Abstract

The Gulf of Mexico offers ample opportunities to both commercial and recreational fishermen. Long-term landings of most key commercial species appear to be stable. Changes in landings are often tied to regulations to manage fish stocks. For the analysis of Gulf fisheries, a 20-year period from 1990 to 2009 was chosen as inclusive of (1) pre- and post-management agency changes, (2) active tropical storm periods, (3) challenging production cost situations, and (4) high and low points in the national economy. This approach acknowledges that a species’ stock level and economic conditions of inputs and demand play roles in landings levels. A 3-year average was used to depict landings and associated value. Increasing imports has led to progressive decline in brown and white shrimp fisheries where employment has dropped from 109,000 in 2007 to 63,000 in 2009 and revenues have dropped from $2.5 billion to $1.7 billion. The Gulf shrimp-processing sector has experienced a steadily eroding marketing margin that has culminated in consolidation of this sector.

You have full access to this open access chapter, Download chapter PDF

Similar content being viewed by others

Keywords

10.1 Introduction

The users of the Gulf of Mexico living marine resources are as diverse as the species and habitats. Depicting the economic components both annually and over time generally is based on agency-collected data primarily focused on landings. The revenue element of use being well documented serves commercial industry analyses partially and leaves a void that confronts recreational industry researchers. Missing critical elements for depicting economic conditions include, but are not limited to, production costs, expenditures by anglers, site-specific data, marketing and processing prices, and margins. Research at universities, by consultants, and within agencies on various economic issues occurs on a project basis. Project studies do not occur consistently enough over time on any species, much less a large enough component of Gulf of Mexico species, to be relied upon for the increasingly complex mix of decisions faced by agencies. Agencies in turn must be responsive to harvesters and increasingly strong regional and national nongovernmental organizations (NGOs). Agencies, users groups, and NGOs face decisions that include habitat protection, avoidance of indirect impacts of harvest gear, access, determining initial catch shares, allocations, law enforcement, and juxtaposition with other agency regulations. The existing data reporting system relied on for this chapter cannot be expected to adequately serve economic researchers addressing the range of inquiries associated with commerce in fisheries. Special projects of short duration from various funding sources most likely will be necessary to meet the needs of participants in the decision-making process. This chapter makes use of the data reporting systems maintained by agencies. State agencies in the Gulf of Mexico are generally unified in their reporting via agreements founded by the Gulf States Marine Fisheries Commission (GSMFC). This congressionally authorized commission has an increasing presence in organizing fisheries data and providing Internet access in a timely manner. Of particular interest is the GSMFC’s role in specific analyses focused to fill special needs. The most recent example is commitment to a multiyear economic study of the inshore commercial shrimping sector. This economic analysis fills a void and has added value as it can be coupled with findings of National Oceanic and Atmospheric Administration (NOAA) Fisheries’ research. Beginning in 2006, NOAA Fisheries began an annual economic survey of federal Gulf of Mexico shrimp permit holders that provides valuable insight over time of the region’s largest commercial fishery. Essentially all other economic perspective of Gulf of Mexico commercial fisheries must be ascertained from annual NOAA and GSMFC reports interspersed with irregularly funded special projects.

When addressing the complexities of the angler harvest of Gulf of Mexico species, economists are no richer in terms of data sources. The core source of most reports is the Marine Recreational Fisheries Statistics Survey (MRFSS), which was later renamed the Marine Recreational Information Program (MRIP). Established in 1979, the MRFSS evolved over the years into a system reflective of the difficulties associated with estimating (1) catch by species, (2) participants, (3) fishing by location, (4) target species, (5) fishing mode, and (6) expenditures by anglers. The use of the database was undertaken with knowledge of changes made over time to improve not only the representativeness of the data but also access. It is noteworthy that the state of Texas does not participate in the annual MRFSS/MRIP survey. Consequently, all discussion of catch by species, participation, and trips made by anglers are exclusive of Texas. However, there is Texas data on angler expenditures and related multipliers included from other sources to make that section as complete as possible. The recreational fisheries are addressed on the basis of economic activities associated with the pursuit of fish. Expenditures and associated indirect impacts springing from multiplier effects must serve as both the cost of angling and the base from which gross benefits can be estimated.

This chapter deals with the complexity of angling with attention to the Gulf of Mexico and state levels inclusive of species-specific findings to give the best possible descriptive background of the marine recreational fisheries. With the understanding that the commercial harvest of Gulf of Mexico fish species is a capture and sale process, there can be minimal comparability with the pursuit of recreational fisheries in terms of economics. Decisions on the use of Gulf of Mexico marine fish species will remain an interesting public process as data improves and economic analyses become more numerous with attention to both descriptive and analytical needs. Beginning with a review of federal, regional, and state management, a review of the commercial and recreational fishing industry in the Gulf of Mexico will be presented in general and for specific, commercially and recreationally important marine species. With respect to the commercial sector, emphasis is given to analysis of the shrimp, crab, menhaden (Brevoortia patronus), oyster, and reef fish industries. Recreationally important marine species for which special emphasis is given include spotted seatrout (Cynoscion nebulosus), red drum (Sciaenops ocellatus), groupers, snappers, and coastal pelagics. This review also includes estimates of expenditure and cost multipliers associated with input–output analyses. This assessment will focus first on the commercial fishing industry followed by the recreational angler-based industry. The chapter ends with a review of the Florida, Mississippi, Alabama, and Louisiana harvests since they represent major recreational fishing foci. A summary of the results of this review is presented in the final section of this chapter.

10.2 The Management Process at Its Base

The mobility of most living marine resources pursued for harvest results in three levels of public entities—federal, state, and regional—being involved in management for the sustainable flow of benefits. Federal, state, and regional responsibilities established by law are approached by entities with similar but not uniform authorizations. Often, agencies charged with the management of fisheries resources in the Gulf of Mexico evolve with expanded abilities to influence the use of marine species. Criteria for guiding the public use of fishery resources can be found in legislation but more frequently in regulations promulgated by agencies. It is beyond the needs of this document to detail the regulations and authority by which agencies act to move resources toward sustainability. Agency websites can be searched for insight to the origin of authorizing legislation and current status of species-specific management activities.

10.2.1 Federal Oversight: National Oceanic and Atmospheric Administration

Of the agencies, the federal level is the most subject to change. Passage of the Fishery Conservation and Management Act (FCMA) in 1976 began an increased level of oversight at the federal level. The passage was associated with many prior years of numerous nations extending fisheries oversight to 200 miles (mi) (322 kilometers [km]). Fishery management councils were authorized around the nation. The membership of the Gulf of Mexico Fishery Management Council (GMFMC) included (1) state fishery agency representatives from Florida, Alabama, Mississippi, Louisiana, and Texas, (2) citizens appointed by the U.S. Secretary of Commerce from nominations by the region’s governors, and (3) NOAA Fisheries’ regional director. GMFMC develops fishery management plans for species common to the federal Exclusive Economic Zone (EEZ). Plan development evolves from guidelines established by federal legislation with frequent amendments necessary due to changing (1) use patterns, (2) technologies of fish harvesting, (3) legislation, (4) data, and (5) analysis methodologies. NOAA has final authority to approve, modify, or deny any amendment to a fishery management plan emanating from the GMFMC.

10.2.2 State Agency Management

The five states with Gulf coastal borders have authority to manage fishery resources on the basis of their preferred regulatory approaches to achieving goals. All have similar goals regarding conserving living resources for sustainable use over time. Though the focus is on state waters, there is the need for substantial interaction and cooperation with other states and the GMFMC. The movement of many species at critical life phases to waters of other Gulf States and waters seaward of state coastal boundaries necessitates formal working relationships to assure oversight throughout the various habitats. Seaward coastal boundaries vary from 9 mi (14.5 km) in Texas and the west coast of Florida to the traditional 3 mi (4.8 km) for the other three states on the Gulf. State agencies have designees on the GMFMC to convey local regulatory perspectives in the federal fishery plan development process. When species are totally within state waters or move laterally along the coast, coastal state regional coordination is authorized through the GSMFC.

The shrimp fisheries exemplify complexity for the management structure in the Gulf. The shrimp industry in Louisiana waters produces the Gulf’s largest landings in pounds. Agency management approaches involve a large inshore fishery and harvest of smaller shrimp sizes (i.e., a larger number of shrimp to the pound at harvest). The management from Texas’ state agency, Texas Parks and Wildlife, is for a lessened inshore catch and cooperative management with the GMFMC for larger-sized shrimp (i.e., fewer shrimp to the harvested pound).

