland Department of Natural Resources and Mines

Australia has three levels of government—federal, state or territory, and local—and has a concessionary fiscal regime. The federal government and state and territory governments share jurisdiction over petroleum resources, and there are no private ownership petroleum resources.

State and territory governments manage the licences for development onshore and within 3 miles of the coastline. They collect royalties of between 10 and 12.5%, based on the wellhead value of the petroleum resource. Licences in Queensland are issued and managed by the Department of Natural Resources and Mines, and the published royalty rate is 10%.

The federal government manages licences for offshore development beyond 3 miles of the coastline. It levies a Petroleum Resource Rent Tax of 40% for both onshore and offshore oil and natural gas, with state and territory royalties deductible from the amount due.Footnote 1 In addition, the federal government levies a corporate tax of 30%. It also levies a value added tax, known as a Goods and Services Tax, of 10% on most transactions, with receipts redistributed to the state and territory governments.

The three levels of government in Australia co-ordinate to develop natural gas resources and markets. The Council of Australian Governments is the main intergovernmental forum that promotes policy reforms with national relevance or those that require co-ordinated action at all levels. Members of the council are the prime minister, the premiers or chief ministers of each state or territory respectively, and the president of the Australian Local Government Association. In addition, the Standing Council on Energy Resources (SCER) was founded in 2011 and comprises federal, state and territory ministers responsible for energy and resource matters. The council’s responsibilities include oversight of the natural gas and electricity markets, energy laws and regulations, energy security and emergency management, and promoting the economic development of Australian resources.Footnote 2

Companies developing new upstream infrastructure may be granted exemptions from third-party access requirements if they satisfy criteria outlined in the legislation.

Access to third-party infrastructure is established under the federal Competition and Consumer Act. The National Competition Council (NCC) is established through consensus by the SCER and is responsible for recommending regulations on third-party access to monopoly infrastructure, including natural gas transmission pipelines. Factors taken into consideration include whether access would increase competition in a market, the economics of developing competing infrastructure, and whether the infrastructure is already subject to an effective access regime.

For example, 15-year exemptions have been granted to cover the pipelines being built to transport natural gas from the three Queensland LNG projects to the liquefaction plants in Gladstone. The NCC concluded that third-party access “would not promote a material increase in competition in any likely dependant market”.Footnote 3 Even though the developers can obtain a waiver, nonetheless the Australian Competition and Consumer Commission (which also has jurisdiction beyond energy) and the Australian Energy Regulator (AER) both carry out significant oversight, strictly executing energy market rules and providing protection for competition and consumers.

1.4 Case Study 3: Argentina—The Special Licensing System and Encouraging Investment

Argentina is a significant producer and consumer of natural gas. According to data from the US Energy Information Administration, the country’s technically recoverable shale natural gas reserves are second only to those in China, and its shale oil resources are the world’s fourth largest, after Russia, the United States and China. According to forecasts, Argentina’s natural gas demand will have been 44 billion m3 in 2015, accounting for 45.7% of its energy structure. Currently, the domestic shortfall is met by LNG purchased primarily from the spot market and imported through two floating regasification and storage units. Natural gas prices are regulated and subsidised below cost, but prices have begun to be deregulated—mainly through bilateral negotiations—to encourage upstream investment and to raise revenues for the government.

Argentina’s concession-based licensing system replaced a system based on risk service contracts. State-controlled Energía Argentina S.A. (ENARSA), which is 35% publicly owned, owns all unlicensed federal offshore exploration acreage more than 12 nautical miles from shore. Any activity in these blocks must be done in partnership with ENARSA. Provincial governments issue tenders for onshore projects.

All licences are subject to royalties, income tax, provincial sales tax and other signature bonuses and rentals, as well as possible export duties on oil and natural gas. The Oil and Gas Law, passed in 2014, centralises implementation of the royalty system and licensing, but leaves the administration to provincial regulators. Before this law was enacted, provincial governments had jurisdiction on oil and natural gas licensing and operations, and many provincial governments took equity interests in licences. From this it is clear that provincial-level governments can become involved in relevant licensing matters through their various oil and natural gas departments (Figs. 19.4 and 19.5).

Argentina’s primary basins and LNG receiving stations

Argentina’s natural gas production and consumption. Source Energy Information Administration, International Energy Statistics

Due to growing energy needs, governments have begun to focus on stimulating investment. In October 2014, the Oil and Gas Law was passed. This contained a series of measures providing incentives for investment in unconventional oil and natural gas exploration and production, including:

-

distinguishing between conventional and unconventional resources, for example by providing unconventional assets with an exploitation period of 35 years compared to 25 years for conventional resources (exploration periods are 13 years);

-

plans to allow higher prices for natural gas produced using unconventional means;

-

creating an unconventional production licence, providing five years for a pilot project to become commercially viable, with royalties to be dropped by 25% for unconventional projects after the pilot phase is completed; and

-

allowing 20% of production to be exported.

However, obstacles remain to building an unconventional natural gas industry in Argentina, including a shortage of trained labour. The opening of the Unconventional Fields Technology Center in Neuquén Province is a step forward, but more is needed to build capabilities in shale natural gas technology. In addition, current regulations do not address environmental concerns adequately, which could become problematic for unconventional developments near population centres.

1.5 Case Study 4: Mexico—Reopening the Market and Round Zero Tender

Mexico’s oil industry is one of the world’s oldest; oil was first discovered in Mexico in 1904. By 1921, Mexico’s oil production had reached 530,000 bod, accounting for 25% of the world’s oil production. Following labour disputes, international oil company assets in Mexico were nationalised in 1938, which led to the creation of the national oil company Petróleos Mexicanos (Pemex). Pemex held exclusive rights to the country’s oil and natural gas fields.

In the following decades, Pemex largely ran its own oil and natural gas operations, aided by international service companies. As a state monopoly, its budget and financial management were heavily controlled by the Ministry of Finance and Public Credit, leading in part to its gradual stagnation. Its production volume continually dropped, beginning in 2004 (Fig. 19.6). Its production volume peak was between 2004 and 2005, with approximately 2.6 million barrels/day, as well as 3 billion ft3 of natural gas. Rapid further decline is projected for the coming years.

