Abstract

This chapter is devoted to exotic options, which include multifactor options and Asian options. Non-constant coefficients require numerical methods for more general PDEs than those discussed in Chap. 6 Upwind schemes, stability issues and total variation diminishing are discussed. The final part of the chapter is devoted to penalty methods, here applied to a two-asset option.

Access this chapter

Tax calculation will be finalised at checkout

Purchases are for personal use only

Notes

- 1.

Again, the name has no geographical relevance.

- 2.

The ordinary integral A t is random but has zero quadratic variation [340].

- 3.

After interpolation; MATLAB graphics; similar [385].

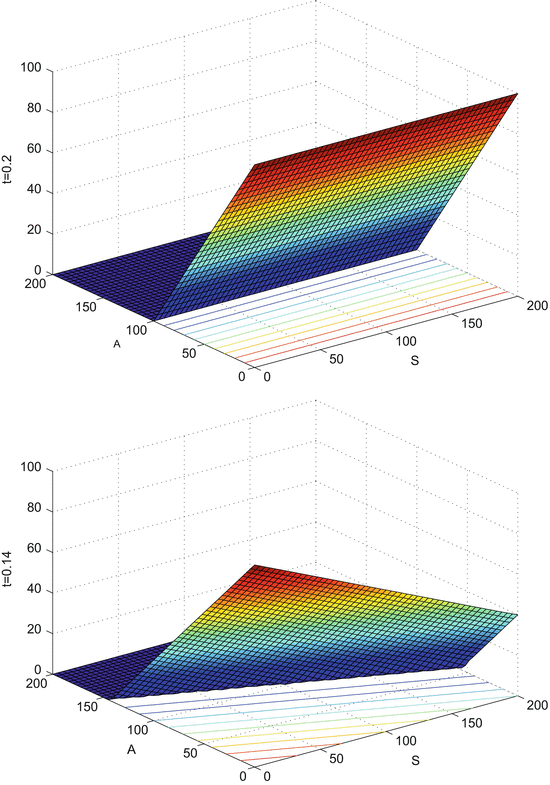

Fig. 6.3

Asian European fixed strike put, K = 100, T = 0. 2, r = 0. 05, σ = 0. 25. The top figure shows the payoff V (S, A, t) for t = T = 0. 2; the bottom figure shows the solution surface V (S, A, t) for t = 0. 14. For the solution surfaces t = 0. 06, and t = 0 see Fig. 6.4. With kind permission of Sebastian Göbel

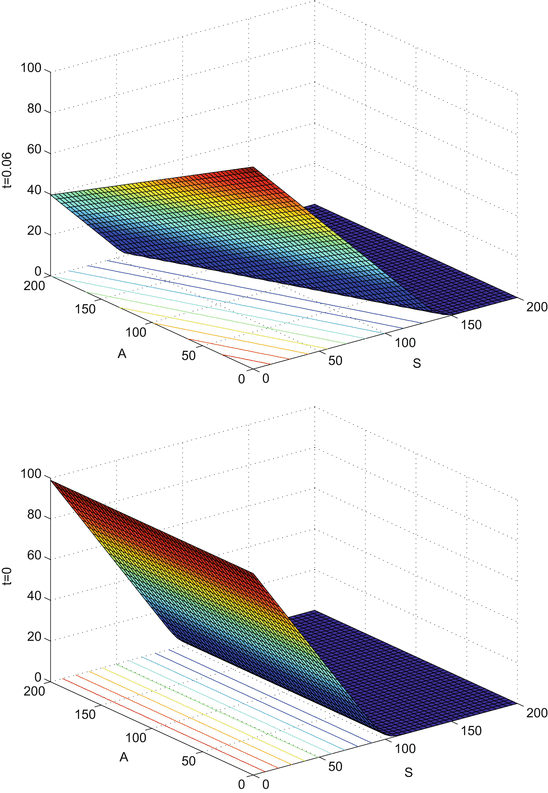

Fig. 6.4

Figure 6.3 continued, with solution surfaces V (S, A, t) for t = 0. 06 (top), and t = 0 (bottom)

- 4.

In case of a continuous dividend flow δ, replace r by r −δ.

- 5.