Texas is unique among the states in that it has a voluntary commercial fishing license buyback program. The license buyback programs for bay shrimp, blue crab (Callinectes sapidus), and finfish seek to stabilize fishing efforts through time in order to promote healthy fisheries stocks. Funds for the buyback come from a surcharge on related commercial fishing licenses and a saltwater fishing stamp endorsement to recreational licenses.

10.2.3 Gulf States Marine Fisheries Commission

Acknowledging the joint interest of coastal states to achieve multiple goals for management of mobile fishery resources, Congress authorized the formation of multistate commissions in 1949. Utilization of fishery resources to meet food, employment, economic, and recreation needs of citizens was reasoned to be facilitated by use based on conservation and a multistate oversight. The GSMFC includes 15 commissioners to oversee the implementation and evaluation of efforts to coordinate management among Gulf States. Each governor appoints a commissioner and each state legislature appoints one as well. The other five commissioners are the state fishery agency directors.

Though the GSMFC does not have direct regulatory authority, it clearly has been successful in stimulating deliberations leading to cooperative planning, data programs, and research. An understanding of the key role that fishery data improvement plays in goal achievement for the Gulf has been a visible part of GSMFC actions. While there are many GSMFC programs, the creation of fishery-independent and fishery-dependent data collection programs serve to prove the value of regional cooperation. The former is termed the Southeast Area Monitoring and Assessment Program (SEAMAP). The latter comprises two elements: (1) Commercial Fisheries Information Network (ComFIN) and (2) Recreational Fisheries Information Network (RecFIN). A common element of both the ComFIN and RecFIN programs is an emerging program to administer collection of economic information on Gulf fisheries.

Following the active hurricane year of 2005, Congress assigned the GSMFC a leadership role in recovery programming. A 5-year program began in 2006 to oversee rehabilitation and recovery efforts. This emergency assistance to Gulf States established a format for action that resulted in valuable experience on enabling fisheries agencies to respond with coordinated programs.

10.3 Gulf of Mexico Commercial Fisheries in Aggregate

10.3.1 Gulf of Mexico Landings

The capture of free ranging marine species for commercial use occurs from a large area subject to both within-year and between-year variability in environmental and economic conditions. Environmental conditions including water temperature, salinity, and turbidity—in conjunction with the life cycles of many of the species that inhabit the Gulf—all contribute to availability. Species availability, in conjunction with those economic conditions that determine whether a trip will be profitable, including the price received for the harvested product and the cost of inputs used in the harvesting process, provide signals to the harvesting units as to whether a trip will be financially viable. This viability along with the multitude of regulations that can also govern fishing patterns influences fishing effort, and ultimately the catch. Considering this, landings of a specific year cannot be descriptive of Gulf fisheries from either a biological or economic viewpoint. For this chapter, the 20-year period from 1990 to 2009 was chosen as inclusive of (1) pre- and post-management agency changes, (2) active tropical storm periods, (3) challenging production cost situations, and (4) high and low points in the national economy. This approach acknowledges that a species’ stock level and economic conditions of inputs and demand play roles in landings levels. This perspective conveys a need to avoid reference to beginning-year and end-year comparisons. Rather, a 3-year average was used to depict landings and associated value as the beginning and end focus of comments. There is a distinction between location of landings and location of catch. This is particularly the case for the shrimp fisheries and most finfish. Location of catch is best documented for Gulf shrimp fisheries by offshore zones east to west across the Gulf and by inshore versus offshore. When data are available to differentiate landings from catch, that data is reported in the sections dealing with key species. Data by state are also reported in the key species sections.

In the latest 3-year period, 2007–2009, landings of all species combined were 1.4 billion pounds (Figure 10.1). This was 10 % lower than the initial 3-year period (1990–1992). With respect to the nation’s total fisheries, Gulf landings were near a 16 % share at the start and end of the 20-year period. Both U.S. and Gulf landings fell over the 20-year period to leave the Gulf shares essentially unchanged.

Gulf of Mexico commercial fishery landings, 1990–2009 (NMFS FSD; data accessed 2012—see Appendix A) (Note: 1 lb = 0.454 kg)

The Gulf landings share for the key species—menhaden, brown shrimp, white shrimp, blue crab, and oysters—demonstrate the national significance of the region’s fisheries. These key species accounted for 94 % of Gulf landings in the latest 3-year period. While other species, primarily finfish, are harvested, their trends do not convey overall change in Gulf landings.

10.3.1.1 Menhaden Landings

The menhaden fishery landings for the 20-year period ranged from a high of 1.7 billion pounds in 1994 to a low of 0.8 billion pounds in 2005 (Figure 10.2). The average was a 21 % decrease for the nation. The resulting Gulf share of national landings was 69 %. Essentially all menhaden landings occur in Louisiana (80 %) and Mississippi (19 %) for the industrial production of fish meal and oils. However, this is a case where there is some divergence due to catch location. Some Louisiana landings occasionally are caught off Texas. Mississippi landings can originate from Louisiana and vice versa.

Gulf of Mexico commercial menhaden landings, 1990–2009 (NMFS FSD; data accessed 2012—see Appendix A) (Note: 1 lb = 0.454 kg)

10.3.1.2 Brown Shrimp Landings

Landings of brown shrimp (whole weight) ranged from a high of 168 million pounds in 1990 to the period low of 79 million pounds in 2008 (Figure 10.3, left panel). The average landings on the basis of the 3-year groupings decreased 27 %. With Gulf landings accounting for 95 % of U.S. production, national landings were then down 27 %.

Gulf of Mexico brown shrimp (left panel) and white shrimp (right panel) landings, 1990–2009 (NMFS FSD; data accessed 2012—see Appendix A) (Note: 1 lb = 0.454 kg)

10.3.1.3 White Shrimp Landings

Annual white shrimp landings ranged from the period high of 132 million pounds in 2006 to the period low of 55 million pounds in 1996 (Figure 10.3, right panel). The average annual landings, on the basis of the 3-year groupings, increased 41 %. U.S. landings showed a smaller increase (30 %) when the non-Gulf landings decrease (20 %) was included. The Gulf’s increased white shrimp production for the period almost negated the lower production from the brown shrimp fishery, which left total shrimp landings essentially unchanged.

10.3.1.4 Blue Crab Landings

Statistics are reported for three blue crab products: (1) hard blue crab, (2) peeler crab, and (3) soft crab. Hard blue crab is, by far, the target of harvesters. Peeler is a designation for a crab in molt stage that results in a soft crab that can be marketed. Only hard blue crab landings are addressed herein, because it is the largest commodity form and also would reflect changes in levels of the other forms (Figure 10.4). The Gulf crab fishery accounts for 35 % of domestic landings with the remaining landings from Chesapeake and South Atlantic areas. Gulf landings, examined in 3-year intervals, began the period of analysis at almost 65 million pounds (i.e., 1990–1992 average) and ended the period at 56 million pounds (i.e., 2007–2009 average) for a 14 % decrease (Figure 10.4). National landings fared worse with a 26 % decrease.

Gulf of Mexico commercial blue crab landings, 1990–2009 (NMFS FSD; data accessed 2012—see Appendix A) (Note: 1 lb = 0.454 kg)

10.3.1.5 Oyster Landings

U.S. landings of eastern oysters (Crassostrea virginica) were essentially unchanged for the period at 24 million pounds of meat. The initial 3-year average was 23.9 million pounds of meat, and the final 3-year period average was 24.4 million pounds of meat. Gulf oyster harvesters produced 13.7 million pounds in the initial period but the average for the final 3-year period rose to 22 million pounds (61 % increase) (Figure 10.5). The 22-million-pound level for the Gulf represents 90 % of the country’s eastern oyster landings.