Oil and natural gas production in Mexico. Source Wood Mackenzie

In an attempt to halt production declines, in 2013 the political party known as PRI began implementing energy reforms after 71 years. President Enrique Peña Nieto proposed an Energy Reform Act in August 2013. The act was eventually passed in December 2013, allowing international oil companies and other investors to invest once again in Mexican oil and natural gas businesses through three possible legal arrangements: service contracts, production- or profit-sharing contracts, or licences.

To protect the national interest in Pemex, the government ran a unique tender in 2014, Bid Round Zero. Under the tender, Pemex had to submit applications for which fields and blocks it wanted to keep and relinquish the rest. The submission had to demonstrate technical, financial and operational capabilities to operate productive assets, and, for exploration acreage, Pemex had to show it had either drilled exploration wells, conducted sub-surface studies or both. The Energy Secretary and the Comisión Nacional de Hidrocarburos (National Hydrocarbons Commission) made the final decisions on the applications.

As a result of Bid Round Zero, Pemex retained about 83% of proven and probable oil and natural gas reserves (Fig. 19.7) and 21% of the prospective resources, based on commission estimates (Fig. 19.8). Pemex was also allowed to invite foreign investors to join in the exploration, development and production of assets it retained.

Pemex reserves analysis after bid round zero

Pemex unconfirmed resources, 2014. Information source HIS, PFC Energy

A measure like Bid Round Zero could be an attractive option for China. Such a tender would allow existing state oil companies to nominate assets they would like to retain, freeing up other assets for new entrants. The move could attract greater energy investment and accelerate the development of unconventional shale natural gas production. Increased domestic production would reduce the country’s dependence on foreign natural gas, which rose from zero in 2005 to 32% of domestic consumption in 2013.

In late 2014, the National Hydrocarbons Commission began Bid Round One, which will be a staged tender and include shallow water exploration, shallow water development, onshore projects, enhanced production for the Chicontepec field, unconventional oil and natural gas, and deepwater projects (Fig. 19.9).

Suggested timeline for a new round of tenders

Without question, the most important factor in these events has been the speed and determination of the Mexican government in taking clear and transparent steps toward energy reform, including the 20%+ of discovered oil/natural gas fields provided to international oil companies following the final Round Zero Tender. It is worth considering which of these measures could suit China’s situation, especially in the accelerated exploration and development of unconventional natural gas and shale natural gas, as well as in attracting suitable international oil companies and private investors to accelerate the trials in this process. It is also worth considering whether Mexico will continue on its path of open policies after the six-year term of President Enrique Peña Nieto.

2 The Midstream Segment: Building Infrastructure and Managing Access

Midstream assets—transmission pipelines, LNG regasification terminals and storage facilities, and distribution networks—are natural monopolies. They have high fixed capital costs of investment but low, and decreasing, marginal costs of operation. As a result, it is economically more efficient if fewer of these assets are built and fully utilised, rather than assets being duplicated and dividing volumes among them through competition.

Natural gas pipelines—both transmission and distribution—have more significant natural monopoly characteristics than LNG terminals or storage facilities. The economies of scale for LNG terminals and storage facilities are not as great as those for pipelines. Hence, for a given market size, the optimal number of facilities required will be greater compared to the number of pipelines required to serve a market of similar size. Moreover, LNG terminals and storage facilities can compete with other similar assets once they are connected through a pipeline network.

In the United States, LNG receiving stations are viewed as upstream assets, because they are seen as extensions of upstream wells. However, in Europe, LNG receiving stations are midstream assets. The difference in perception depends on the degree of competition in the market. In the United States, LNG receiving stations compete with domestic products, and thus they seen as comparable to domestic wells. In Europe, the majority of competition comes from imported natural gas, and thus LNG receiving stations are viewed as part of the transmission network. If LNG receiving stations are seen as upstream assets, then regulatory measures will be different, and there will be fewer concerns about the monopolistic nature of the receiving stations. In China, there is uncertainty regarding the character of LNG receiving stations, because development is lacking in competitive natural gas markets.

The natural monopoly characteristics of midstream infrastructure mean that government oversight and regulation is required to prevent access being restricted and monopoly rents being charged. A monopoly owner of midstream infrastructure has an incentive to charge very high prices to maximise its profits, reducing pipeline utilisation in the process. It may therefore be necessary to unbundle midstream assets from vertically unified companies. Examples of the options for accomplishing this can be found by looking at the international experiences seen in the case studies.

Even if midstream assets do not belong to a given vertically unified company, if no oversight is implemented, there is still the possibility of problems arising. On the one hand, independent owners need upstream and midstream participants to use their midstream assets. On the other hand, independent owners also have an incentive to collect the highest price possible to maximise their profits. Regulation is the solution, to ensure that usage rights to midstream assets are available to all parties (in other words, third-party access).

Regulatory institutions will often need to unbundle and re-establish third-party access. In practice, even if there are rules for third-party access, there are still many means to exclude third parties, such as lack of transparency over pricing. Using regulatory institutions to implement strict regulation of third-party access can prevent such anti-competitive behaviour. At the same time, many regulatory institutions believe that through unbundling such motivations can be eliminated, which is an effective supplement to third-party access rules.

In a growing market in need of investment, such as China, regulatory frameworks should ensure that investments can receive sufficient profits, encouraging capital investment. Regulation of the collection of usage right fees can help asset owners to recover their capital. Regulation of fee collection can employ either a “regulated return” system or a “regulated tariff” system. These two methods are very similar, but have differing risk allocations in terms of midstream asset users and owners. Under a “regulated return” oversight approach, the owner of the midstream is authorised to receive a high enough rate of return to act as a motivation for future pipeline construction. Under the “regulated tariff” regime, such tariffs should likewise be sufficiently high to provide an incentive for future asset investments.

The challenge therefore faced by government departments is to achieve a balance between making usage rights available and encouraging investment in midstream assets. This balance can be achieved through a precisely designed regulatory framework, which will need to include the following key factors: rules for liability and standards, a consensual pricing framework for third-party access and a mechanism to assure returns for investors. In some frameworks, when regulatory institutions solve downstream market structure or legacy issues, these mechanisms can be used to balance out two different goals.

