Abstract

At different stages of the development of the natural gas industry, markets exhibit different characteristics depending on the different levels of competition and different problems encountered, and thus the focus of reforms should also differ. In general, no stage in the reform process can be left out, as each key issue must be dealt with effectively to ensure that policy and adoption of measures keep step. This approach should achieve a balance between the three aspects of timing, location and quantity.

* This chapter was overseen by Xiaoming Wang from the Development Research Center of the State Council and Mallika Ishwaran from Shell International. It was jointly completed by Yusong Deng, Jiaofeng Guo, Shouhai Chen from China University of Petroleum and Qingle Wu from Shell China. Other members of the topic group participated in discussions and revisions.

You have full access to this open access chapter, Download chapter PDF

Similar content being viewed by others

1 Roadmap

At different stages of the development of the natural gas industry, markets exhibit different characteristics depending on the different levels of competition and different problems encountered, and thus the focus of reforms should also differ. In general, no stage in the reform process can be left out, as each key issue must be dealt with effectively to ensure that policy and adoption of measures keep step. This approach should achieve a balance between the three aspects of timing, location and quantity. Attention should also be paid to the special characteristics of the natural gas industry sector and to the extent of the effects of the reforms and the uncertainties relating, for instance, to market conditions. Taking all these factors into account, the increase in the extent of reform occurring in the natural gas sector in China should take place at a gradual pace and to a moderate degree, so that the reforms are acceptable to society. Appropriate objectives and measures should be determined based on the stage of development reached by the natural gas market and according to its specific characteristics. For the purposes of this paper we envisage a gradual roll-out involving three stages.

1.1 Upstream Sector Roadmap

Currently the vast majority of oil and gas mineral rights are concentrated in the hands of four major corporations: China National Petroleum Corporation, China National Offshore Oil Corporation, China Petrochemical Corporation and Shaanxi Yanchang Petroleum Group. Resolving this problem of excessive centralisation of mineral rights, resulting in control over land being awarded but no exploration taking place, is key to advancing reform in the upstream field. As a result, reforms need to start by looking at current legislative and administrative methods, concentrating on promoting diversification of investors, encouragement of effective competition and creation of a restriction list, in order to refine the system of market access, ensuring that a system for issuing tenders and bidding on quotas is implemented for natural gas mineral rights; this in turn will result in the orderly and effective encouragement of the creation of primary and secondary markets for exploration rights and extraction rights, at the same time as ensuring that basic data on natural gas resources is placed in the public domain.

-

1.

By 2020, the preliminary creation of a mineral rights primary and secondary market should have taken place. This will involve the creation and refinement of a legislative system and framework with a “mineral resources law” at its centre. Restriction list, industry admission and competence baseline administrative systems will be established, allowing companies that are viewed as “competent” to import gas independently (pipeline gas and LNG) in addition to allowing freedom of choice of importer. This will also include the preliminary creation of a public-domain natural gas resources information management system, which will also include newly discovered Chinese gas hydrates mineral resources, while also involving introduction and refinement of a system for tendering and bidding in relation to conventional natural gas, shale natural gas, coalbed methane, gas hydrates and other such mineral rights and the preliminary creation of an exploration and extraction rights secondary market system and trading mechanism. The natural gas wellhead (ex-works) price will be deregulated and then decided by market competition, while the natural gas pricing method will be based solely on calorific value pricing. Amalgamation and integration of the main state oil companies will occur, according to experience gained overseas in terms of balancing development upstream, midstream and downstream, resulting in the creation of two or three vertically integrated large international oil companies, the upstream, midstream and downstream operations of which are equally balanced. This will allow the growth of an effective, competitive market structure, in addition to establishing and refining a specialised independent regulator.

-

2.

By 2025, establish the basic elements of a primary and secondary mineral rights market. Establish a legislative system with an “oil and gas law” at its centre. Refine the restriction list and industry admission regime. Create a public-domain natural gas resources information management system. Create a regime for tendering and bidding on conventional natural gas, shale natural gas, coal bed gas, gas hydrates and other such mineral rights, including the preliminary creation of an exploration and extraction rights secondary market system and trading mechanism. Complete the honing and specialisation of the independent regulator.

-

3.

By 2030, primary and secondary mineral rights markets should be fully established. A comprehensive legislative system based on an “oil and gas law” should have been established. A highly effective administrative implementation structure based on a restriction list and industry admission regime should have been created. A strict supervisory system relying on an independent specialist regulatory body should have been established. An integrated, orderly but competitive, legal, trustworthy, effectively regulated natural gas exploration and development market system should have been established.