Gulf of Mexico commercial oyster landings, 1990–2009 (NMFS FSD; data accessed 2012—see Appendix A) (Note: 1 lb = 0.454 kg)

10.3.1.6 Landings of All Other Species

Dozens of species have not been covered in the aggregate discussion of the Gulf. Although comprising approximately 6 % of total landings, many of the species are the focus of GMFMC regulations. The reef fish complex of species includes many that are subject to technically defined designations of “subject to overfishing” and/or “overfished.” As of 2009, gag grouper (Mycteroperca microlepis), gray triggerfish (Balistes capriscus), greater amberjack (Seriola dumerili), and red snapper (Lutjanus campechanus) were being managed so designated. Given the overfishing or overfished designation associated with these species, landings are constrained by regulation and significant changes in landings of these species are unlikely in the absence of a change in regulation. Changes in regulations generally reflect updated stock assessments indicating improvements/deteriorations in the health of the stock. Reef fish complex species generally entail involvement of commercial and recreational harvesters. This adds a complexity to the understanding of Gulf fisheries not present in the previously presented key species. There are small recreational harvests of oysters, blue crab, and shrimp in relation to commercial landings that are not problematic. Anglers for Gulf reef fish species are major participants in quota sharing and likely have a wider distribution throughout the Gulf landing sites than the far smaller number of commercial harvesters. More detailed discussions of the commercial harvest of reef fish species and the recreational harvest of reef fish and other species are given in subsequent sections of this chapter.

10.3.2 Aggregate Landings by State

The finfish and shellfish landings attributed to the states fluctuate as expected, yet the ranking of the states within the Gulf does not change much (Figure 10.6). Louisiana ranks first due to landings in five major species: (1) menhaden, (2) brown shrimp, (3) white shrimp, (4) blue crab, and (5) oysters. Landings are commonly above a billion pounds with menhaden accounting for 80 %. Mississippi attains the second highest landings also fueled by the menhaden fishery with a 94 % component. Most recently the west coast of Florida ranks fourth after historically holding the third spot. Landings in Texas placed third at the end of the 1990–2009 period. Alabama began and ended the period in fifth place. Differences by species among the states are presented in the sections dealing with individual key species.

Average annual landings by state, 1990–1992 and 2007–2009 (NMFS FSD; data accessed 2012—see Appendix A) (Note: 1 lb = 0.454 kg)

10.3.3 Catch by Distance from Shore

The diversity of species in the Gulf subject to commercial harvest results in many being caught either totally or partially in state waters. State waters is reported in the NOAA Fisheries as 0–3 mi (0–4.8 km) offshore even though Florida has a 9 mi (14.5 km) state limit on its west coast as does Texas throughout its Gulf border. Total catch for the Gulf can be portrayed as near a 50 %–50 % split between state and federal waters (Figure 10.7). Mississippi receives the highest level of state water catch at 88 %. At the other extreme, Texas receives 81 % from the 3–200-mi (4.8–322-km) zone, largely because of a large offshore shrimp component. Louisiana, Alabama, and Florida (west coast) were nearer to receiving equal shares from state waters and offshore zones. The Gulf’s large menhaden fishery generally conveys a shallow water image consistent with state waters. This accurately fits for Mississippi with 88 % of the state’s catch coming from state waters. The situation is not so described in neighboring Louisiana even though the harvest methods are the same. Louisiana, with 53 % of total catch from federal waters, can only attain such a level if menhaden comprises a large part of the catch.

Gulf of Mexico commercial catch by distance from shore, by state, in percentage (left panel) and pounds (right panel), 1990–2009 (NMFS, Fisheries Statistics Division with percentage calculations by authors; data accessed 2012—see Appendix A) (Note: 1 lb = 0.454 kg)

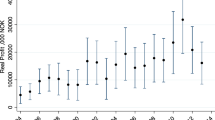

10.3.4 Dockside Value of Landings

Gulf fisheries brought in $658 million (i.e., dockside value), on average, for the last 3 years of the 1990–2009 study period. The first 3-year average for the period was $568 million for an 18 % increase in nominal terms. The high single year was 2000 with value at $997 million (Figure 10.8). The last year of the period had value at its lowest over the 20 years. Value increased while landings decreased 10 %. Key species values were mixed: (1) oyster value increased 89 % under increased supplies of 61 %, (2) blue crab landings were 14 % lower with a value increase response of 59 %, (3) menhaden landed value was 15 % higher on 9 % lower landings, (4) white shrimp value was up 24 % on much higher landings of 41 %, and (5) brown shrimp was 37 % lower on a drop of 27 % in landings. Recall that these are for 3-year averages at the start and end of the 1990–2009 period.

Gulf of Mexico dockside value of commercial landings, 1990–2009 (NMFS FSD; data accessed 2012—see Appendix A)

NOAA Fisheries maintains an ex-vessel price series with 1982 as the base year (i.e., 1982 = 100). The ex-vessel price indexes for blue crab, oysters, menhaden, and Gulf and South Atlantic shrimp are good descriptors for the Gulf. However, none of the edible finfish from the Gulf have price indexes. The substitute index used herein is that of total edible finfish in the country. Edible finfish ex-vessel prices in 1990 had an index of 130 but ended at 117 in 2009. The interpretation is that overall finfish ex-vessel prices were 30 % higher in 1990 compared to 1982 but only 17 % higher by 2009. The index for blue crab was at 152 in 1990 with a large increase to 383 by 2009. Oyster harvesters were successful marketing in 1990 at prices that put the index at 228, the highest index for the key species. By 2009, the oyster index reflected more favorable conditions with an index of 273. Ex-vessel prices in the vertically integrated menhaden industry are estimated from a small number of firms. The index levels in 1990 and 2009 were 128 and 154, respectively. The situation for shrimp necessitated that all warm water shrimp be used in the calculation, not just the brown and white shrimp noted previously in this chapter. Brown and white shrimp commonly comprise over 95 % of landings. For 1990, the index was 79 signaling a 21 % decrease from the 1982 base. Although there were occasional exceptions for the 20-year period, the index reflected poor ex-vessel shrimp prices. Economic conditions by 2009 were not favorable, resulting in an index of 65 (i.e., price was 35 % below 1982).

When examined at the state level, the dockside value of all landings is highly concentrated in Louisiana and Texas with shares of 43 % and 26 %, respectively. The other state achieving a double-digit contribution is Florida (west coast) at 19 %. Alabama and Mississippi range from 6 to 7 % of Gulf value. Species components of the state values are widely different. Louisiana value of individual fisheries for white shrimp, blue crab, oysters, and menhaden leads among the states. For example, the commercial dockside value of Louisiana’s white shrimp landings averaged $96.3 million annually during 2007–2009, which exceeded the combined values for all other states (Figure 10.9 left panel). Similarly, the 2007–2009 annual average commercial value of Louisiana’s blue crab landings ($34 million) and oyster landings ($43.4 million) exceeded the combined landings from all other Gulf states (Figure 10.9 right panel). The remaining key species, brown shrimp, is dominated by Texas landings (with an average dockside value of $87.8 million during 2007–2009), followed by Louisiana ($29.2 million) and Alabama ($21.8 million) (Figure 10.9 left panel). Key species designation of the five species fits well for all but Florida (west coast). At 19 % of total Gulf value, the area only receives 11 % of its landed value from key species. Edible finfish such as groupers and snapper bring high finfish dockside prices. These species and highly valued spiny lobster (Panulirus argus) and stone crab (Menippe mercenaria) claws push the west coast’s share in the Gulf (19 %) past that depicted by key species alone (3 %).

Value of commercial landings by state and species (shrimp, left panel; oysters and blue crab, right panel), (2007–2009 average) (NMFS FSD; data accessed 2012—see Appendix A)

10.3.5 Processing Plants and Related Employment

The after-landings activities necessary to convert marine shellfish and finfish into marketable consumer products in varied locations around the country are substantial. A consumer product can be as basic as one in whole form that has been washed, graded, and temperature safe to labeled frozen product at retail. With the majority of seafood consumption occurring away from home, the product processing can result in an intermediate form that allows chefs final value-added opportunities in restaurants. Estimation of total employment in such a marketing chain when imported products as well as fresh seafood imports account for large shares of supply is not attempted on a times series basis. A substitute is the use of an input/output model that accounts for activity created throughout the economy as a result of an initial sale. The next section describes economic impacts of sales, income, jobs, and value added based on an input/output model developed for NOAA.