When a country’s regulatory mechanisms reflect various domestic factors, such evolutions and influences can be referenced by China. We examine three case studies below: the third-party access arrangements of the United Kingdom in the North Sea; Singapore and Japan’s LNG experience; and Shell’s IPO of its Shell Midstream Partners enterprise in the United States. These case studies yield five primary lessons:

-

if it is to promote usage rights and investment, regulation must strike a balance between the economic interests of midstream asset users and owners;

-

regulatory frameworks must be stable, reliable and clear, thereby facilitating general risk minimisation and stimulation of investment;

-

mechanisms based on rules can provide a means of resolution for this;

-

at the same time as generating revenue, regulations such as mandatory third-party access requirements can ensure that midstream assets are used efficiently;

-

even while balancing usage rights and investment, regulatory institutions can also consider market structure in addition to the value chain. Current regulatory policy will influence future economic opportunities.

2.1 Balancing Third-Party Access and Investment Incentives

Third-party access needs to be balanced against incentives for further investment in midstream infrastructure, especially in growing markets such as China. While allowing for third-party access, the regulatory framework also needs to provide adequate incentives—and returns—on future investment in the midstream. For example, access charges can be regulated to enable asset owners to recover fixed costs.

Regulated charging regimes can be of two types: either regulating the rate of return achieved by midstream infrastructure owners or regulating the tariff charged for access to midstream infrastructure. Under a regulated return regime, the owner is granted a rate of return on its midstream asset value that is high enough to provide incentives for future investment in maintaining and extending the infrastructure network. Under a regulated tariff regime, the tariff is set at a level that provides incentives for future asset investment. Both approaches are similar, but vary in the distribution of risk among the users and the owners of midstream assets.

While an individual country’s regulatory regime reflects a variety of domestic factors, a review of the evolution and impact of these regimes can offer insights for China in achieving a balance between returns to investment and access to midstream assets. The oversight of natural gas infrastructure reflects a country’s experience in the realm of natural gas market liberalisation, as well as its systemisation and government and policy priorities. There is no single oversight system that can be transplanted from one jurisdiction to another. In fact, if residual issues, systems and political factors are not taken into consideration, replicating another country’s oversight structure will result in failure (United Nations Economic Commission for Europe 2012). However, it is possible to learn by comparing existing oversight frameworks that the key is to balance the attainment of public and private goals.

Regulatory institutions often need to unbundle third-party access. In reality, even if there are third-party access rules, there are still many means by which to exclude third parties—for example, a lack of transparency over pricing of capacity. Regulatory institutions can prevent such anti-competitive behaviour by rigorous oversight of third-party access rules, but many regulatory institutions believe that unbundling is an effective solution that eliminates the incentive for anti-competitive behaviour.

In growing markets in need of investment, such as China, regulatory frameworks should also allow for sufficient profits, thereby providing momentum for future midstream investment. Using a “regulated return” system, owners of midstream assets are allowed sufficiently high rates of return that there is an incentive for future piping construction. Under a regime of “regulated tariffs”, such tariffs should likewise be sufficiently high to provide an incentive for future asset investments.

The challenge for government departments is therefore to achieve a balance between midstream asset usage rights and investment, as shown in Fig. 19.10. Within a carefully designed regulatory framework, it is possible to achieve this goal. Many countries have achieved such success, and the regulatory mechanisms that may be of interest to China as precedents include:

The balance of factors needed in the regulatory framework

-

Rules: Regulators establish and enforce rules on liability and standards.

-

Prices: Regulators provide a framework for investors and users to agree on prices in both third-party-access and regulated-return regimes.

-

Mechanisms to reduce risk: Regulators minimise risk for investors and users.

2.2 International Experience of Managing Midstream Asset Access

The case studies provide five overarching insights:

-

Regulation balances the economic interests of users and owners of midstream assets to facilitate access and investment. Economic opportunities drive demand for access to and investment in infrastructure. However, demand by itself is an insufficient condition for access and investment, as users and owners often cannot agree terms, often because of the asset owner’s natural monopoly power. Thus, players require a strong regulatory framework that grants access to the midstream and provides incentives for investment. For example, experience in Singapore and the United Kingdom in establishing third-party access shows that strong regulation can assist users of assets in their negotiations with midstream operators.

The experience of the United States and Japan has shown that in terms of risk/reward for investors, oversight is beneficial in creating investment opportunities and encouraging more funds to be channelled to the construction of midstream infrastructure.

-

Regulation can ensure that the midstream asset is used efficiently. Regulation, such as mandatory third-party access requirements, can ensure that players upstream and downstream can access the pipeline and that the fees charged and returns made by the owner of the midstream asset are fair. Regulation can take various forms, such as negotiated or regulated access, but all forms of regulation are aimed at increasing access while ensuring reasonable returns to the asset owner and supporting sufficient investment to maintain energy security.

Controls implemented according to specific circumstances can utilise agreement negotiations or controls to achieve third-party access. The British North Sea owner and user negotiations successfully implemented third-party access, with new companies able to develop small-scale gas fields without needing to invest in the construction of new piping. Midstream asset owners can obtain revenue from amortised assets, and the government can obtain relevant oil and natural gas production taxes related to asset development.

However, in the rapidly growing market of China, the experience from the North Sea is of limited use. There is very little need for new investment in piping in the North Sea, and this made it easier for midstream facility owners and users come to an agreement. This is not the case in China, and the facility owners tend to look to use their position to collect monopolistic lease amounts. As a result, China’s rapidly growing emerging market should give greater consideration to using mandatory third-party access systems to stimulate investment in midstream facilities by promoting recovery of capital and reasonable risk returns.

-

The regulatory framework should be stable, credible and clear to minimise risk and encourage investment. The success of the master limited partnership in the United States has been in large part the result of government providing a statutory basis for partnership treatment: federal rules on qualifying income and assets gave all parties the necessary certainty to proceed. In the United Kingdom, the combination of a statutory, rules-based framework and the threat of arbitration ensures that when negotiating third-party access, parties have similar expectations and incentives, with it being very rare that events end in disagreement. The regulatory layers collectively help to reduce uncertainty for participants (see Fig. 19.11). In contrast, the absence of enforcement has meant that third-party access rules are not credible, and midstream infrastructure is for the most part not open to third parties.

Fig. 19.11

The three layers of agreements supporting North Sea usage rights

-

Regulators should take into account market structures along the value chain when balancing access and investment. The nature of competition along the entire value chain influences regulatory choices. For example, Japan has a fragmented market where all natural gas is imported by LNG shipments and there is limited interconnection between regional markets. This means that competition is hard to achieve and brings few benefits, and as a result third-party access is limited.