1.2 Midstream Roadmap

Currently, Chinese oil and natural gas long-distance pipelines, branch pipelines and provincial pipelines are mainly concentrated in the hands of three major corporations (China National Petroleum Corporation, China National Offshore Oil Corporation and China Petrochemical Corporation). How to resolve the issues of the low numbers of participants involved in pipeline construction and operation, the bundling of transport and sales and a lack of third-party access are all key issues encountered in relation to overall reform of the midstream field. As a result of this, it is necessary to commence work regarding current legal and administrative systems, concentrating efforts in the areas of diversification of market participants (this in turn will encourage effective competition), creation of a restrictions list and improve market admission mechanisms. In this way, the complete separation of long-distance pipeline, branch pipeline and provincial pipeline transport services and sales operations will be ensured, so that the reform objective of third-party access to pipeline networks and open admittance to the industry can be achieved. Admittance to sectors where natural monopolies exist, such as the pipeline networks, charging and cost supervision should also be strengthened.

-

1.

By 2020, allow preliminary pipeline capacity trading in a primary market, including the trading of storage capacity such as that within LNG installations. Ensure that reforms are implemented that make natural gas pipeline network finances independent, with the trial introduction of independence of production rights from the natural gas pipeline network. Enforce third-party access and open industry admittance. Completely separate long-distance pipeline, branch pipeline and provincial pipeline transport and sales services. Establish and refine an independent specialist regulator.

-

2.

By 2025, the creation of a primary pipeline capacity and storage trading market should be basically complete, in conjunction with the preliminary creation of a secondary pipeline capacity and storage trading market. Ensure that the independence of the natural gas pipeline network from production rights has been accomplished and that the objectives of third-party access and open industry admittance have been achieved. In order to encourage the construction of pipelines and gas distribution networks and increase transport capacity, permit long-term natural gas supply and transport contracts (although gradual pricing regulation of transport and distribution networks would be necessary). Implement policies giving pipeline investment and construction projects that are of proven benefit to society and that have a major social influence immunity for limited periods (for instance by not enforcing third-party access to pipeline transport services for a specified period of time). Ensure that a specialised independent regulator is fully in place and refined.

-

3.

By 2030, ensure the formation of both primary and secondary pipeline capacity and storage trading markets. Implement third-party access to distribution services, while allowing residential and commercial clients to seek out alternative suppliers or wholesalers other than their local distributor, either via the introduction of trials or as part of a compulsory process. Create a restriction list and an industry admission administrative regime which will act as the foundation of an effectual administrative implementation system. Create a strict supervisory system based on a specialised independent regulator. Ensure that this results in an integrated, competitive, ordered, legal, trustworthy natural gas pipeline and storage market system which is effectively regulated.

1.3 Downstream Roadmap

China has already begun to establish downstream market structures, and in overall terms it is possible to see the existence of market competition to differing degrees. However, there are still a lot of problems, requiring solutions for issues such as irregularities in market regulation, incomplete pricing mechanisms, poorly developed market structures and localised monopolies, all of which are key areas of concern in ensuring thorough reforms in the downstream sector. As a result, work needs to begin on the existing legislative and administrative systems, concentrating efforts in the following areas: the formation of market systems; encouraging effective competition; the creation of a restrictions list and improving market admission mechanisms; and the deregulation of natural gas terminal pricing, with prices then being established by market competition. This should finally result in the formation at the national level of around 10 regional oil and natural gas spot trading markets, as well as establishing and refining a natural gas futures trading market, ending in the establishment of a fully featured, modern market and associated regulatory structures.

-

1.

By 2020, ensure the deregulation of natural gas terminal pricing, which will subsequently be determined according to market competition. Establish natural gas spot trading markets and wholesale markets at the main natural gas trading centres and provincial distribution hubs. Establish a natural gas trading market within the Shanghai Futures Exchange. Create and refine an independent specialised regulator.

-

2.

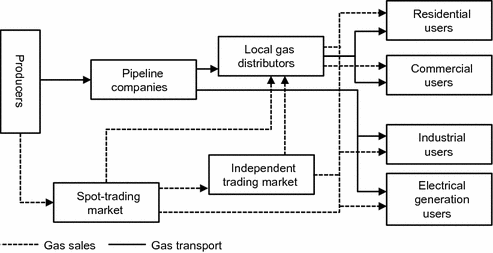

By 2025, ensure the development of a natural gas sales market system based on a combination of producers, independent traders, large users, local distributors and end users that rely on a spot trading market. Create and refine an independent specialised regulator (Fig. 14.1).

Fig. 14.1

Diagrammatic representation of the natural gas markets after complete separation of sales and pipeline transport. Source Xu (2015)

-

3.

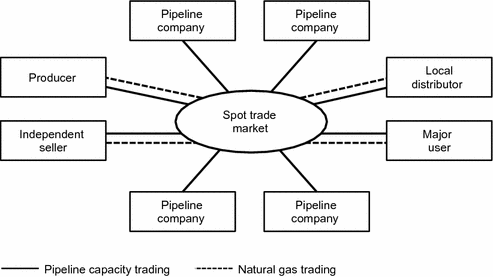

By 2030, a natural gas sales market system based on a combination of producers, independent traders, large users, local distributors and end users that rely on a combined natural gas market system consisting of a natural gas spot trading market and a natural gas futures market should have been established. Create a specialised independent regulatory body as part of a strict regulatory system. Ensure that this results in an integrated, competitive, ordered, legal, trustworthy natural gas sales market system which is effectively regulated (Fig. 14.2).