There are minimal data available annually on the domestic processing industry. NOAA’s annual report Fisheries of the United States includes the number of processing and wholesale plants with direct employment estimates. Indirect and induced employment estimates are not included. The state of Florida data are reported without differentiation of east and west coasts. Therefore, data to be discussed are for the non-Florida Gulf. For the 2007–2009 period, Gulf States averaged 163 processing plants and 231 wholesaling plants. The range for processing plants during the 3 years was small at 160–165 indicating stability in the near term. As expected, wholesaling plants were more numerous, in part due to the lower capital cost. The range for wholesaling plants during the 3 years was smaller at 229–232. There likely was more entry and exit in the wholesaling sector than the narrow range suggests due to the lower capital entry costs. Louisiana was home to both the largest number of processors and wholesalers (72 and 176, respectively). Mississippi had the lowest number of plants. However, in terms of employment, Mississippi led the Gulf States. Approximately one-third of the region’s employment can be identified as Mississippi based. Average plant employment in Mississippi amounted to three times the level of the next highest Gulf state, Texas.

10.3.6 Economic Impact of Gulf of Mexico Commercial Fishing

Economic impacts to be portrayed include those of sales, income, and value added originating from landings and imports. The initial use of the National Marine Fisheries Service (NMFS) Fishing Industry Input/Output Model was applied to 2006. Annual analyses followed with a value-added calculation made in 2009. Thus, there are findings for the 2007–2009 period previously used to depict near term conditions with respect to landings. Separate information for the Florida west coast versus Florida east coast was not available. The Gulf economic impacts of landings had to be reported for Alabama, Mississippi, Louisiana, and Texas to avoid inconsistencies with the prior sections dealing with landings and this impact, with and without the inclusion of imports, is presented in Figure 10.10 for 2009. This represents the first year in which NMFS segmented imports from domestic product in the calculation of economic impacts.

Gulf of Mexico commercial seafood industry economic impact, 2009 (U.S. Department of Commerce 2011)

10.3.6.1 Sales Impacts

An input/output model measures the impacts of an economic impetus, in this case the value of landings, on other sectors in a defined economy or region. Impacts estimated include the effects of domestic landings, imported seafood, wholesaling, processing, and retail on an economy. In this case the impact generated $4.6 billion from Alabama, Mississippi, Louisiana, and Texas. For the 2007–2009 period, average annual sales impacts by state, including both domestic and imported product, were (1) Alabama, $441 million; (2) Mississippi, $348 million; (3) Louisiana, $1.9 billion; and (4) Texas, $1.9 billion.Footnote 1 All four states experienced a sales impact decrease from 2007 to 2009. Using the 3-year period, landed value average results in a higher impact estimate for sales than if 2009 alone was calculated. Importers accounted for 41 % of the seafood industry’s Texas sales impact. Louisiana importers had 21 % of the impact. Mississippi and Alabama seafood economy had minimal importer roles.

10.3.6.2 Income Impacts

Income impacts are a component of sales in an economy. The income impacts for the four states associated with the use of both domestic and imported product amounted to $1.3 billion. Louisiana ($574 million) leads the Gulf and Mississippi was lowest in income generated at $113 million. Texas at $474 million was near the top and Alabama ranked third at $148 million. Each of the states experienced a reduction of income impacts from 2007 to 2009 with no change in rankings. Specifically, income impacts for the four states in 2007 were as follows: Louisiana, $1.1 billion; Mississippi, $184 million; Texas, $959 million; and Alabama, $268 million.Footnote 2

10.3.6.3 Employment Impacts

Direct jobs in the commercial harvesting sector spur actions among companies supplying inputs and for those adding value to landings and imported product ultimately used by consumers. The four states Gulf economy averaged 92,000 seafood industry jobs during 2007–2009. Employment decreased each year from 109,000 in 2007 to the period low of 63,000 in 2009. Texas job contraction was largest at −56 % followed by −38 % in Louisiana. Alabama and Mississippi had the lower decreases with each approximately −20 %. Seafood industry jobs in 2009 were (1) Louisiana, 29,200; (2) Texas, 18,900; (3) Alabama, 8,800; and (4) Mississippi, 6,400.Footnote 3 Jobs in the retail sector comprised approximately half of the jobs over the period. As to be expected, when employment decreased the retail sector experienced the largest problems. The nation’s economy began a period of slowdown that could have led to the result. However, the input/output model result of a Gulf retail sector experiencing a 60 % reduction between 2007 and 2009 is problematic in spite of Gulf landings falling 10 %.

In addition to these employment estimates from the U.S. Department of Commerce, NOAA’s annual publication Fisheries Economics of the United States and NOAA’s report Fisheries of the United States (FUS) include employment estimates. The later report lists employment from seafood wholesale and processing plants by state and region. With the exception of the input/output model indicating lower employment for Mississippi than the FUS report, the employment estimates are close between the reports. This closeness warrants caution because an input/output model accounts for direct employment and jobs arising from the induced effects of direct employment. So the employment estimate from the model should be higher than the direct employment in FUS.

10.3.6.4 Value Added

The value-added measure from an input/output model addresses a net concept to an industry’s economic impact. Gross sales reflect that costs are associated to produce the product sold. When the transfer payments of costs for goods and services used to produce the product sold are subtracted from gross sales, a net value image emerges. Referred to as value added, the estimate yields a descriptor useful for measuring a firm’s or sector’s net contribution to an economy. This section continues with the Alabama, Mississippi, Louisiana, and Texas designation for the Gulf because the input/output model does not report for the Florida west coast separately. The landed value and import value of the four-state Gulf in 2009 resulted in a value added of $1.4 billion. Louisiana’s post dockside firms accounted for 47 % of the total. Texas was second at a 31 % contribution to the total. Alabama at 13 % and Mississippi at 9 % had the smaller roles. There was no means by which to measure change between 2007 and 2009 because 2009 marked the first year of estimation.

10.3.6.5 Imports and Sales, Income, Employment, and Value Added Impacts

Use of imported seafood in Gulf post dockside economic endeavors can be significant to a firm’s success. The Fisheries Economics of the United States report for 2009 includes a treatment of imports as supply that leads to economic impacts. The four economic impact measures indicate double-digit contributions by imported product: (1) 33 % of sales, (2) 21 % of income, (3) 13 % of jobs, and (4) 25 % of value added (Figure 10.10). Among states Texas’ sales were 98 % higher than would have been experienced with state landings alone. Mississippi incorporated imports the least at 6 % of sales. Louisiana and Alabama used imports to gain 34 % and 16 % higher seafood industry sales, respectively.

10.3.7 Commercial Fisheries of State Managed Species

10.3.7.1 The Blue Crab Fishery

Essentially all of the nation’s catch of blue crab occur in state waters. Harvesting units are small and make daily trips. These characteristics apply throughout the Chesapeake Bay, South Atlantic, and Gulf assuring that landings by state mimic catch by state. Management of the elements contributory to population levels and harvests consequently fall to state agencies. Regional cooperation via GSMFC adds another level of contribution to states achieving their goals. Gulf landings fell 14 % from the 1990–1992 base period to the end period of 2007–2009. However, the region’s share of national landings increased in the comparison periods because national landings with Gulf removed fell by 32 %. Nationally, the increasing ex-vessel price for blue crab pushed dockside value up 90 %. The non-Gulf component increased over 100 %, while the Gulf increase neared only 59 %.

Within the downward landings results for the 1990–1992 period versus the 2007–2009 period, there was divergence among states. Texas (−57 %), Florida west coast (−40 %), and Alabama (−38 %) all experienced significantly lower landings (Figure 10.11). The Gulf’s largest producer, Louisiana, by comparison experienced only a 2 % decline in production while the region’s smallest producer, Mississippi, experienced an increase in production (Figure 10.11). Given that the Gulf blue crab production is dominated by Louisiana, the reduction in Gulf blue crab landings between 1990–1992 and 2007–2009 was minimal and largely mimicked that observed for Louisiana. These were among the lower producing states in the Gulf, but the impact with the largest producer, Louisiana, up only 2 % resulted in a decrease for the Gulf in total. Lowest producer, Mississippi, had a large percentage increase, but production approached only 500,000 lb. An important aspect of the Gulf blue crab fishery relates to the value of landings. Previously cited was the ex-vessel price performance being the best of species comprising Gulf landings. With 1982 serving as the base year for NOAA Fisheries’ ex-vessel price index, the blue crab index reached 383 in 2009. In 1990, the index stood at 152 suggesting that most of the large price increase occurred from 1990 to 2009. The end period had U.S. average ex-vessel price in a small range of $0.75–$0.81 per pound with the low occurring in 2009. Gulf end-period average prices were similar at $0.73–$0.80 per pound. The national recession in 2009 must have played a role as most Gulf species attained period low levels. Exceptions were oysters and stone crab claws.