In the United Kingdom, the natural gas market was originally created upstream, with competitive downstream markets only starting in the 1980s, and thus its regulatory framework design focus is on the promotion of midstream usage rights.

In Singapore, private funding for an open-access LNG terminal fell through as a result of sufficient pipeline gas supply to meet demand and liberalised downstream markets, which favoured cheaper pipeline gas over more expensive LNG imports. The government stepped into develop the LNG terminal as a means of diversifying sources of supply and enhancing energy security. Ownership is deliberately separated from operation of the multi-user LNG terminal, and the government has developed a framework to open the terminal to third-party access. At the same time, the government has also sought to secure downstream demand for LNG by restricting new pipeline imports (Table 19.1).

Table 19.1 The influence of the nature of competition on midstream infrastructure regulation choices -

The regulatory framework a country pursues affects the set of available policy choices. The regulatory legacy can affect the level of utilisation of infrastructure, the level of activity by new entrants and the form of private contracts. The private sector’s capacity to identify and develop economic opportunities is a function of how a country’s regulatory regime and its infrastructure have evolved.

In the first years of development of North Sea gas, large companies obtained permits from the government and independently invested to develop the oil and gas fields. In the past 12 years, because of drops in yields, these oil and gas fields have seen reduced rates of return, and there is less interest from large companies. However, the amortised assets that they possess can be transferred to smaller enterprises to develop small-scale oil fields that pay the larger companies for usage of their assets. Therefore, from the 1960s to the 1990s, the United Kingdom’s regulation system has increased the opportunities today.

In Japan, even though on the surface LNG receiving stations seem to be accessible, regulators have chosen to use negotiated approach a third-party access, rather than making it mandatory. This approach gives facility owners a powerful negotiating position. Combined with a lack of competition upstream and downstream, there is a push for suppliers and upstream facility owners to sign long-term supply agreements. Without reliable access systems, new entrants to the market generally build new LNG receiving stations in order to take advantage of downstream business opportunities.

2.3 Case Study 1: The UK North Sea—The Framework for Negotiated Third-Party Access

The United Kingdom’s North Sea experience illustrates one approach to arranging access to midstream infrastructure. In particular, it focuses on the government’s efforts to develop a regulatory framework that grants new entrants access to the pipelines built by earlier North Sea field developers.

Several key lessons emerge from this experience:

-

A liberalised market with clear rules encourages new investment. Output from the North Sea was declining and costs were rising. However, new firms that specialise in declining fields were able to enter the liberalised market, which has provided asset owners with new business and the government with greater tax revenue.

-

Users of assets have been favoured over owners to some extent. As midstream assets were already in place as a legacy of past exploration of the North Sea, and faced declining utilisation, new users seeking access had greater bargaining power as asset owners had few alternative customers. In addition, by encouraging access, the government could benefit from greater hydrocarbon production tax revenues associated with resource development.

-

Where interests between midstream asset owners and users are broadly aligned, a voluntary agreement on access provision between the parties is feasible. The United Kingdom had a layered regulatory framework to access. Parties were encouraged to reach voluntary agreements, with clear rules for dispute resolution and, ultimately, a legal framework if voluntary agreements could not be reached. This system has worked well, with many parties reaching voluntary agreements, because interests are broadly aligned and the rules are clear and credible.

China faces a different gas market context than seen in the North Sea example. China’s natural gas market is growing rapidly, whereas output from the North Sea was declining. As a result, the economic pressures felt by UK asset owners that supported negotiated third-party access—specifically, existing assets with declining utilisation—would not be as prevalent in China, where limited midstream capacity gives asset owners more bargaining power. Nevertheless, the North Sea experience demonstrates how a credible regulatory framework can help achieve agreement and avoid disputes.

-

1.

Background

The regulatory regime for natural gas exploration in the United Kingdom from the mid-1960s through to the 1980s was characterised by liberalisation and increasingly competitive markets. When the first licences were offered by government, major companies chose to develop oil and natural gas fields as stand-alone installations. Upstream pipelines and offshore processing facilities were usually built by field owners to process and transport output from specific oil and natural gas fields. However, since then, recovery rates—and returns—from these fields have fallen, and larger enterprises have been less interested in developing the remaining resources.

As spare capacity became available in pipelines and terminals, opportunities arose. The existence of their depreciated pipeline assets has allowed smaller players to enter the industry and exploit smaller fields, paying larger companies to use their assets to transport oil and natural gas to the mainland. A liberalised downstream market meant there was a ready market for small-field developers if they could access midstream assets. There were benefits to infrastructure owners, too, in terms of additional revenue from granting third-party access to new users and from deferring the costs of decommissioning these assets. The government saw opportunities in terms of additional job creation, maximising recovery of North Sea oil and gas resources, and continued production tax revenues.

The 1996 Network Code established the rules and procedures for third-party access to pipelines and introduced a regime for daily balancing, while the Petroleum Act of 1998 set out the rules around upstream exploration and production. By the early 2000s, liberalisation of the sector was complete, with the creation of the National Grid as a fully unbundled, independent transmission system owner and operator of the United Kingdom’s natural gas and electricity markets in 2002.

However, the legal framework by itself was insufficient and left room for commercial disputes between owners and users of the infrastructure. Through the 1990s, there were concerns that the tariffs to access infrastructure were too high compared to costs and risks of developing small fields. This led to a new process for negotiating access. The legislative and regulatory changes provided a statutory basis for a rules-based framework, including a process for arbitration of disputes, which helped co-ordinate activity and create common expectations.

-

2.

The framework for negotiated third-party access

Working with government, the natural gas industry sought to develop voluntary frameworks for third-party access. The first industry offshore Code of Practice was introduced in 1996. It sought to establish a timely process for seeking, offering and negotiating third-party access to natural gas infrastructure in the North Sea. It also sought to ensure that access was easy and fair, with terms offered on a negotiated, non-discriminatory basis.