Fig. 14.2

Diagrammatic representation of a spot trading market system. Source Xu (2015)

2 Key Measures

The basic direction of China’s natural gas policy it that it “supports energy efficiency, strengthens China’s position, encourages diversification, is concerned about the environment, ensures thorough reforms, encourages international co-operation and improves the lives of everybody”. This approach promotes transformation in terms of energy resources and modes of production and consumption, and forms the basis of a clean, efficient, safe and sustainable modern industrial system, placing complete reliance on the sustainable development of energy resources to support the sustainable development of the economy and society as a whole.

2.1 Creation of Market Systems

Efforts must be made to ensure that by 2020, an integrated, open, competitive and orderly natural gas combined production/transport/sales market system which encompasses “one network, diversified gas sources and 10 regions” has been created.

A “one network” pipework transport system is required in order to allow connection of gas resources from different sources and regions to the market, thus creating a national unified natural gas market system, which will encourage the flow of resources between the markets of different regions, and allowing effective competition, helping to ensure the security of natural gas supplies. To be specific, it will be necessary to create a pipeline backbone by perfecting the current “Western Gas Going East” system, the new Guangdong-Zhejiang and Shaanxi-Beijing systems, the “Sichuan Gas Going East” system and the China-Burma pipeline networks, while the Lanzhou-Yinchuan (Lan-Yin) line, Lanzhou-Yinchuan-Ningxia (Lan-Yin-Xia) line, Huaiyang-Wuhan (Huai-Wu) line, Zhongwei-Guizhou (Zhong-Gui) line and the Ji-Ning line act as connecting lines to create a “one network” pipeline transport system.

-

1.

“Diversified gas source” gas supply framework

China’s main natural gas market resource is state-produced gas from the Xinjiang, Sichuan-Chongqing, Qinghai and Shaanxi-Gansu-Ningxia regions as well as from maritime areas, in addition to gas imported from Central Asia via pipelines located in the west, gas imported via the northern China-Russia pipeline and imported LNG. Due to the need to concentrate on placing reliance on nearby supplies, more consideration needs to be given to a framework relying on “piping of western gas east, delivery of gas from the north to the south and bringing maritime gas ashore”, ensuring that full use is made of a variety of market resources to satisfy the gas supply demands of various regions in order to ensure security of supply.

-

2.

“Top 10” regional markets

Due to the factors affecting the distribution of natural gas resources, the layout of the pipeline network and existing socioeconomic conditions, the hope is to establish a seamless network in China connecting imported pipeline gas to the markets, connecting LNG receiving stations to the markets, connecting producing regions to the markets, connecting underground gas reserve storage to the markets and connecting producing regions with underground gas reserve storage. By around 2020, 10 large regional markets based on the Bohai Loop, Yangtze River Delta, Pearl River Delta, Sichuan-Chongqing, Yunnan-Guizhou-Guangxi, Central-Southern, Shandong-Henan-Anhui, Central-Western, North-Western and North-Eastern regions will be created, including:

-

a locally supplied market to feed local production and consumption in Sichuan-Chongqing and the North-Western region, with Shanghai and Guangdong acting as production-transportation-consumer centres for the Yangtze River Delta and Pearl River Delta regional markets;

-

Zhongwei in Ningxia, Wuhan in Hubei and Yongqing in Hebei acting as logistical hubs in the creation of Central-Western, Central-Southern and Bohai Loop regional markets, while gas from the China-Russia pipeline and pipeline gas produced domestically will come mainly from the gas source for a North-Eastern regional market;

-

gas from the China-Burma pipeline and imported LNG acting as the gas source for the Yunnan-Guangxi-Guizhou regional market, with the underground gas storage groupings of the Yellow River Plain and northern China providing support to locally produced pipeline gas and imported LNG and gas from other sources in the Shandong-Henan-Anhui regional market.

These “Top 10” regional markets are not completely independent but are interconnected and influence each other. This is achieved via a “single network” pipeline transport system connecting different pipelines and different entities in addition to effective market regulation, encouraging effective competition, and ensuring that market resources can spontaneously flow from high-value areas to low-value areas, thereby establishing a national pricing system based on different regional prices and a flexible natural gas market framework, in turn ensuring the optimised allocation of resources.

The creation and developmental progression of these “Top 10” regional markets should occur sequentially, by policy-led trial introduction. From the point of view of market creation and developmental progression, the relatively mature Sichuan-Chongqing, Yangtze River Delta and Pearl River Delta regional markets should be established within the time constraints of the 13th Five-Year Plan. When compared at the national level to other regional markets, the Sichuan-Chongqing region was the earliest regional natural gas market established in China, relying mainly on the Sichuan Basin, which is rich in oil and natural gas resources as well as having a relatively well established pipeline transportation network; this would make it much easier for a relatively mature market to become established. In light of this, it is recommended that a “Sichuan-Chongqing natural gas market reform trial zone” be established as soon as possible, with the results achieved in this trial allowing the creation of a mature regulatory system as far as market access and pricing mechanisms are concerned, which should be capable of overcoming inertia in the developing market and obstacles to effective competition, while allowing the market to play a definitive role. This in turn will allow the creation of a natural gas market with a 100 billion m3 annual output capacity and a 70 billion m3 annual sales volume.