L stands for the wave length or the length of the interval. In case of a partition into n steps of size Δx, ηΔx = 2π∕n. Without loss of generality, we may set L = 2π, so η = 1 for the following analysis. It will be sufficient to study the propagation of eikx.

- 6.

In fact, the situation is more subtle. We postpone an outline of how dispersion is responsible for the oscillations to Sect. 6.5.2.

- 7.

Actually, the LCP (6.44) is nonlinear as well, which is not correctly reflected by the name “LCP”.

- 8.

For δ 1 > r or δ 2 > r the “other” quotient is upwind.

References

Abramowitz, M., Stegun, I.: Handbook of Mathematical Functions. With Formulas, Graphs, and Mathematical Tables. Dover, New York (1968)

Achdou, Y., Pironneau, O.: Computational Methods for Option Pricing. SIAM, Philadelphia (2005)

Adams, R.A.: Sobolev Spaces. Academic Press, New York (1975)

AitSahlia, F., Carr, P.: American options: a comparison of numerical methods. In: Rogers, L.C.G., Talay, D. (eds.) Numerical Methods in Finance, pp. 67–87. Cambridge University Press, Cambridge (1997)

Alfonsi, A.: On the discretization schemes for the CIR (and Besselsquared) processes. Monte Carlo Methods Appl. 11, 355–384 (2005)

Almendral, A., Oosterlee, C.W.: Numerical valuation of options with jumps in the underlying. Appl. Numer. Math. 53, 1–18 (2005)

Almendral, A., Oosterlee, C.W.: Highly accurate evaluation of European and American options under the Variance Gamma process. J. Comput. Finance 10(1), 21–42 (2006)

Andersen, L., Andreasen, J.: Jump diffusion process: volatility smile fitting and numerical methods for option pricing. Rev. Deriv. Res. 4, 231–262 (2000)

Andersen, L., Broadie, M.: Primal-dual simulation algorithm for pricing multidimensional American options. Manag. Sci. 50, 1222–1234 (2004)

Andersen, L.B.G., Brotherton-Ratcliffe, R.: The equity option volatility smile: an implicit finite-difference approach. J. Comput. Finance 1(2), 5–38 (1997/1998)

Ané, T., Geman, H.: Order flow, transaction clock, and normality of asset returns. J. Finance 55, 2259–2284 (2000)

Arnold, L.: Stochastic Differential Equations (Theory and Applications). Wiley, New York (1974)

Arouna, B.: Robbins-Monro algorithms and variance reduction in finance. J. Comput. Finance 7(2), 35–61 (2003)

Artzner, P., Delbaen, F., Eber, J.-M., Heath, D.: Coherent measures of risk. Math. Finance 9, 203–228 (1999)

Avellaneda, M.: Quantitative Modeling of Derivative Securities. From Theory to Practice. Chapman & Hall, Boca Raton (2000)

Avellaneda, M., Levy, A., Parás, A.: Pricing and hedging derivative securities in markets with uncertain volatilities. Appl. Math. Finance 2, 73–88 (1995)

Avellaneda, M., Parás, A.: Dynamic hedging portfolios for derivative securities in the presence of large transaction costs. Appl. Math. Finance 1, 165–194 (1994)

Avellaneda, M., Parás, A.: Managing the volatility risk of derivative securities: the Lagrangian volatility model. Appl. Math. Finance 3, 21–53 (1996)

Babuška, I., Strouboulis, T.: The Finite Element Method and Its Reliability. Oxford Science, Oxford (2001)

Ball, C.A., Roma, A.: Stochastic volatility option pricing. J. Financ. Quant. Anal. 29, 589–607 (1994)

Barles, G.: Convergence of numerical schemes for degenerate parabolic equations arising in finance theory. In: Rogers, L.C.G., Talay, D. (eds.) Numerical Methods in Finance, pp. 2–21. Cambridge University Press, Cambridge (1997)

Barles, G., Burdeau, J., Romano, M., Samsœn, N.: Critical stock prices near expiration. Math. Finance 5, 77–95 (1995)

Barles, G., Daher, Ch., Romano, M.: Convergence of numerical schemes for parabolic equations arising in finance theory. Math. Models Methods Appl. Sci. 5, 125–143 (1995)