Gulf of Mexico commercial blue crab landings by state for selected periods (NMFS FSD; data accessed 2012—see Appendix A) (Note: 1 lb = 0.454 kg)

Seasonality was less of an issue with blue crab production than other species. Closed seasons were not a management approach in major producing areas. Louisiana’s fishery accounts for 83 % of Gulf landings. Therefore, the occasional crab trap free periods based in avoiding gear conflicts or the facilitation of abandoned trap removal do not result in production shifts. May–September landings account for 53 % of annual landings (Figure 10.12). Winter months are lowest. Crabbers still put 4.3 million pounds on docks in the lowest month, March.

Gulf of Mexico commercial blue crab landings by month, 2007–2009 average (NMFS FSD; data accessed 2012—see Appendix A) (Note: 1 lb = 0.454 kg)

Blue crab can be graded by size with larger crabs going to live resale. Those not reaching the live resale size limit, the majority, are processed to remove the meat. However, the meat is not a uniform product; processed product is differentiated for sale as crab fingers, claw meat, white, backfin, lump, and jumbo lump. Multiple products of varied value for the human market represent perhaps the most complex of the Gulf’s processing industries. Blue crab processing occurred in all five Gulf states until 2005 which marked the stoppage in Mississippi from 2006 to the end of period used herein, 2009 (personal communication, Melissa Yencho-NOAA Fisheries). Texas processing was at the level with such a small number of firms that reporting it separately would divulge confidential data. From 2006 forward, the Texas data had to be combined with the Louisiana data to maintain confidentiality. Gulf blue crab processing data exists for Alabama, Louisiana/Texas, and Florida west coast. The 2007–2009 average Alabama processed production was six times larger than the next largest, Louisiana/Texas. Recalling the level of landings in Alabama being a 3-year average of approximately ten million pounds, points to significant cross state movement of live blue crab. The 4 % of average Gulf landings clearly would not support the Alabama processing industry’s 4.2 million pounds of blue crab meat. It is an inescapable conclusion that Louisiana was the only state that could have supplied sufficient live crabs for Alabama to attain such a high processed volume.

10.3.7.2 The Menhaden Fishery

Menhaden are a small oily finfish caught in nearshore fisheries from Chesapeake Bay to the Gulf. The vast majority of landings come from catch in the 0–3 mi (0–4.8 km) coastal area. Occasionally substantial catch is from the 3–200 mi (4.8–322 km) offshore area. The prospect of offshore harvest necessitates a closer tie between state agencies and NOAA Fisheries than would be thought for a clearly nearshore focused species. The decreasing number of firms in what is a large fishery for a species used in domestic and international markets encourages close cooperation among agencies and firms. Menhaden processing results in three products: (1) fish meal for use in animal feeds, primarily poultry; (2) fish oil for mostly export markets inclusive of human food uses; and (3) soluble, which often can be an additive to the meal.

The menhaden industry is noted as vertically integrated. Processors own vessels that fish under corporate direction. Crews are compensated on the basis of shares. Reported ex-vessel price under a vertically integrated structure with a small number of firms can be expected to differ from other Gulf fisheries. The other fisheries are characterized by large numbers of harvesters operating as owner operators throughout the Gulf at all times of a year. The companies and NOAA Fisheries do generate a price so that dockside value can be reported. The index of ex-vessel price for menhaden in 1990 and 2009 was at 128 and 154, respectively. At the end of the analysis period menhaden prices were $0.06–$0.07 per pound.

Gulf landings were two-thirds of the U.S. total. On only four occasions from 1990 to 2009 did Gulf landings not reach at least one billion pounds and on only two occasions did landings exceed 1.5 billion pounds (Figure 10.13). Based on the first and last 3-year averages for the period, landings exhibited stability. Landings over the period fell only slightly with value increasing by 15 %. The number of firms over time decreased; evidently making for an increase in average landings per firm. The industrial firms are located in Mississippi and Louisiana. Much smaller firms in Florida (west coast) and Alabama focus on menhaden as bait for other fisheries such as blue crab and some recreational uses. These states land less than 1 % of the Gulf production. Landings for the industrial fishery start minimally in April, steadily increase to a peak in July, and end by October (Figure 10.14). Firms in Mississippi and Louisiana essentially fish the same times of the year.

Gulf of Mexico annual menhaden landings, 1990–2009 (NMFS FSD; data accessed 2012—see Appendix A) (Note: 1 lb = 0.454 kg)

Gulf of Mexico menhaden landings by month, 2007–2009 average (NMFS FSD; data accessed 2012—see Appendix A) (Note: 1 lb = 0.454 kg)

10.3.7.3 Other State-Managed Species

The species selected as key species by the authors provide the insight needed regarding general conditions in the Gulf. Menhaden, brown shrimp, white shrimp, oysters, and blue crab combined accounted for 94 % of landings in the 2007–2009 period. NOAA Fisheries in its annual publication Fisheries Economics of the United States identifies Gulf key species additionally as crawfish, groupers, red snapper, mullets, stone crab, and tunas. The focus of this chapter being the northern Gulf (i.e., Alabama, Mississippi, and Louisiana) means there was no need to include crawfish and stone crab claws. The former is a freshwater species of wild and aquaculture origins found in Louisiana. The latter is overwhelmingly a Florida fishery. Like stone crab, the vast majority of Gulf striped mullet (Mugil cephalus) catch is Florida based; representing over 70 % of the Gulf total. Alabama and Louisiana basically account for the remainder with Alabama the larger. Total Gulf landings averaged ten million pounds of striped mullets in the most recent period. This was down from the initial 1990–1992 period average of 26 million pounds. Dockside value fell from the initial period’s level of $26.4 million to $5.7 million.

Yellowfin tuna (Thunnus albacares) landings in the Gulf for 2007–2009 increased to 35 % of the United States. The increase did not result from increased landings compared to elsewhere in the country. Rather, Gulf landings decreased (69 %) but landings other than the Gulf fell 78 %. Prices were favorable during 1990–2009 by almost doubling nationally. Gulf yellowfin prices followed the increase by the lesser amount of 50 %. The distribution of Gulf landings was very narrow. Louisiana received 77 % of the catch in 2007–2009, which represents an increase from the 46 % share in 1990–1992.

The harvest of red snapper and grouper are subject to increasingly constraining catch regulations of the GMFMC and cooperating states. Management of commercial effort by seasonal, gear, area protections and quotas with share assignment has the near-term effect of constraining catch. Additionally, these key species have been highly prized by anglers throughout the Gulf. Commercial red snapper average landings were essentially unchanged on the basis of an initial-period versus end-period measure at 2.6 million pounds. The 1995–2006 period average was 4.5 million pounds.

Location of landings changed among the states between initial and end periods. Northern Gulf states of Alabama, Louisiana, and Mississippi experienced a 50 % decrease. Texas and Florida west coast benefitted with the 1990–1992 average of 1.2 million pounds, increasing to 1.9 million pounds by 2007–2009. Gag (Mycteroperca microlepis), red (Epinephelus morio), and warsaw grouper (Epinephelus nigritus) landings have consistently been attributable to Florida west coast ports. Thus, there are landings of some groupers in the northern Gulf, but these cannot be considered important compared to previously reviewed species.

10.3.8 Additional Detail on Key Commercial Species

An overview of the Gulf of Mexico commercial seafood industry, including a brief discussion of some of the key species, was provided in the previous section of this chapter. This section provides additional detail on some of these key species including shrimp, oysters, and reef fish. Shrimp is given more discussion because it is by far the largest contributor, by value, to the Gulf of Mexico seafood industry. Oysters are given additional treatment because the nature of the industry involves leasing activities, with emphasis being given to Louisiana. Reef fish species comprise a sizeable portion of commercial finfish landings and are the subject of considerable management, including recently enacted catch share programs, and are given additional consideration on this basis.

10.3.8.1 The Shrimp Fishery

10.3.8.1.1 Gulf Shrimp Landings and the Relation to Imports

With a 2009 dockside value of $314 million, the shrimp fishery is the largest contributor to the $615 million (2009) Gulf of Mexico commercial fishing sector. Since it is by far the largest component of the Gulf of Mexico commercial seafood industry, it is covered in additional detail in this section.