Take full advantage of the economic advantages of the production-transport-sales centres of Shanghai and Guangdong and their ability to sustain prices and other such market advantages, which should allow for the rapid development and operation of a Shanghai oil and natural gas trading exchange. This will allow Shanghai and Guangzhou to act as pricing centres, making the creation of relatively mature regional markets in the Yangtze River Delta and Pearl River Delta districts possible within the time frame of the 13th Five-Year Plan. At the same time, by relying on the Ningxia Zhongwei, Hubei Wuhan and Hebei Yongqing natural gas distribution hubs and making full use of the advantages offered by distribution network nodes, it will be possible to gradually develop logistical systems so that they radiate out into surrounding areas, establishing these as oil and natural gas circulation and logistical centres, and allowing the formation by 2020 of relatively mature Central-Western, Central-Southern and Bohai Loop regional markets. Using this as the foundation, construction of the Yunnan-Guangxi-Guizhou, Shandong-Henan-Anhui, North-Western and North-Eastern regional markets will then be possible.

This activity should take place in conjunction with the construction of the “Top Six” subterranean gas storage groups. These rely on depleted oil and gas reserves, and depend on suitable storage conditions existing within the oil or gas deposits and create value from waste resources. The Central Plain, northern China, the North-East, Changqing, the North-West and the South-West oil- and gas-producing regions will form six major subterranean gas storage groups. These groups will gradually create and optimise a natural gas reserve peak adjustment system, which will be a major factor in the creation of China’s “single network, with diversified sources and 10 regions”.

By harmonising planning, construction and usage of natural gas markets, resources and infrastructure, it will be possible to create an integrated national upstream-midstream-downstream combined production-transport-sales market system, ensuring that development of the natural gas industrial chain occurs evenly at all levels.

2.2 Completion of a Natural Gas Pricing Mechanisms

-

1.

Staged introduction of reforms to natural gas pricing

Currently, preliminary work has been carried out regarding the introduction of a dynamic mechanism for pegging natural gas prices against alternative energy sources. Considering the special circumstances of the natural gas industry, the widespread implications of reforms and the uncertainties concerning market conditions, it is recommended that, depending on the stage of development encountered in the natural gas market, reforms to natural gas pricing should advance steadily.

In the first stage, between 2015 and 2017, the emphasis should be on the creation of a pricing system. Application of the netback method should be introduced as soon as possible (including adjustment of the pricing coefficient K from 0.85 to 0.70–0.75). Determine the costs and pricing of long-distance pipeline, branch pipeline, provincial pipeline, urban pipeline and distribution network pipework transport in a scientific and acceptable manner. Establish residential gas pricing in the light of basic economic factors. Refine implementation methods to allow for seasonal price variations, peak and trough price variations, interruptible supply pricing and gas storage pricing. Revise measurement standards and valuation methods (conversion from a flow rate or mass valuation method to a calorific valuation method), and increase administrative and technical monitoring of illegal valuation activities. Bring an end to the charging irregularities occurring at local government levels (such as the current natural gas pricing adjustment fund, with local governments exacting this at rates that vary between 0.3 CNY and 1.0 CNY per cubic metre, which results in additional burdens being placed on the consumer).

In the second stage, between 2018 and 2020, remove all regulation of gas source pricing, including all provincial gate station pricing. Enhance regulation over residential use gas prices. Enhance the regulation of charging for use of such infrastructure as gas transport pipelines and gas storage, ensuring that there is effective regulation in relation to sector admission.

In the third stage, between 2021 and 2023, charging for all gas transport pipelines except gas distribution networks and for gas storage should be completely determined by the market. Complete introduction of supervisory and administrative systems with regard to pipeline networks and other infrastructure, ensuring that the objectives of allowing open, fair, orderly competition with regard to natural gas prices are achieved. In addition, policy should be formulated concerning the introduction of a financial and taxation system relating to resource tax, environmental tax and carbon tax. This will ensure that a suitable scientific financial taxation system and pricing mechanism is put in place, which will reflect the growing scarcity of resources, the relationships of market supply and demand and the costs of external environmental impact.

-

2.

Accelerated creation of regional trading centres

In the short term, the Shanghai and Guangdong natural gas trading centres could be established. In the mid to long term, new regional trading centres could be established in Beijing, Sichuan, Hubei, Ningxia and Xinjiang. Efforts must be made to ensure that the Shanghai natural gas trading centre becomes both an Asian and international natural gas trading centre, resulting in the Shanghai trading centre system eventually becoming the centre for trading of both internationally priced and regionally priced gas, thus effectively creating a link between domestic and international supply and demand. The creation of natural gas trading centres should commence with spot trading, then the range and quantity of trading should be expanded, finally developing into futures trading, increasing the depth of the market.