In 2004, market participants agreed to a strengthened code, the Infrastructure Code of Practice. The code outlined best practice and expected behaviour in conducting negotiations for access to infrastructure. According to the industry group Oil & Gas UK, the code was intended “to facilitate the utilisation of infrastructure for the development of remaining UKCS [United Kingdom continental shelf] reserves through timely agreements for access on fair and reasonable terms, where risks taken are reflected by rewards”. Its main tenets are:

-

Parties uphold infrastructure safety and integrity and protect the environment.

-

Parties follow the Commercial Code of Practice.

-

Parties provide meaningful information to each other before and during negotiations.

-

Parties support negotiated access in a timely manner.

-

Parties undertake to settle disputes if needed through the Automatic Referral Notice process which involves the UK minister responsible for energy.

-

Parties resolve conflicts of interest.

-

Infrastructure owners provide transparent and non-discriminatory access.

-

Infrastructure owners provide tariffs and terms for unbundled services, where requested and practicable.

-

Parties seek to agree on fair and reasonable tariffs and terms, where risks taken are reflected by rewards.

-

Parties publish key commercial provisions from the agreements.

Companies seeking access to infrastructure falling within the scope of the third-party access provisions of the Energy Act 2011 must apply first to the owners. However, the act also allows the government minister responsible to take the initiative and set the terms in cases where there is no realistic prospect of reaching an agreement. If the parties are unable to agree to satisfactory terms and conditions, the prospective user may apply to the minister to resolve the dispute. The minister can require access to pipelines, associated offshore production facilities, and onshore natural gas processing facilities, and dictate the appropriate terms. In most cases, these terms will be in line with those offered by infrastructure owners in a competitive environment. In such cases, the legislation stipulates that appropriate notices be issues to the parties to implement the terms. While a dispute resolution procedure exists and the minister can intervene to adjudicate, the third-party access framework is essentially self-enforcing and has rarely resulted in dispute.

A crucial factor in the success of the framework is that it reduces commercial risk by giving stakeholders guidance on tariffs and a variety of other terms. Terms of agreements tend to be quite specific with regard to liability, transparency and technical standards. Terms covered often include:

-

the basis for modification of infrastructure, if necessary;

-

the duration of service;

-

identifying which party has ownership and risk exposure to the natural gas while it is within the infrastructure owner’s facility;

-

capacity terms and the ability of the owner to change them;

-

charges for providing the service;

-

rights of both parties to terminate the agreement; and

-

liabilities covering damage and loss relating to people, property and pollution.

Within the regulatory framework, both owner and user considerations are important in determining terms of access. Competition and other market forces, the user’s ability to pay and contract flexibility are all key considerations to be taken into account when agreeing the terms of access (Fig. 19.12).

Analysis of regulatory frameworks

Owners and users have flexibility when negotiating access. For example, when agreeing to provide access, the infrastructure owner reserves capacity in its system for the shipper. The shipper gains certainty that the required capacity will be available, subject to normal operational availability, and the infrastructure owner will not market reserved capacity to others. In turn, the infrastructure owner will want to mitigate the risk of the user booking more capacity than required, such as through send-or-pay provisions, which guarantee minimum payment regardless of the extent to which the reserved capacity is used. In declining fields, such as in the North Sea, terms of access are often based on operating costs, plus a risk premium. This contrasts with the approach for newer fields, where the terms of access also tend to include operating costs, as well as capital cost recovery.

2.4 Case Study 2: Japan and Singapore LNG—National Power and the Influence of Oligopoly

Singapore and Japan have had entirely opposite experiences in the development and control of midstream infrastructure, especially in terms of LNG regasification receiving stations (Table 19.2). However, the experiences of the two countries highlight that for a balance to be struck between access to and investment in midstream infrastructure, both a streamlined industry chain and consideration of the influence of the market structure are necessary.

-

1.

Singapore LNG: national power involved in influencing construction of infrastructure

Singapore has no domestic natural gas resources and is dependent on imports. Natural gas consumption grew rapidly in the 2000s, from 1.3 billion m3 in 2000 to 8.7 billion m3 in 2010.

Into the early 2000s, the island-state’s natural gas market was characterised by government ownership along the value chain through Singapore Power Group and SembCorp, limited or no unbundling in commodity and transportation activities, significant price controls on electricity, and generally homogeneous supply through pipelines deliveries from Malaysia and Indonesia. In 2004, the country began progressive liberalisation, resulting in a competitive midstream and downstream natural gas market, including regulated open-access networks, a significant number of primarily private market participants, unbundled commodity and transportation activities, and oversight entrusted to an independent energy regulator, the Energy Market Authority (Fig. 19.13). The government’s role is limited to ensuring fair access to infrastructure.

Market diversification in Singapore, 2004 versus 2014

In 2006, the government decided to develop an LNG regasification terminal to enhance energy security by diversifying sources of supply away from existing pipeline gas. However, meeting the policy objective on energy security was not consistent with Singapore’s liberalised and competitive wholesale and retail markets. Singapore had a well-functioning domestic natural gas market, with sufficient supply from pipelines, and there was little market demand for an LNG regasification terminal, despite the energy security benefits it offered.

The country originally granted a licence to a private consortium of PowerGas and GDF Suez to make the necessary investment, but this arrangement collapsed in 2009 because of a funding shortfall. While the problem was linked to the 2008 global financial crisis, it also reflected the competitive nature of the downstream market, which dampened the commitment among potential customers of the LNG facility. The benefits of diversifying supply were outweighed by the risks of being a first mover to a more expensive and untested source, reducing the incentive for energy companies and end users to switch supply sources.

In 2009, the government announced it would take over the development and ownership of the LNG terminal. It established the Singapore LNG Corp. to develop and operate the terminal. The facility, which opened in 2013, was regulated by the Energy Market Authority. It was open access, with third-party access arrangements underpinned by a rules-based regulatory framework, including a dispute-resolution process, and public ownership of the infrastructure was deliberately kept separate from commercial operation.

The regulatory framework established by the government and the Energy Market Authority was designed to guarantee fair and transparent access to midstream infrastructure while reducing investor risk. It comprised three key elements:

-

Aggregator: A private company, BG, was appointed natural gas aggregator to secure supplies. By pooling demand from large users, Singapore maximised its negotiating power on global markets and secured competitively priced supply.

-

Framework: Terminal access rules agreed between BG and Singapore LNG provided a commercial framework for other third parties that sought access and enabled a greater degree of forward planning by energy companies.