Barles, G., Soner, H.M.: Option pricing with transaction costs and a nonlinear Black-Scholes equation. Finance Stochast. 2, 369–397 (1998)

Barndorff-Nielsen, O.E.: Processes of normal inverse Gaussian type. Finance Stochast. 2, 41–68 (1997)

Barone-Adesi, G., Whaley, R.E.: Efficient analytic approximation of American option values. J. Finance 42, 301–320 (1987)

Barone-Adesi, G., Whaley, R.E.: On the valuation of American put options on dividend-paying stocks. Adv. Futures Options Res. 3, 1–13 (1988)

Barraquand, J., Pudet, T.: Pricing of American path-dependent contingent claims. Math. Finance 6, 17–51 (1996)

Barrett, R., et al.: Templates for the Solution of Linear Systems: Building Blocks for Iterative Methods. SIAM, Philadelphia (1994)

Bates, D.: Jumps and stochastic volatility: the exchange rate processes implicit in Deutschmark options. Rev. Financ. Stud. 9, 69–107 (1996)

Baxter, M., Rennie, A.: Financial Calculus. An Introduction to Derivative Pricing. Cambridge University Press, Cambridge (1996)

Behrends, E.: Introduction to Markov Chains. Vieweg, Braunschweig (2000)

Bellman, R.: Dynamic Programming. Princeton University Press, Princeton (1957)

Ben Hamida, S., Cont, R.: Recovering volatility from option prices by evolutionary optimization. J. Comput. Finance 8(4), 43–76 (2005)

Bensoussan, A.: On the theory of option pricing. Acta Appl. Math. 2, 139–158 (1984)

Berridge, S.J., Schumacher, J.M.: Pricing high-dimensional American options using local consistency conditions. In: Appleby, J.A.D., et al. (eds.) Numerical Methods for Finance. Chapman & Hall, Boca Raton (2008)

Billingsley, P.: Probability and Measure. Wiley, New York (1979)

Bischi, G.I., Sushko, I. (eds.): Dynamic Modelling in Economics & Finance. Special Issue of Chaos, Solitons and Fractals 29(3) (2006)

Bischi, G.I., Valori, V.: Nonlinear effects in a discrete-time dynamic model of a stock market. Chaos Solitons Fractals 11, 2103–2121 (2000)

Björk, T.: Arbitrage Theory in Continuous Time. Oxford University Press, Oxford (1998)

Black, F., Scholes, M.: The pricing of options and corporate liabilities. J. Polit. Econ. 81, 637–659 (1973)

Blomeyer, E.C.: An analytic approximation for the American put price for options with dividends. J. Financ. Quant. Anal. 21, 229–233 (1986)

Bouchaud, J.-P., Potters, M.: Theory of Financial Risks. From Statistical Physics to Risk Management. Cambridge University Press, Cambridge (2000)

Bouleau, N.: Martingales et Marchés Financiers. Edition Odile Jacob, Paris (1998)

Box, G.E.P., Muller, M.E.: A note on the generation of random normal deviates. Ann. Math. Stat. 29, 610–611 (1958)

Boyle, P.P.: Options: a Monte Carlo approach. J. Financ. Econ. 4, 323–338 (1977)

Boyle, P., Broadie, M., Glasserman, P.: Monte Carlo methods for security pricing. J. Econ. Dyn. Control 21, 1267–1321 (1997)

Boyle, P.P., Evnine, J., Gibbs, S.: Numerical evaluation of multivariate contingent claims. Rev. Financ. Stud. 2, 241–250 (1989)

Brachet, M.-E., Taflin, E., Tcheou, J.M.: Scaling transformation and probability distributions for time series. Chaos Solitons Fractals 11, 2343–2348 (2000)

Brandimarte, P.: Numerical Methods in Finance and Economics. A MATLAB-Based Introduction. Wiley, Hoboken (2006)

Breen, R.: The accelerated binomial option pricing model. J. Financ. Quant. Anal. 26, 153–164 (1991)

Brennan, M.J., Schwartz, E.S.: The valuation of American put options. J. Finance 32, 449–462 (1977)

Brenner, S.C., Scott, L.R.: The Mathematical Theory of Finite Element Methods, 2nd edn. Springer, New York (2002)