2.3 Removal of Pipeline Transport Bottlenecks

The supervision of the operation of natural gas infrastructure such as pipeline networks should be extended, clearly establishing functional roles, to ensure that pipeline transport services and sales services are completely separate and that third-party access is facilitated.

The emphasis should be on reform to the natural gas pipeline network construction and operational systems, establishing functional roles within pipeline networks, and gradually resulting in a natural gas pipeline network to which fair access is provided, driven by supply and demand and which is both reliable and flexible. The formulation of policy in relation to market admittance in terms of pipeline network operation and services should be accelerated; this should involve the introduction of an admittance system of operator accreditation, ensuring the suitability of operators to undertake certain functions and duties. The basic requirements for operators will be the existence of an independent legal body corporate, and implementation of independent financial accounting systems. In light of the actual circumstances of China’s natural gas industry, the separation of provision of infrastructure services could commence first with the relatively easily reformed long-distance pipeline network and LNG receiving stations. As for how to approach separation, this could begin with financial and legal separation. Then, as the extent to which reforms are adopted increases, it would be possible to institute trials in the eastern regions, where there is a greater diversity of gas sources, where competitive market structures are more or less already in place and where there is a relatively high density in terms of gas transport pipeline networks. This would be followed by a nationwide expansion. In addition to all this, an exploratory separation of the financial systems and legal status of gas storage services from gas distribution networks should be carried out. Such a change would encourage varied investment in the construction of gas storage capacity, allowing independent storage operators to participate in the natural gas market and profit from market peak and trough pricing differences.

Implementation of pipeline network interconnectedness allowing connection of third-party services should occur rapidly, and more effort must be put into the regulation of connection contracts, service pricing and quality of service—this will encourage the creation of the conditions necessary for market competition.

In the gas transportation and LNG receiving station sector, the scope of long-distance pipeline and LNG receiving station third-party access should be gradually expanded. Also, a permit administration system should be introduced, allowing any accredited operator of natural gas services to sign transport or storage contracts with pipeline networks and LNG receiving stations. Under such circumstances, when excess capacity in the distribution network systems arises, operators of pipeline networks and LNG receiving stations must offer this to any natural gas supplier or user who has need of such services, thus providing a non-discriminatory service based on fair pricing. Within the main pipeline backbone, all gas source input nodes and market terminals should be interconnected, removing any obstruction to the circulation of natural gas products. In terms of application, depending on the extent to which infrastructure has been developed and the degree of separation that has occurred between services and sales, it would then be possible to gradually introduce negotiable and subsequently obligatory third-party access. At this point, it would be essential to promote gradual deregulation (in terms of annual natural gas consumption), allowing large users to choose their natural gas suppliers directly (“large users” being urban gas companies, 200,000 kW power stations, combined cooling, heating and power generation stations, large-scale industrial companies (including for use as fuel and as a raw material) and LNG/CNG fuel suppliers, among others).

Regarding storage and urban gas distribution, third-party access mechanisms should be gradually introduced to users at different scales of consumption. Start with non-residential customers with fairly high annual consumption; this should result in a timetable and establish annual consumption scales. Then introduce freedom of choice of gas supplier to non-residential users according to different annual consumption levels while adhering to this timetable and depending on the extent of overall implementation of the previous measures. Alternatively, it would be possible to completely avoid urban pipeline distribution networks, or such urban networks would only be allowed to provide gas distribution services according to government regulated prices.

2.4 Further Regulatory Reform

Gradually set up a comprehensive, centralised, vertically unified, integrated, independent, specialised regulatory system, with fully established regulatory functions, and put more effort into establishing regulatory powers.

At different stages in their energy development, the United States and European nations each introduced an independent regulatory body. The US established both an energy administration and an energy regulator. The energy administration mainly has responsibility for fundamental policies relating to the development of energy resources and safety and for related policy research. The energy regulator mainly has responsibility for formulation and implementation of specific regulatory policy. In terms of its market regulation, this includes a staged upstream-midstream-downstream regulatory process. Although there is no regulatory committee for the upstream field, the federal government’s Department of the Interior is responsible for regulation relating to production and use of energy sources, while individual states carry out the regulation of certain types of permit in upstream manufacturing. There are, however, independent regulators at both the midstream and downstream levels, with FERC being responsible for the regulation of state-level pipeline transport and sales regulation, while state public utility regulatory committees carry out regulation of downstream energy structures. These legally established regulatory bodies have adjudicative powers and are independent of the government, making them a more effective guarantee of the implementation of government policy regarding energy resources. Their open, fair, transparent, legal principles make them more accessible to public scrutiny.

Establish independent regulatory bodies and clarify their regulatory responsibilities. Fully extend their regulatory functions, providing greater regulatory functionality. The energy-related regulatory system should be established as soon as possible. Enhance energy-related regulation. Create and complete the structure of regulatory organisations and related legislation, involving regulatory innovation, thus allowing improved regulation efficiency and ensuring the fairness and stability of the markets. This will help to create a healthy environment within which to develop the energy industry.