-

Support: The government offered a purchase agreement with any power-generation company that committed to LNG supply and a tariff structure that allowed companies to pass through the cost of LNG.

The terminal had the capacity to handle three times as much natural gas as the country consumed. While it initially opened with a 3 million tonnes per year capacity, the opening of its third tank in 2014 doubled capacity to 6 million tonnes. A fourth tank is expected to open by 2017, which would bring total capacity to 9 million tonnes. The terminal could eventually accommodate seven tanks, for a total capacity of 15 million tonnes.

Because capacity was planned to exceed domestic requirements, the government has also sought to secure downstream demand for LNG. To do this, the government introduced controls on new pipeline imports in 2006. These controls allow existing contracts to be honoured, but new contracts were subject to approval from the Energy Market Authority. The decision moved Singapore away from its free market approach and introduced a measure of uncertainty about the evolution of Singapore’s natural gas markets. While the moratorium on new pipeline imports is likely to be lifted, it remains unclear whether the government will continue to limit direct competition between pipeline natural gas and LNG.

Key lessons from Singapore’s experience of developing and regulating its midstream LNG infrastructure include:

-

Markets can face challenges when investing to achieve policy objectives. Singapore had a well-functioning domestic gas market, with sufficient supply from pipelines. Given this, there was little market demand for an LNG terminal, despite the energy security benefits it offered.

-

Regulation is needed to deliver policy objectives. As the market would not provide the investment, the government had to step in and invest in the LNG terminal itself. At the same time, the government also sought to secure downstream demand for LNG by restricting new pipeline imports. However, in recognition of the efficiency of market forces, the government operated the terminal as a multi-user access terminal to enable competition downstream between importers.

-

Regulators have an important role in setting up the commercial framework for access. The terms of access were clear and credible, allowing private companies to make long-term plans despite the uncertainty that comes from an open access terminal, such as available docking times and capacity.

-

2.

Japanese LNG: oligopoly restricting third-party access

Japan imports most of its natural gas, and its imports are exclusively LNG. The country has 30 operating LNG terminals, with a total capacity of 172 million tonnes a year, a level well above domestic demand. However, Japan remains constrained by how much LNG it can receive, based on berthing, ship size and other infrastructure limitations. Five additional terminals are currently under construction and expected to become operational by 2016, adding capacity of at least 7 million tonnes.

The majority of LNG terminals are near main population centres and manufacturing hubs around Tokyo, Osaka and Nagoya (Fig. 19.14). They are owned by local power companies, either alone or in partnership with natural gas companies, and the same companies own much of Japan’s LNG tanker fleet.

Japanese LNG facilities and their proximity to large cities and manufacturing hubs. Note This document and any map included here are without prejudice to the status of or sovereignty over any territory, to the delimitation of international frontiers and boundaries and to the name of any territory, city or area. Source IEA

Japan has unique energy fundamentals that make midstream assets particularly important. Japan has no domestic production of natural gas and few other domestic sources of energy.

The country also does not have a well-developed or integrated domestic long-distance natural gas transportation network, partly because its mountainous geography limits the development of a network. Instead, LNG regasification terminals have proliferated along the coastline and take the vital role of a transmission network. However, as a result of these conditions, downstream markets are fragmented and dominated by regional monopolies. Domestic natural gas transport and distribution infrastructure, including LNG terminals, is owned and operated by vertically integrated private natural gas and power companies. The natural gas market remains largely uncompetitive, with four companies supplying more than 70% of natural gas and almost all LNG terminals owned by a small number of companies and no actual third-party access.

Open access in LNG infrastructure was discussed in the US-Japan Third Joint Status Report under the Enhanced Initiative in 1999, an economic co-operation agreement between the two countries. In response, the Japanese government amended the Gas Utility Act in 2003 and introduced an open-access scheme that obliged natural gas companies to define preconditions for negotiated access. Further transparency requirements related to the capacity information for LNG storage and facilities were also introduced. The changes were intended to act as a guide for infrastructure users, but did not go far enough: third-party access to terminals was characterised as “desirable” and LNG terminals were not classified as “essential facilities”. As a result, while a mechanism for access exists, the regulatory framework does not promote ease of access. Users face a lengthy application process, the timing, flexibility and tariffs are unclear, and there is no arbitration or dispute resolution process.

Since the changes were introduced, no company has effectively negotiated third-party access. Incumbents have successfully argued against third-party access, claiming that regulated third-party access, such as in Singapore, may create disincentives for investment in natural gas infrastructure and hamper energy security. As a result, regulators have tended to promote investment over access. Lack of downstream competition has also led to LNG shippers and LNG terminal owners signing long-term supply contracts, which make it more difficult for newcomers to enter the market.

Natural gas market liberalisation in Japan has been ineffective. The country has rules in place for market liberalisation, such as retail price liberalisation for the non-household sector and third-party access rules. However, natural gas market reform has been piecemeal. Third-party access rules have not been complemented by mandatory unbundling or by other measures to increase competition in downstream retail markets. If the market were to be liberalised, reform is needed on all fronts: while effective third-party access facilitates competition, the lack of downstream competition has prevented third-party access from being effective.

Energy security remains the primary policy priority. Japan’s regulatory regime cannot focus on minimising costs as vigorously as that of countries with more favourable fundamentals, such as China, which has greater energy security and can build a national transmission network.

Key lessons from Japan’s experience of developing and regulating its midstream LNG infrastructure include:

-

Japan has unique energy fundamentals that make midstream assets very important. The country had no domestic production of gas and few other domestic sources of energy, and its mountainous geography limited the development of a national transmission network. As a result, energy security was a high priority, and LNG terminals played the role of a transmission network by providing access at points along the coastline.

-

Japan has experienced large investments in midstream assets. Japan has invested in a large number of LNG terminals, which were warranted from an energy security and geography perspective. Incumbents have successfully argued against third-party access, claiming that regulated third-party access, such as in Singapore, may create disincentives for investment in natural gas infrastructure and hamper energy security. As a result, regulators have tended to promote investment over access.

-

Gas market liberalisation in Japan has been ineffective. Japan had rules in place for market liberalisation, such as retail price liberalisation for the non-household sector and third-party access rules. However, in practice the market remained uncompetitive, with four companies supplying more than 70% of natural gas and almost all LNG terminals owned by a small number of companies with no meaningful third-party access.