Annual Gulf shrimp production (heads-on weight) during 1990–2009 is provided in Figure 10.15 (left panel). While exhibiting a significant amount of annual variation, the yearly changes tend to follow a random-walk process and, over time, production returns to its long-run average (while not shown in the graph, long-run production of gulf shrimp has been stable since at least the 1970s). These observed random walks are primarily the result of changes in environmental conditions that influence recruitment and growth. Since the primary species of shrimp landed in the Gulf—brown and white—are short-lived animals, with maximum age of about 1 year, any short-run deviations from the long-term average will be temporary in nature assuming environmental conditions return to normal and there is a sufficient amount of effort to harvest the available crop. Overall, annual harvest of Gulf shrimp during 1990–2009 averaged 236 million pounds with a range from 181 million pounds in 2008 to 290 million pounds in 2006. While the effort needed to harvest the aggregate shrimp crop has historically been sufficient, as addressed in subsequent sections of this chapter, changes in profitability have led to a significant decline in industry effort in recent years and an increasing concern that with further declines in effort, a portion of the annual shrimp crop may not be harvested.

Gulf of Mexico shrimp landings (left panel) and value (right panel), 1990–2009 (NMFS FSD, data accessed 2012, with deflated values calculated by authors–see Appendix A) (Note: 1 lb = 0.454 kg)

While the long-run production of Gulf shrimp, in pounds, has remained stable over time, the same cannot be said about the value of landed product; especially when the influence of inflation is removed. As indicated in Figure 10.15 (right panel), the long-run dockside value of the Gulf shrimp harvest has, overall, been declining, whether considered on a current or deflated basis. This decline has been particularly pronounced since 2001. On a current dollar basis, the value of Gulf production fell from an average of just over $400 million annually during 1990–1994 to about $350 million annually during 2005–2009. After adjusting for inflation, the decline was approximately 40 %, from $617 million to $367 million (expressed in 2009 dollars).

While there are several reasons for the sharp decline in the Gulf dockside shrimp price beginning in 2001, the overriding one is that of increasing imports. The source of these imports is from more than 40 countries throughout the world with Asian countries dominating the field. As indicated by the information in Figure 10.16, import growth has been large during the considered timeframe with total imports (heads-on equivalent weightFootnote 4) advancing from an average of 850 million pounds annually during 1990–1994 to 2.3 billion pounds annually during the 2005–2009 period. Furthermore, as indicated, much of this increase has occurred post 2000. Given the strong U.S. economy throughout the later portion of the 1990s and the concomitant increase in demand for shrimp, the increase in imports during the 1990s did not lead to any sharp decline in the Gulf of Mexico dockside value (or price). However, the large increase in imports post 2000 combined with a number of other factors, including a recession that officially began in the third quarter of 2001, resulted in a sharp and prolonged decrease in the Gulf of Mexico dockside value (via a change in price). A detailed examination of possible factors influencing this price decline can be found in Keithly and Poudel (2008).

U.S. shrimp imports (whole weight), 1990–2009 (NMFS FSD, data accessed 2012, with weight conversions calculated by authors–see Appendix A) (Note: 1 lb = 0.454 kg)

Comparison of the information in Figure 10.15 (left panel) and Figure 10.16 clearly highlights how small Gulf landings are relative to imports. Given this and the fact that differentiation of Gulf shrimp from the imported product is minimal, one would expect changes in the Gulf and import prices to follow a similar pattern. This relationship is evident in the information in Figure 10.17. While the import price, expressed on a whole weight equivalent basis, generally exceeded the Gulf dockside price by a considerable margin during the early 1990s, this margin gradually lessened over time and had largely disappeared by the mid-2000s.Footnote 5 Furthermore, given the large share of total U.S. supply (i.e., domestic and imported product) provided by imports, along with their apparent close substitutability, one would expect that changes in Gulf landings would have little or no influence on its own price. This is examined in greater detail in a subsequent section.

Deflated Gulf dockside shrimp price and import price (whole weight), 1990–2009 (NMFS FSD, data accessed 2012, with weight conversions and deflated prices calculated by authors—see Appendix A) (Note: 1 lb = 0.454 kg)

10.3.8.1.2 A Closer Look at Imports

As noted, a large number of countries export shrimp to the United States. Asian countries have accounted for the majority of U.S. shrimp imports since at least the early 1990s and in 2009 accounted for more than 70 % of the total (based on product weight). Thailand dominated exports to the United States in 2009 accounting for almost one-half of the Asian exports and more than one-third of total exports. Other countries of significance include Indonesia (17 % of Asian exports and 13 % of total exports to the United States), Ecuador (70 % of South American exports and 11 % of total exports to the United States), China and Vietnam (each accounting for approximately 10 % of Asian exports to the United States and 8 % of total exports to the United States), and Mexico (accounting for about 67 % of Central American exports to the United States and 7.5 % of total exports to the United States).

Employing monthly data covering the 1995–2005 period, Jones et al. (2008) examines the U.S. demand for shrimp by source in relation to prices from the sources. The analysis includes seven import sources—Mexico, Ecuador, India, Thailand, Vietnam, China, and Rest of World—and domestic (i.e., U.S.) source. Own-price elasticities for all sources were negative, as suggested by theory, and statistically significant.Footnote 6 Furthermore, the own-price elasticities were inelastic (less than −1) for all sources implying that a 1 % increase (decrease) in price from any given source would result in a less than proportionate decrease (increase) in quantity demanded for shrimp from that source in the U.S. market. The scale elasticities, which measure the influence of a change in overall U.S. shrimp demand on the demand from the individual sources, were positive and statistically significant for all sources and ranged from a low of 0.30 (Ecuador) to a high of 1.74 (India). The scale elasticity for the U.S. production with an estimate of 0.90 indicates that the demand for U.S. produced shrimp increases by 9 % for each 10 % increase in total U.S. shrimp demand. Finally, the researchers note that “[f]or the most part, cross elasticities were negative, implying that shrimp demand exhibited a complementary relationship between countries.” This finding is not easily explainable.

The large increase in U.S. shrimp imports and the resultant decline in Gulf dockside price resulted in a coalition of Southeast U.S. shrimp harvesters and processors (Gulf and South Atlantic) petitioning the U.S. International Trade Administration and the U.S. International Trade Commission for relief in the form of antidumping duties. These petitions, filed on December 31, 2003, charged six countries—China, Thailand, Vietnam, India, Ecuador, and Brazil—with unfair trade practices. These six countries exported 822 million pounds of shrimp (product weight) to the United States in 2003, which represented almost three-quarters of the total U.S. shrimp imports for that year. After an exhaustive investigation, the finding of dumping and injury was found, and duties were imposed on subject merchandise from these six countries. Details on the investigation and factors leading to the investigation are provided by Keithly and Poudel (2008) who, after analysis of the situation, conclude that these duties had only a marginal impact on limiting shrimp exports to the United States because of trade diversion effects (essentially increased shrimp imports from countries not named or merchandise not named that offset any reduction in imports from countries and merchandise named). Thus, the duties likely had only a marginal, if any, effect on increasing the price received by the domestic shrimpers for their harvested product. Furthermore, the conclusion by Keithly and Poudel (2008) would suggest that the recent stability in imports was not the result of the duties imposed on named countries and merchandise. Instead, the stability likely reflects a decline in demand in 2008 as the United States entered a deep and protracted recession. While the antidumping duties imposed on the six named countries may have had little influence on increasing the U.S. Gulf shrimp dockside price, the domestic industry did benefit significantly via funds collected from the duties and negotiated settlements to rescind reviews. Specifically, the Continued Dumping and Subsidy Offset Act of 2000 (i.e., the Byrd Amendment) provided for the annual disbursement of funds collected under the Act to the injured party (i.e., the petitioners). This disbursement totaled hundreds of millions of dollars before the Act was repealed.