Brent, R.P.: On the periods of generalized Fibonacci recurrences. Math. Comput. 63, 389–401 (1994)

Briani, M., La Chioma, C., Natalini, R.: Convergence of numerical schemes for viscosity solutions to integro-differential degenerate parabolic problems arising in financial theory. Numer. Math. 98, 607–646 (2004)

Broadie, M., Detemple, J.: American option valuation: new bounds, approximations, and a comparison of existing methods. Rev. Financ. Stud. 9, 1211–1250 (1996)

Broadie, M., Detemple, J.: Recent advances in numerical methods for pricing derivative securities. In: Rogers, L.C.G., Talay, D. (eds.) Numerical Methods in Finance, pp. 43–66. Cambridge University Press, Cambridge (1997)

Broadie, M., Glasserman, P.: Pricing American-style securities using simulation. J. Econ. Dyn. Control 21, 1323–1352 (1997)

Broadie, M., Glasserman, P.: A stochastic mesh method for pricing high-dimensional American options. J. Comput. Finance 7(4), 35–72 (2004)

Brock, W.A., Hommes, C.H.: Heterogeneous beliefs and routes to chaos in a simple asset pricing model. J. Econ. Dyn. Control 22, 1235–1274 (1998)

Broyden, C.G.: The convergence of a class of double-rank minimization algorithms 1. General considerations. IMA J. Appl. Math. 6, 76–90 (1970)

Bruti-Liberati, N., Platen, E.: On weak predictor-corrector schemes for jump-diffusion processes in finance. Research Paper, University of Sydney (2006)

Bunch, D.S., Johnson, H.: A simple and numerically efficient valuation method for American puts using a modified Geske-Johnson approach. J. Finance 47, 809–816 (1992)

Caflisch, R.E., Morokoff, W., Owen, A.: Valuation of mortgaged-backed securities using Brownian bridges to reduce effective dimension. J. Comput. Finance 1(1), 27–46 (1997)

Carmona, R., Durrleman, V.: Generalizing the Black–Scholes formula to multivariate contingent claims. J. Comput. Finance 9(2), 43–67 (2005)

Carr, P., Faguet, D.: Fast accurate valuation of American options. Working paper, Cornell University (1995)

Carr, P., Geman, H., Madan, D.B., Yor, M.: Stochastic volatility for Lévy processes. Math. Finance 13, 345–382 (2003)

Carr, P., Madan, D.B.: Option valuation using the fast Fourier transform. J. Comput. Finance 2(4), 61–73 (1999)

Carr, P., Wu, L.: Time-changed Lévy processes and option pricing. J. Financ. Econ. 71, 113–141 (2004)

Carriere, J.F.: Valuation of the early-exercise price for options using simulations and nonparametric regression. Insur. Math. Econ. 19, 19–30 (1996)

Cash, J.R.: Two new finite difference schemes for parabolic equations. SIAM J. Numer. Anal. 21, 433–446 (1984)

Chan, T.F., Golub, G.H., LeVeque, R.J.: Algorithms for computing the sample variance: analysis and recommendations. Am. Stat. 37, 242–247 (1983)

Chen, S.-H. (ed.): Genetic Algorithms and Genetic Programming in Computational Finance. Kluwer, Boston (2002)

Chen, X., Chadam, J.: Analytical and numerical approximations for the early exercise boundary for American put options. Dyn. Continuous Discrete Impulsive Syst. A 10, 649–660 (2003)

Chen, X., Chadam, J.: A mathematical analysis of the optimal exercise boundary for American put options. SIAM J. Math. Anal. 38, 1613–1641 (2007)

Chiarella, C., Dieci, R., Gardini, L.: Speculative behaviour and complex asset price dynamics. In: Bischi, G.I. (ed.) Proceedings Urbino 2000 (2000)

Choi, H.I., Heath, D., Ku, H.: Valuation and hedging of options with general payoff under transaction costs. J. Kor. Math. Soc. 41, 513–533 (2004)

Chung, K.L., Williams, R.J.: Introduction to Stochastic Integration. Birkhäuser, Boston (1983)

Ciarlet, P.G.: Basic error estimates for elliptic problems. In: Ciarlet, P.G., Lions, J.L. (eds.) Handbook of Numerical Analysis, Vol. II. Elsevier/North-Holland, Amsterdam (1991)