-

The failure of liberalisation demonstrates the importance of regulating across the value chain. Gas market reform in Japan has been piecemeal. Third-party access rules have not been complemented by mandatory unbundling or by other measures to increase competition in downstream retail markets. If the market were to be liberalised, reform is needed on all fronts: while effective third-party access facilitates competition, the lack of downstream competition has prevented third-party access from being effective.

2.5 Case Study 3: The United States—Master Limited Partnerships

In the United States, a unique corporate structure, master limited partnerships, enables ownership of midstream assets to be reallocated to owners with appropriate risk profiles. The structure facilitates the transfer of midstream assets from organisations focused on high-risk, high-return activities, such as oil and gas exploration and development to organisations seeking low-risk, low-return assets, such as pension funds. While the case study focuses on oil pipelines, it is applicable to midstream infrastructure more generally.

Key lessons from the US experience with master limited partnerships include:

-

Midstream assets are low-risk, low-return assets and can attract significant investment. Once constructed, midstream assets such as pipelines have a relatively simple business model, especially in markets with high demand and regulated charges, such as the United States. Such assets were attractive to investors comfortable with low-risk holdings and a regular return, such as pension funds.

-

Greater capital liquidity enables better allocation of capital. Many midstream assets were constructed by companies with a greater appetite for risk and higher return expectations, such as domestic and international oil companies with upstream assets, as a way of transporting wellhead natural gas to consumers. However, these companies specialised in higher-risk, higher-return investments. Instruments such as master limited partnerships enabled these companies to sell midstream assets to investors with more appropriate risk profiles and recycle the proceeds into new investment more consistent with their own risk-reward profile.

-

Tax efficiency is important in attracting investor interest. A master limited partnership is a particular form of business entity that is not liable for US federal income tax. Allowing midstream assets to be structured into a master limited partnership reduced tax liability and improved the returns, therefore increasing investor interest.

-

Regulation gives clarity and certainty, further enhancing capital liquidity. Beyond the corporate structure, master limited partnerships in the United States have benefited from a clear, credible and stable regulatory regime, which has created confidence among investors less familiar with the energy industry. Regulated access charges, a history of long-term contracts, and a stable regulatory and tax regime helped lower the risk of an investment and attract new capital.

-

1.

Background

The United States is the world’s largest oil consumer. The level of domestic crude oil production has increased over the past few years, reversing a decline that began in 1986. According to the IEA, crude oil production increased from 5 million barrels a day in 2008 to just less than 5.7 million barrels a day in 2011 and 6.5 million barrels a day in 2012. This increase in oil production was largely brought about by new seismic and horizontal drilling technology and hydraulic fracturing, bringing domestic resources that were previously considered non-viable into production.

Pipelines are the common transport mode for shipping crude oil and refined products. In total, the country has more than 275,000 km of crude-gathering and distribution pipelines, operated by 2338 companies. The top 10 operators alone run almost 90,000 km of pipeline. In 2011, this network delivered 514.3 million barrels a day of crude oil between regions. The highest concentration of pipelines is in the Gulf Coast, which is also home to almost half the country’s refining capacity.

Because of the capital-intensive nature of pipeline operations, many companies have sought to structure these units as master limited partnerships, publicly traded businesses that are taxed as partnerships. Unlike a corporation, a partnership in the United States is classified as a pass-through entity and is not liable for federal income taxes. Instead, partners pay tax based on their allocated share of the partnership. The structure offers two significant advantages. First, tax is levied only at a single level of federal income tax, which is applied individually on the total income of each member of the partnership. The master limited partnerships do not pay corporation tax. The other advantage is that favourable tax treatment allows a master limited partnership to access lower-cost capital than if it were taxed as a corporation.

These advantages make the master limited partnership approach an especially attractive option for capital-intensive pipeline infrastructure transmission enterprises.

-

2.

Benefits to infrastructure owners

One example of the structure was Shell Midstream Partners, a master limited partnership that held onshore and offshore oil infrastructure. Three of the four pipelines in its portfolio served the Gulf Coast, while the fourth reached into the Northeast (Fig. 19.15).

Shell midstream partners pipelines

For the infrastructure owner, a particular advantage of this corporate structure is that the business retains control of the pipelines. Unlike shareholders in a publicly traded company, unitholders—investors holding shares of master limited partnerships—are not entitled to elect the general partner or any directors. Instead, they benefit from a stream of income in accordance with their ownership interest, while the partnership itself is managed by a board of directors and executive officers appointed by a general partner, in this case Shell Pipeline Company LP, an affiliate of Shell. The distribution of ownership interests varied across the pipelines in the portfolio (Table 19.3).

Launching an initial public offering for Shell Midstream Partners allowed Shell to release capital for investment elsewhere in its value chain and optimise its risk profile. It also allowed Shell to divest itself of low-return, non-core assets and to improve its focus on other activities. At the same time, investors in Midstream Partners, such as pension funds, were attracted by its lower risk-return profile.

-

3.

Importance of the regulatory framework

The regulatory framework provided certainty for investment by detailing eligible assets and activities. Master limited partnerships were only possible as a result of the regulatory authorities providing rules for partnership treatment: federal rules on qualifying income and assets gave Shell the necessary certainty to proceed. It also enabled Shell to offer stable and predictable cash flows to investors. Rules on access meant that Midstream Partners’ assets generated stable revenue under FERC-based tariffs and long-term transportation agreements. In addition, ship-or-pay contracts mitigated volatility in cash flows by limiting exposure to changing market dynamics that could reduce production and affect shipper demand. Finally, life-of-lease agreements, some of which have a guaranteed return, reduced cash flow exposure to volume reductions.

3 Unbundling Midstream Infrastructure

Midstream infrastructure unbundling is a critical step in natural gas market liberalisation progress and in the promotion of natural gas market competition. This section analyses the effects of unbundling with the background of natural gas market liberalisation as well as related goals of unbundling. In addition, a comparison of five partition models is carried out using case studies from the United Kingdom, the European Union and Japan. These case studies offer experience and a reference point to China in its future unbundling work.

Natural gas markets have historically been dominated by large vertically integrated companies operating across the various segments of the value chain. Vertically integrated pipeline owners face particularly strong incentives to engage in anti-competitive behaviour, charging excessive rates to third-party natural gas shippers for access to midstream infrastructure to protect profits in their own production or retail businesses.