As noted, Southeast U.S. processors also petitioned for relief from the growing import base. This reflected the fact that not only was the total import base increasing but the composition of the import base was also changing with value-added products comprising an increasing share of the total (Figure 10.18). Imports of peeled raw product, for example, increased from about 300 million pounds (whole weight basis) in 1990 to more than 800 million pounds in the late 2000s. Peeled cooked imports increased from about 60 million pounds (whole weight equivalent) to more than 800 million pounds. Imports of headless shell-on shrimp, by comparison, exhibited a much more modest increase—from about 325 million pounds (whole weight basis) in 1990 to 500–550 million pounds by the late 2000s.

U.S. shrimp imports by product form (whole weight equivalent basis), 1990–2009 (NMFS FSD, data accessed 2012, with weight conversions calculated by authors—see Appendix A) (Note: 1 lb = 0.454 kg)

10.3.8.1.3 A Closer Look at the Gulf Shrimp Fishery

Gulf shrimp fishermen target four species of shrimp, including brown (Farfantepenaeus aztecus), white (Litopenaeus setiferus), pink (Farfantepenaeus duorarum), and royal red (Pleoticus robustus or Hymenopenaeus robustus). Other species of related organisms, such as seabobs (Xiphopenaeus kroyeri) and rock shrimp (Sicyonia brevirostris), are incidentally harvested. Of the main shrimp species, brown shrimp is the most important to offshore harvesters and is primarily caught in waters up to 40 fathoms (73.2 m) from June through October of each year. The white shrimp fishery, which approaches the importance of brown shrimp in terms of catch, typically peaks in the months of August through December. Geographically, however, white shrimp are primarily harvested from nearshore, state waters up to 20 fathoms (36.6 m), thus generally making them the target of smaller vessels. Of the remaining shrimp species, pink shrimp are primarily harvested as a distinct species off of Florida’s west coast and in the Florida Keys in waters up to 30 fathoms (54.9 m). Outside Florida waters, pink shrimp are less abundant; if harvested, they tend to be caught while harvesting brown shrimp and are typically included as part of the brown shrimp harvest. Royal red shrimp, a species harvested in waters 140–275 fathoms (256–503 m) deep, are a minor component of the Gulf shrimp fishery. Unlike other shrimp species, which are relatively short-lived and thus considered to be an annual crop, royal reds have a multiple-year life span. While brown, white, and pink shrimp are all subject to capture in state and EEZ waters (depending on the time of year), royal reds are harvested exclusively in the EEZ.

Technologically, the Gulf shrimp fleet employs a wide range of both gear and vessels depending on the species and fishing area being exploited. In terms of gear, harvesters have been known to use cast nets, haul seines, stationary butterfly nets, wing nets, skimmer nets, traps, beam trawls, and otter trawls, with the otter trawl being the primary gear used in offshore and EEZ waters.

10.3.8.1.3.1 Shrimp Effort

Given the large decline in the Gulf of Mexico dockside shrimp price in conjunction with rising fuel prices, shrimp fishermen have been experiencing a cost-price squeeze for some time now. This squeeze was exacerbated in late 2001 when the dockside price fell sharply and this decline lasted for a protracted period of time (see Keithly and Poudel 2008 for additional details). Given this cost-price squeeze, it should come as no surprise that effort in the fishery has fallen. The decline in offshore effort (defined as outside the Collision Regulation [COLREG] lines), measured in terms of 24-h days fished, is given in Figure 10.19 for the 1990–2009 period. As indicated, total offshore effort approached or exceeded 200,000 days fished per year throughout the 1990s. Since 2003, however, effort has fallen sharply and in recent years, has been less than 70,000 days per year. Overall, effort in recent years has only been about one-third to one-half of the observed effort throughout the 1990s. Analysis by Nance et al. (2006) examines the relationship between catch and effort in the offshore component of the Gulf of Mexico shrimp fishery and if their analysis is valid, one can conclude that the current level of effort associated with the offshore component of the fishery is significantly less than what is required to harvest maximum yield. This conclusion, however, needs to be tempered because the treated relationship between offshore yield and effort in their analysis was considered independently of inshore shrimping activities. As the case with respect to offshore effort, inshore effort has also fallen sharply in recent years. Reduction in effort in the inshore component of the fishery would, one might hypothesize, result in increased escapement of the small shrimp to offshore waters and, hence, an increasing abundance of shrimp in the offshore waters. This increased abundance translates into a higher catch per unit of effort in the offshore waters.

Estimated offshore effort (24-h days fished) by the Gulf of Mexico offshore shrimp fleet, 1990–2009 (NMFS Galveston Laboratory, personal communication, 2012--see Appendix A)

A more detailed examination of effort in the two main northern Gulf of Mexico shrimp fisheries—the brown shrimp fishery and the white shrimp fishery—can be made with the aid of Figure 10.20. As indicated, total estimated effort (i.e., inshore and offshore) in the brown shrimp fishery (Grids 7–21)Footnote 7 fell from almost 200,000 days annually in the early 1990s to about 160,000 days by the late 1990s/early 2000s (effort is assumed to be directed at a particular species if at least 90 % of that trip’s catch comprises that particular species). Thereafter, in association with the sharp decline in shrimp price and increasing fuel costs, effort fell precipitously to less than 50,000 days in recent years.

Directed shrimping effort on brown (left panel) and white shrimp (right panel) fisheries (grids 7–21), 1990–2009 (NMFS Galveston Laboratory, personal communication, 2012–see Appendix A)

A somewhat different picture emerges when one examines total effort (i.e., inshore and offshore) white shrimp effort (Figure 10.20, right panel). As indicated, effort associated with this fishery showed a large increase in the mid-1990s to early 2000s with an abnormally high number of days fished being reported in 2002 (169,000 days). Thereafter, however, effort fell sharply to about 60,000 days in recent years. This decline in effort coincided with a period of increasing white shrimp harvest indicating a significant increase in the catch per unit effort.

As noted by Liese and Travis (2010), vessels fishing for Penaeid shrimp in the federal waters of the Gulf of Mexico were required to have a permit as of December 5, 2002. Subsequently, a moratorium was placed on the issuance of new permits and, according to unpublished NMFS records, a total of 1,907 vessels were permitted under the Gulf shrimp moratorium permit in 2009 (i.e., the upper-bound estimate of the number of vessels that would be legally allowed to shrimp in the federal waters of the Gulf of Mexico). Of this total, 693 of the vessels, or more than one-third of the total, were home-ported in Texas. Louisiana ranked second (545 permits; 29 %), followed by Florida (278 permits; 15 %), Mississippi (164 permits), and Alabama (149 permits). While the number of permits equaled about 1,900 in 2009, Liese and Travis (2010) report that only about 1,215 of these actively harvested shrimp in 2009.

In addition to those vessels holding a Gulf shrimp moratorium permit, which is required for shrimping in federal waters, a large number of boats shrimp only in the state waters. Based on state license sales, Miller and Isaacs (2011) estimate that the population of inshore shrimpers, excluding those that had a Gulf shrimp moratorium permit, approximated 3,765 in 2009. About 60 % of the licenses were issued in Louisiana while another 14 % and 12 % were issued in the states of Texas and Alabama, respectively.

10.3.8.1.3.2 Shrimp Size at Harvest

The size of shrimp at harvest varies significantly throughout the year and can vary over time as a result of environmental factors, dates associated with opening inshore waters, the amount of fishing pressure, where the fishing pressure is centered, or some amalgam. Cold weather, for example, can retard the growth of brown shrimp, which may yield a smaller size at harvest, all other factors being equal. Similarly, declining fishing pressure may provide the shrimp additional time to grow which would yield a larger average size at harvest (assuming all other factors are the same). The estimated average size of shrimp for four time periods—1990–1994, 1995–1999, 2000–2004, and 2005–2009—by month is given in Figure 10.21. As indicated, shrimp size is consistently smallest in May (i.e., a larger number of shrimp to the pound), associated with movement of brown shrimp from the estuaries and the opening of the inshore fishery in the northern Gulf States. The average size then increases (as the brown shrimp grows and moves offshore) until September/October when white shrimp show up in significant quantities.