2015–2017: Complete and perfect harmonisation of the regulatory system. After establishing the relevant regulatory legislation, statutes and standards in conjunction with state energy development planning and strategy and energy industry policies, the different departments concerned should enhance communication in order to harmonise their work and co-operation. During the course of the implementation of the regulatory system, all departments should ensure enhanced sharing of information and co-operation. At the same time, it will be necessary to establish the functions and duties of each regulatory department in relation to central government and local organisations.

2018–2020: The State Council will deputise an energy regulation leadership group, which will be responsible for harmonising work between different departments and gradually establishing a relatively centralised regulation department. Each department will retain its original regulatory legislation, standards and functions, while the main burden of regulatory implementation will gradually be transferred to one organisation, which will then provide a relatively centralised regulatory service. At the local level, government will only establish a regulatory organisation consisting of a single level of administration, which will then dispatch specialist regulatory teams to various locations. In addition, the central regulatory department will be responsible for monitoring and supervision of local regulatory organisations.

2021–2023: Complete and refine the functions of a unified regulatory organisation. Apart from its role of regulation of the environment and national resources, this will gradually be endowed with full regulatory responsibility for the economic and social aspects of the entire energy industry chain. At this point a system of interaction between different departments will be clarified and their individual duties established and an independent, unified regulator will gradually be created. Finally, establish a system with an independent, unified, specialised regulator and vertical regulatory administrative organisations at different levels.

Enhance reforms in terms of social accountability and monitoring, with enhanced monitoring of present and future development and promotion of a system of market supervision based on standardised and procedural regulatory measures. Impose a system of unified market supervision, eliminating and discarding all regulations and practices that obstruct the creation of a national unified market and fair competition. Make better use of the government, in order to ensure that legal concepts and methods are applied to the adoption of market regulatory functions, with enhanced monitoring of present and future development and promotion of a system of market supervision based on standardised and procedural regulatory measures.

-

1.

Enhance the role of government regulation

Completion and optimisation of standards and norms is vital. Accelerate the pace of work on the formulation and actualisation of regulatory legislation and technical standards and norms relating to all aspects of natural gas development, transport, storage and distribution. Complete and refine an environmental impact evaluation system, including evaluation of strategic environmental impact, evaluation of environmental planning impact and dynamic evaluation of the impact of construction projects related to development, transport, storage and distribution of oil and natural gas.

Enhance the overall regulation of the complete oil and natural gas development process, involving strict regulation in the pre-development stage, during development and in the post-development stage. Pre-development regulation should include planning and preparatory work in relation to oil and natural gas development, ensuring that all safety and environmental hazards are rooted out. At the stage when companies or contractors draft oil and natural gas development projects, they should also draft an oil and natural gas environmental impact report, which should make proposals relating to implementing measures to avoid or reduce all types of pollution. At the same time, companies undertaking development projects should be required to establish baselines in terms of the main environmental indicators (such as subterranean water quality, surface water quality, air quality and so on) prior to commencing work, and continuous monitoring should be carried out during the course of development. Well locations must be based on detailed geographical surveys, avoiding where possible densely populated areas, areas where environmental protection orders apply and so on, all the while reducing damage to the local land and using land more effectively. Where possible, pre-existing infrastructure should be relied on, thus reducing the need for the construction of new roads and infrastructure.

Regulation during development mainly relates to the drilling of oil and natural gas wells, their completion, gas extraction and normal operation. Contractors should be required to satisfy safety and environmental regulation standards and norms at all times and in all aspects of their work, adopting efficient, green, recyclable technology, all the while ensuring environmental protection and safety. At the same time, they should ensure that contractors are capable of responding effectively to prevent environmental pollution, that they have emergency protocols and that they provide anti-pollution equipment.

Post-development regulation mainly relates to the evaluation of the long-term risks resulting from the development of oil and natural gas. In the course of development of oil and natural gas it is possible that environmental factors which were not easily perceived pre-development and during development may arise. In the post-production phases it is necessary to carry out analysis of subterranean water, surface water, soil and air and other such aspects of the environment. These samples should be compared with pre-development baseline levels, allowing an appraisal of the environmental impact of oil and gas development. Post-development regulation must be strictly enforced, and companies that do not satisfy standards should be punished accordingly.

Special consideration should be given to safety and environmental protection as regards midstream pipelines:

-

During pipeline construction, it is necessary to audit the legality and qualifications of prospective designers, suppliers and contractors. During the pipeline design, supply and construction process, there should be close monitoring for adherence to state safe production legislation and technical standards. Pipes and safety infrastructure should be scientifically selected and constructed, in order to root out any safety flaws that may exist in pipework. Companies responsible for distribution and delivery of oil and gas should have a safety executive in place, and ensure that suitable personnel and equipment is provided, ensuring the step-by-step creation and optimisation of a safe pipeline network and allocation of production safety responsibilities.