Ciarlet, P., Lions, J.L.: Finite Difference Methods (Part 1) Solution of Equations in \(\mathbb{R}^{n}\). North-Holland/Elsevier, Amsterdam (1990)

Clarke, N., Parrot, A.K.: Multigrid for American option pricing with stochastic volatility. Appl. Math. Finance 6, 177–179 (1999)

Clewlow, L., Strickland, C.: Implementing Derivative Models. Wiley, Chichester (1998)

Coleman, T.F., Li, Y., Verma, Y.: A Newton method for American option pricing. J. Comput. Finance 5(3), 51–78 (2002)

Cont, R., Tankov, P.: Financial Modelling with Jump Processes. Chapman & Hall, Boca Raton (2004)

Cont, R., Voltchkova, E.: Finite difference methods for option pricing in jump-diffusion and exponential Lévy models. SIAM J. Numer. Anal. 43, 1596–1626 (2005)

Cox, J.C., Ingersoll, J.E., Ross, S.A.: A theory of the term structure of interest rates. Econometrica 53, 385–407 (1985)

Cox, J.C., Ross, S., Rubinstein, M.: Option pricing: a simplified approach. J. Financ. Econ. 7, 229–263 (1979)

Cox, J.C., Rubinstein, M.: Options Markets. Prentice Hall, Englewood Cliffs (1985)

Crandall, M., Ishii, H., Lions, P.L.: User’s guide to viscosity solutions of second order partial differential equations. Bull. Am. Math. Soc. 27, 1–67 (1992)

Crank, J.: Free and Moving Boundary Problems. Clarendon Press, Oxford (1984)

Crank, J.C., Nicolson, P.: A practical method for numerical evaluation of solutions of partial differential equations of the heat-conductive type. Proc. Camb. Philos. Soc. 43, 50–67 (1947)

Cryer, C.: The solution of a quadratic programming problem using systematic overrelaxation. SIAM J. Control 9, 385–392 (1971)

Cyganowski, S., Kloeden, P., Ombach, J.: From Elementary Probability to Stochastic Differential Equations with MAPLE. Springer, Heidelberg (2001)

Dahlbokum, A.: Empirical performance of option pricing models based on time-changed Lévy processes. Available at SSRN: http://ssrn.com/abstract=1675321 (2010)

Dai, M.: A closed-form solution for perpetual American floating strike lookback options. J. Comput. Finance 4(2), 63–68 (2000)

Dai, T.-S., Lyuu, Y.-D.: The bino-trinomial tree: a simple model for efficient and accurate option pricing. J. Deriv. 17, 7–24 (2010)

Dana, R.-A., Jeanblanc, M.: Financial Markets in Continuous Time. Springer, Berlin (2003)

Dempster, M.A.H., Hutton, J.P.: Pricing American stock options by linear programming. Math. Finance 9, 229–254 (1999)

Dempster, M.A.H., Hutton, J.P., Richards, D.G.: LP valuation of exotic American options exploiting structure. J. Comput. Finance 2(1), 61–84 (1998)

Derman, E., Kani, I.: Riding on a smile. Risk 7, 32–39 (1994)

Detemple, J.: American options: symmetry properties. In: Jouini, E., et al. (eds.) Option Pricing, Interest Rates and Risk Management. Cambridge University Press, Cambridge (2001)

Deutsch, H.-P.: Derivatives and Internal Models. Palgrave, Houndmills (2002)

Devroye, L.: Non-uniform Random Variate Generation. Springer, New York (1986)

d’Halluin, Y., Forsyth, P.A., Labahn, G.: A semi-Lagrangian approach for American Asian options under jump diffusion. SIAM J. Sci. Comput. 27, 315–345 (2005)

d’Halluin, Y., Forsyth, P.A., Vetzal, K.R.: Robust numerical methods for contingent claims under jump diffusion processes. IMA J. Numer. Anal. 25, 87–112 (2005)

Dieci, R., Bischi, G.-I., Gardini, L.: From bi-stability to chaotic oscillations in a macroeconomic model. Chaos Solitons Fractals 12, 805–822 (2001)

Doeblin, W.: Sur l’équation de Kolmogorov (1940)