Estimated average size of shrimp at harvest (headless), by month, selected 5-year periods (NMFS Galveston Laboratory, personal communication, 2012, with calculations by authors–see Appendix A) (Note: 1 lb = 0.454 kg)

The apparent increase in average shrimp size (i.e., fewer shrimp to the pound), particularly after the 1995–1999 period is of interest as well. For example, the estimated average number of shrimp to the pound (headless) in May during 1990–1994 was estimated to equal 102 and increased to 113 during 1995–1999. During the May 2000–2004 period, the average declined to 98 and declined again to 85 during the 2005–2009 period. For September (roughly when white shrimp begin to move), the averages for the four 5-year periods are 55, 53, 50, and 40, respectively. The increasing shrimp size (i.e., fewer shrimp to the pound) has been particularly pronounced during the most recent 5-year period when the monthly trend held for all months but February. While not formally tested, one plausible explanation for the changing shrimp size over the period of analysis is the large reduction in effort during recent years (Figs. 10.19 and 10.20).

Size of shrimp at harvest is an important consideration for at least two reasons. First, the price the shrimper receives for his harvested product is directly related to the harvested size with smaller shrimp commanding a lower price. Second, an increase in the average shrimp size at harvest (i.e., fewer shrimp to the pound) can translate into increased harvest in the aggregate assuming natural mortality is low relative to the gains in weight that could be achieved by allowing the shrimp to grow to a larger size prior to harvest. The relationship between size of shrimp and price received on an annual basis for the 2000–2009 period is given in Figure 10.22. As is illustrated by the information in the figure, prices (undeflated) of all shrimp sizes fell during the 2000–2009 period. Furthermore, the price declines are particularly pronounced (in terms of the absolute dollar decline) for the larger-sized shrimp (i.e., smaller count to the pound). With respect to the under 15 count (i.e., less than 15 shrimp to the pound), the unadjusted price fell from about $9.00 per pound to $4.00 per pound, or by about $5.00 per pound. The 51–67 count size price, by comparison, fell by only $1.75 per pound from $3.44 in 2000 to $1.69 in 2009. In all size categories, overall, the price decline between 2000 and 2009 ranged from about 45 to 55 %.

Average annual shrimp prices per pound (current) by size category (NMFS Galveston Laboratory, personal communication, 2012–see Appendix A) (Note: 1 lb = 0.454 kg)

With a change in average size of shrimp harvested throughout the year comes a change in price. This is illustrated in Figure 10.23 for selected years. As indicated, price is consistently lowest in May when the average size of shrimp is smallest (see Figure 10.21) and inland waters are opened. As the brown shrimp grow and move offshore, the average price tends to increase through August. Associated with the opening of the inshore waters to white shrimp in late August, the price of shrimp begins to decline. The relatively high prices in months prior to the opening of the inshore waters to brown shrimp fishing in May (i.e., January through April) to a large extent represent the harvest of large, overwintering white shrimp.

Gulf dockside price by month for selected years (prices deflated based on 1982–1984 Consumer Price Index [CPI]) (NMFS Galveston Laboratory, personal communication, 2012, with price calculations by authors--see Appendix A) (Note: 1 lb = 0.454 kg)

The information in Figure 10.23 also points to some other price features meriting discussion. First, note that the sharp differential between the 2001 monthly prices and the 1990 monthly prices beginning in September and continuing throughout the remainder of the year. This sudden and sharp price differential reflects the terrorist attack of September 11, 2001 and subsequent recession. Second, the 2009 monthly prices are well below either the 1990 or 2001 deflated prices. Finally, as indicated, there is considerably less price variation by month in the 2009 prices than in either the 1990 or 2001 prices; consistent with a narrowing of the price differential between the large and small shrimp as observed in Figure 10.22.

10.3.8.1.3.3 Harvested Species

Two species, brown shrimp and white shrimp, as noted, dominate the commercial harvest of shrimp. This is particularly true in the northern and western Gulf. Both of these species tend to be seasonal in nature, and harvest is directly related to their growth and migration patterns. The seasonal nature of harvest of brown shrimp, based on the 2005–2009 period, is illustrated in Figure 10.24. Harvest tends to be small until May, which coincides with emigration of the brown shrimp from the estuaries to deeper waters and the opening of the inshore waters in the northern Gulf States. On average, 9.3 million pounds of brown shrimp were harvested in the month of May during 2005–2009, and this increased to 14 million pounds in June. Coinciding with the opening of Texas waters to shrimping, brown shrimp catch, in pounds, increased once again in August and then fell through the remainder of the year.Footnote 8

Gulf of Mexico brown shrimp harvest by month, 2005–2009 average (NMFS Galveston Laboratory, personal communication, 2012, with calculations by authors--see Appendix A) (Note: 1 lb = 0.454 kg)

Production (pounds) of brown shrimp by month for selected time periods during 1990–2009, expressed on a percentage basis, is given in Figure 10.25 (left panel). In general, the monthly production pattern is relatively consistent across the four 5-year time periods considered. One significant difference, however, is observed in the most recent 5-year period (2005–2009).

Gulf of Mexico brown shrimp harvest by month (pounds, left panel; value, right panel) expressed on a percentage basis for selected time periods, 1990–2009 (NMFS, Galveston Laboratory with calculations by authors; data 2012—see Appendix A)

In this period, the harvest of brown shrimp appears, to some extent, to be delayed. For example, May harvest, expressed on a percentage basis, was significantly lower than in other 5-year periods while harvests in the later months (August through October) were higher than in other periods. This delayed harvest may reflect the declining effort on the stock (Figure 10.20, left panel), which provides the brown shrimp stock additional time to grow.

While May and June tend to be the peak months in terms of poundage of brown shrimp harvest, peak value from the harvest tends to be in July and August (Figure 10.25, right panel). The observed difference in monthly poundage and value patterns is the result of larger brown shrimp being harvested in the later months and the increased price per pound for the harvested product. This price pattern is presented in Figure 10.26 for the 2005–2009 period. As indicated, the May brown shrimp price during 2005–2009 averaged less than $1.50 per pound. Coinciding with an increased size at harvest, the brown shrimp price increased rapidly reaching $3.00 per pound by the end of the year.

Gulf of Mexico brown shrimp price by month, 2005–2009 average (NMFS Galveston Laboratory, personal communication, 2012, with calculations by authors–see Appendix A) (Note: 1 lb = 0.454 kg)

The U.S. Gulf of Mexico white shrimp harvest has, overall, been increasing during the 1990–2009 period. For example, in 1990–1994, annual production of white shrimp averaged about 40 million pounds (heads off). By 1995–1999, the average had increased again to 42 million pounds and increased sharply to 58 million pounds in 2000–2004. Annual production of white shrimp in 2005–2009, averaging 66 million pounds, exceeded that of 1990–1994 by about 65 %.

While not as distinct as for brown shrimp, there is also a seasonal pattern to the Gulf white shrimp harvest. During 2005–2009, for example, Gulf landings of white shrimp averaged 66 million pounds (heads off). While brown shrimp catch is predominant in the 3-month period ending in August, the Gulf white shrimp catch tends to be highest in the months of August through November (Figure 10.27, left panel). This pattern is relatively consistent back to the 1990–1994 period, although the most recent 5-year period indicates a higher proportion being harvested in the May–July period at the expense of later months.

Gulf of Mexico average monthly white shrimp production for 2005–2009 (left panel) and production by month, expressed on a percentage basis, selected periods (right panel) (NMFS Galveston Laboratory, personal communication, 2012, with calculations by authors--see Appendix A) (Note: 1 lb = 0.454 kg)

The higher proportion of white shrimp catch in the earlier months (May through July) may well reflect the increased catch of overwintering white shrimp. Specifically, with significantly less white shrimp fishing effort in recent years, an increasing proportion of the shrimp stock produced in a given year escapes catch in that year and is available for harvest in the subsequent year. This hypothesis is, to some extent, supported by examination of monthly white shrimp dockside prices (Figure 10.28). Specifically, the monthly white shrimp dockside prices tend to be relatively high in the earlier months suggesting larger shrimp that escaped harvest in the previous year. While one might argue that this price effect may be the result of low quantities being harvested in these earlier months, this argument is likely fallacious for two reasons. First, there are large quantities of brown shrimp landed in the May–July period that represent a close substitute for the white shrimp product. Second, as discussed later in this chapter, large changes in Gulf landings appear to have little influence on the Gulf dockside price due, largely, to the large import base.

Gulf of Mexico average monthly dockside white shrimp price, 2005–2009 average (NMFS Galveston Laboratory, personal communication, 2012, with price calculations by authors--see Appendix A) (Note: 1 lb = 0.454 kg)

10.3.8.1.3.4 Harvest by Depth and Movement of the Fleet