-

Oil and gas pipeline safety work should be included within the scope of day-to-day government administration, establishing a comprehensive, scientific and sensible regulatory system, further enforcing specific responsibility for safety management in relation to pipeline installations. This should implement a system whereby responsibility for this lies with local leadership, thus establishing effective and enforceable procedures in relation to public safety. A system harmonising the work of various departments, the government and pipeline companies needs to be established, such as a system of joint progress consultations. The next level of government above will be responsible for harmonising response in terms of cross-boundary safety issues, and this will include establishing a system of responsibilities for all related government departments and pipeline companies, fully implementing a safety information sharing system and rapid safety event response system.

-

Those responsible for illegal appropriation and excavation and other actions that represent a serious threat to the safety of oil and gas pipelines will be held accountable, and any organisations or persons found responsible will be dealt with.

-

2.

Enhanced enforcement of the safety and environmental responsibilities of enterprises

Establish a comprehensive safe production supervisory and administrative body and regime. Enterprises must set up safe production committees and safety management departments, which should be staffed with appropriate managerial staff. In addition, enterprises must establish a comprehensive production safety management system, including a system of production safety duties, a system of safety instruction, a safety meeting system and a safety equipment management system, including a safety incentive and penalty system and emergency response system.

Clarify production safety duties, providing a comprehensive production safety duty regime. Enterprises must establish a comprehensive production safety duty system, based mainly on job responsibilities, with the person with overall responsibility at its centre, which establishes who has overall responsibility for production safety and consists of a system of production safety duties applicable to staff involved in all departments and activities, thus forming part of the overall production safety monitoring and duty system.

Strengthen safety management in relation to specialist technology. Strengthen safety management in relation to specialist technology on the basis of production safety legislation, standards and norms.

Institute a safety troubleshooting regime, thereby enhancing preparation for emergencies. Enterprises must carry out intermittent potential accident troubleshooting on the main aspects of the production process, the main points of activity and main items of equipment used. Where any potential accident areas are found, these should be subjected to specialist evaluation, categorisation and pre-emptive restrictions and special precautions. It is necessary to establish a strict potential accident reporting regime, standardising potential accident control work. Where accidents occur, it is necessary to have an effective emergency response organisation and specifically formulated responses, which should be practised in the course of day-to-day operations.

Introduce a health, safety and environment (HSE) management system and a pipeline integrity management system. HSE management is particularly concerned with the safety of operative activities, safeguards and operational safety, while pipeline integrity management systems are specifically concerned with equipment and technical management and preventative maintenance in order to ensure the safe and reliable operation of equipment. By effectively integrating the functions of these two roles, allowing them to complement each other, it is possible to create a new pipeline management system. This not only enhances HSE management systems, but also increases the level of safety management, supervision and the professional skills of auditing personnel and is an extremely effective approach to safety.

-

3.

Increased openness of information and public scrutiny

Openness of information and public scrutiny should be standard throughout the entire process of oil and natural gas production, transportation and usage. Government departments should provide effective guidance and carry out effective supervision of work on the openness of company data and public scrutiny. This work should concentrate on providing open, honest descriptions of any environmental, safety or health issues related with production, transport and usage processes, and the response of the company concerned to such risks. Furthermore, the government should rapidly publish safety and environmental testing data, and should make communication with local residents a part of all stages of the development process, ensuring that residents are fully aware of any challenges, risks or benefits that may arise as a result.

NGOs and other civil society organisations should be active in carrying out public scrutiny, to establish whether or not the companies concerned respect environmental standards, while also holding regulatory bodies accountable. The public should be aware of environmental issues, and have a full appreciation of the safety issues and environmental risks associated with oil and natural gas production, transportation and usage, thus allowing them to play a role in the public scrutiny of oil and natural gas production, transport and usage. The media should play a role in the dissemination of environmental knowledge and the exposure of illegal activities. Where media reports are critical, they should require companies to carry out investigations into the veracity of the claims and resolve the issues in question. In addition, companies should then provide reports within two weeks to the relevant departments and news organisations regarding the results of rectification work they have undertaken or the progress of their investigations.

2.5 Further Reform of the State-Owned Oil and Gas Companies

State-owned oil and gas companies played a dominant role in The Netherlands before reform, making the situation very similar to that encountered in China. Despite having created a unified energy market according to EU requirements, due to path dependence, The Netherlands adopted a different development approach. This approach involved the retention of a number of major state-controlled upstream, midstream and downstream enterprises, while EBN, a completely state-owned company with special characteristics, stepped in and took control over operation of the oil and natural gas markets, a step which proved to be an effective measure.

The evidence proves that the presence of state-owned enterprises does not necessarily mean the presence of a monopoly or low efficiency. However, there does need to be specialised supervision and management in order to improve operational efficiency, which under fair market conditions will effectively promote the entry of social capital. The background of China’s development from a planned economy to a market economy as well as features such as the strategic position of gas resources and their exploration and development, the high-risk nature of pipeline transport and delayed returns on investment have determined that in order to ensure the security and supply of oil and gas, involvement and investment by state-owned enterprises is, at present, essential. Especially from the point of view of natural monopolies and important public goods and service sectors, dominance by state-owned enterprises should continue for a certain period of time. However, at the same time it is important to encourage effective competition through diversification of investment and improvements in tendering and bidding structures.