Unbundling seeks to separate the incentives facing midstream operations from those of upstream and downstream operations and to reduce the opportunity and incentives for anti-competitive behaviour. Without this, owners of midstream assets will retain an incentive to operate in a way that favours their upstream or downstream businesses. Unbundling focuses on the midstream segment because of its natural monopolies and the potential for misusing market power (Fig. 19.16).

Unbundling is the separation of midstream business from that of upstream and downstream business

Full ownership unbundling is the most complete form of unbundling, although some models of unbundling seek to change these incentives without separation of ownership. For example, if a single vertically integrated firm participates in the upstream segment, transportation and retail sales, but regulation effectively prevents it from operating its midstream assets to the advantage its upstream or downstream businesses, vertical integration does not threaten efficient market operations.

Unbundling is a key step in natural gas market liberalisation, as part of a broader effort to create open access to midstream infrastructure, particularly to pipelines which have stronger characteristics of natural monopolies. Unbundling is required in addition to third-party-access regimes. Third-party access requirements address the incentive of a natural monopoly owner to charge very high prices to maximise its profits, reducing pipeline utilisation in the process. Unbundling requirements, on the other hand, address the incentive for vertically integrated owners to make monopoly profits by favouring their vertically integrated partners and excluding third parties.

Vertically integrated companies can misuse their market power even if third-party access to midstream assets is allowed, for example through a lack of transparency over available capacity and prices or through onerous contracting or technical studies requirements for third parties. Such anti-competitive behaviour can be remedied by strict policing of third-party access rules, but removing the incentive for this behaviour through unbundling has been seen by many regulators as a part of the solution. Unbundling is not itself the goal, but rather a means to ensure that third-party access is effective. The success of an unbundling regime should be measured by the ultimate effectiveness of an open access reform package in supporting an efficient and competitive gas market.

3.1 Models of Unbundling

Five unbundling models are defined and examined using case studies from the United Kingdom, the European Union and Japan. They are:

-

Service unbundling: Businesses must offer use of their midstream assets as a distinct service separate from the wholesale supply of natural gas.

-

Account unbundling: Midstream businesses must maintain separate accounts from upstream and downstream businesses to prevent cross-subsidisation and distorting behaviour.

-

Legal unbundling: Midstream assets are placed into a separate legal entity, such as a wholly-owned subsidiary, to reinforce the operational separation of these assets from other assets within a vertically integrated entity.

-

Structural unbundling: Strict regulatory requirements are placed on how a midstream business is operated to ensure that it supports the efficient operation of the natural gas market, rather than to the benefit of related upstream or downstream interests.

-

Ownership unbundling: The legal entity that owns midstream assets does not have common ownership with upstream or downstream interests, fully separating their economic incentives.

Each of these models builds sequentially on each other, alongside an overarching process known as functional unbundling, which can reinforce each of these models. Functional unbundling restrictions can vary from being fairly mild to quite onerous. They could include, for instance, requiring separate management, locations, support units and logos, prohibiting the sharing of information, and imposing additional compliance and reporting requirements. Functional unbundling is a critical element of any unbundling process. To illustrate, a legally unbundled midstream business that shared management or offices with a related upstream or downstream business could be less effective than, say, a midstream business that legally remained part of a vertically integrated entity, but had more rigorous separation of staff and management.

Each of the five models of unbundling serves different purposes and follows sequential changes in moving from service unbundling to ownership unbundling (Table 19.4).

3.2 Key Insights from the Case Studies

Our review of international experience in unbundling midstream assets from upstream and downstream businesses produced three general insights that might be valuable to China’s policy discussions.

-

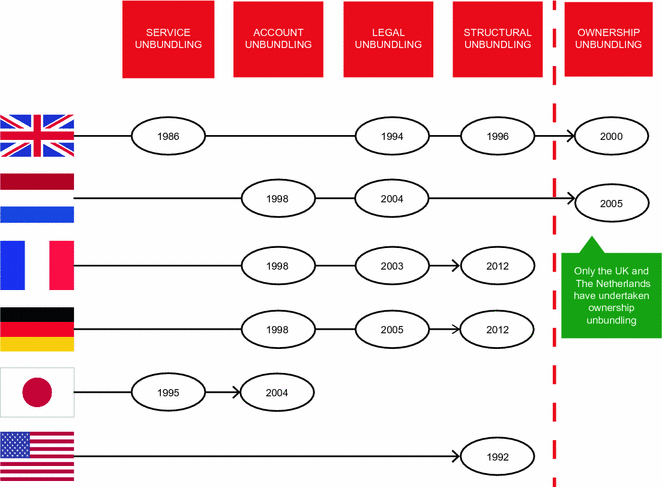

Complete ownership unbundling is not necessary under a strong regulator. The case studies indicated that there are viable models that don’t require full ownership unbundling. In particular, structural unbundling under a strong regulator could capture many of the benefits of full ownership unbundling. Of the country case studies, only the United Kingdom and The Netherlands pursued full ownership unbundling. France and Germany argued for structural unbundling that fell short of full ownership unbundling, and the latest EU Gas Directive included this option along with strong regulatory measures to enforce a well-developed structural unbundling model. Experience in the United States also suggested that a competitive natural gas market can be supported without mandatory ownership unbundling, provided the operations of transmission companies are tightly prescribed. Each of these cases followed a unique path to unbundling (Fig. 19.17).

Fig. 19.17

The path of unbundling (ultimate ownership rights unbundling might not be necessary)

In general, structural unbundling can be effective if the regulator is strong. However, anything less than structural unbundling is likely to be inadequate in delivering liberalised natural gas markets. The experience of the United Kingdom and Japan indicated that service unbundling alone offered few benefits and that service and account unbundling, combined with meaningful functional unbundling, was the minimum viable unbundling models. However, this combination of unbundling models should be seen as a stepping stone to deeper unbundling, rather than an end point. The European experience also indicated that legal unbundling offered little without moving to deeper structural unbundling, complemented with functional unbundling.

These observations suggest a streamlined unbundling process consisting of three steps (Fig. 19.18). Functional unbundling supports this process at key junctions, principally in the account, legal and structural unbundling phases.

Fig. 19.18

Streamlined unbundling process (three steps only)

-