There is a need to optimise the allocation of resources afresh, while remodelling the core competitiveness of the enterprises concerned, in order to create oil companies that satisfy basic rules of structural proportions in terms of the upstream and downstream sectors that apply throughout the global oil and gas industry. This will result in the creation of international oil and gas companies that are more competitive internationally, which will in turn improve the standing of China’s oil and natural gas industry, as well as providing greater national energy security. Between two and three international oil and gas super-companies which have balanced development in terms of the upstream, midstream and downstream sectors should be established. At the same time, in order to ensure that suitable conditions exist for effective market competition to occur, after merging, such unified international super-companies should then hive off part of their midstream and downstream businesses.

Simultaneously with this restructuring, if state-owned oil and gas companies are to converted into satisfactory market participants, then there will need to be a deepening of reforms. This process would mainly require the completion and refinement of state-owned asset supervision and administration systems and operational systems, so that government’s various functions can be separated: social and economic, asset ownership management, state-owned asset management and state-owned asset operation. This would achieve separation between government and business enterprises and between government and assets, resulting in the creation of efficient operational mechanisms and governance structures, which would encourage the management of state-owned enterprises to conduct managerial activities and operations based on market forces, thus encouraging greater activity by state-owned enterprises.

2.6 Establish and Improve the Services Market

The experience of the United States in its successful development of shale natural gas shows that multiple investors and combined development systems for specialised services can mobilise the positive aspects of venture capital, technology research and development, upstream extraction, infrastructure, market development and end applications, as well as put in place a system for the implementation and improvement of the regulatory system to ensure the rapid and orderly development of the shale natural gas industry. In an open and competitive environment, there are advantages that may be exploited, such as increased specialisation and access to technology within the technological services industry, providing horizontal drilling, well completion and cementing and multi-stage hydraulic fracturing services to rights owners etc., as well as professional and technical services for engineering, logging and experimental testing. After a company completes a service in relation to a specific aspect, it can then be replaced by another company that specialises in the next aspect. A high degree of division of labour allows for splitting of shale natural gas extraction operations into individual aspects, requiring less investment, with shorter operating cycles and a faster recovery of funds, attracting a large amount of venture capital and private capital into the shale natural gas field.

Market mechanisms must therefore be allowed to play a complete role. This will provide a strong impetus for the development of oil and natural gas-related professional services and technology companies, in line with the principles of “production requirements, advanced technology and a good reputation”. Market mechanisms and qualifying constraints can be used to regulate service enterprises and their activities, organising specialist construction teams, while establishing new systems founded on “exploration, production, site operations, costing, safety and the environment”. All the while, procedural regulation of production processes and standardised operations will ensure effective and orderly exploration and extraction.

At the same time, the training of professional personnel needs strengthening. Sustainable development depends on the personnel of the oil and gas industry, so competition between enterprises is ultimately competition using human resources. It is therefore necessary to establish professional resources for China’s oil and gas market—and, indeed, for the international market. Not only is there a need for experts with a great deal of management and technical expertise, they also need to be encouraged to expand their proficiency to legal matters and international trade, resulting in a relatively stable human resource system which encompasses all the professions required.

Author information

Authors and Affiliations

Consortia

Corresponding author

Editor information

Editors and Affiliations

Rights and permissions

Open Access This chapter is licensed under the terms of the Creative Commons Attribution 4.0 International License (http://creativecommons.org/licenses/by/4.0/), which permits use, sharing, adaptation, distribution and reproduction in any medium or format, as long as you give appropriate credit to the original author(s) and the source, provide a link to the Creative Commons license and indicate if changes were made.

The images or other third party material in this chapter are included in the chapter's Creative Commons license, unless indicated otherwise in a credit line to the material. If material is not included in the chapter's Creative Commons license and your intended use is not permitted by statutory regulation or exceeds the permitted use, you will need to obtain permission directly from the copyright holder.

Copyright information

© 2017 The Editor(s) and The Author(s)

About this chapter

Cite this chapter

Shell International and The Development Research Center., Ishwaran, M., King, W., Haigh, M., Lee, T., Nie, S. (2017). Roadmap for Natural Gas Market Liberalisation and Regulatory Reform. In: China’s Gas Development Strategies. Advances in Oil and Gas Exploration & Production. Springer, Cham. https://doi.org/10.1007/978-3-319-59734-8_14

Download citation

DOI: https://doi.org/10.1007/978-3-319-59734-8_14

Published:

Publisher Name: Springer, Cham

Print ISBN: 978-3-319-59733-1

Online ISBN: 978-3-319-59734-8

eBook Packages: Earth and Environmental ScienceEarth and Environmental Science (R0)