Doob, J.L.: Stochastic Processes. Wiley, New York (1953)

Dowd, K.: Beyond Value at Risk: The New Science of Risk Management. Wiley, Chichester (1998)

Duffie, D.: Dynamic Asset Pricing Theory, 2nd edn. Princeton University Press, Princeton (1996)

Duffie, D., Pan, J., Singleton, K.: Transform analysis and asset pricing for affine jump-diffusions. Econometrica 68, 1343–1376 (2000)

Dupire, B.: Pricing with a smile. Risk 7, 18–20 (1994)

Eberlein, E., Frey, R., Kalkbrener, M., Overbeck, L.: Mathematics in financial risk management. Jahresber. DMV 109, 165–193 (2007)

Eberlein, E., Keller, U.: Hyperbolic distributions in finance. Bernoulli 1, 281–299 (1995)

Egloff, D.: Monte Carlo algorithms for optimal stopping and statistical learning. Ann. Appl. Probab. 15, 1396–1432 (2005)

Ehrhardt, M. (ed.): Nonlinear Models in Mathematical Finance. New Research Trends in Option Pricing. Nova Science, Hauppauge (2008)

Ekström, E., Lötstedt, P., Tysk, J.: Boundary values and finite difference methods for the single factor term structure equation. Appl. Math. Finance 16, 253–259 (2009)

El Karoui, N., Jeanblanc-Picqué, M., Shreve, S.E.: Robustness of the Black and Scholes formula. Math. Finance 8, 93–126 (1998)

Elliott, C.M., Ockendon, J.R.: Weak and Variational Methods for Moving Boundary Problems. Pitman, Boston (1982)

Elliott, R.J., Kopp, P.E.: Mathematics of Financial Markets. Springer, New York (1999)

Embrechts, P., Klüppelberg, C., Mikosch, T.: Modelling Extremal Events. Springer, Berlin (1997)

Ender, M.: Model risk in option pricing. www.risknet.de/risknet-elibrary/kategorien/market-risk (2008)

Epps, T.W.: Pricing Derivative Securities. World Scientific, Singapore (2000)

Faigle, U., Schrader, R.: On the Convergence of Stationary Distributions in Simulated Annealing Algorithms. Inf. Process. Lett. 27, 189–194 (1988)

Fang, F., Oosterlee, C.W.: A novel option pricing method based on Fourier-cosine series expansions. SIAM J. Sci. Comput. 31, 826–848 (2008)

Fang, F., Oosterlee, C.W.: Pricing early-exercise and discrete barrier options by fourier-cosine series expansions. Numer. Math. 114, 27–62 (2009)

Feller, W.: An Introduction to Probability Theory and Its Applications. Wiley, New York (1950)

Fengler, M.R.: Semiparametric Modeling of Implied Volatility. Springer, Berlin (2005)

Figlewski, S., Gao, B.: The adaptive mesh model: a new approach to efficient option pricing. J. Financ. Econ. 53, 313–351 (1999)

Fishman, G.S.: Monte Carlo. Concepts, Algorithms, and Applications. Springer, New York (1996)

Fisz, M.: Probability Theory and Mathematical Statistics. Wiley, New York (1963)

Föllmer, H., Schied, A.: Stochastic Finance: An Introduction to Discrete Time. de Gruyter, Berlin (2002)

Forsyth, P.A., Vetzal, K.R.: Quadratic convergence for valuing American options using a penalty method. SIAM J. Sci. Comput. 23, 2095–2122 (2002)

Forsyth, P.A., Vetzal, K.R.: Numerical methods for nonlinear PDEs in finance. In: Duan, J.-C., Härdle, W.K., Gentle, J.E. (eds.) Handbook of Computational Finance, pp. 503–528. Springer, Berlin (2012)

Forsyth, P.A., Vetzal, K.R., Zvan, R.: A finite element approach to the pricing of discrete lookbacks with stochastic volatility. Appl. Math. Finance 6, 87–106 (1999)

Forsyth, P.A., Vetzal, K.R., Zvan, R.: Convergence of numerical methods for valuing path-dependent options using interpolation. Rev. Deriv. Res. 5, 273–314 (2002)

Fournié, E., Lasry, J.-M., Lebuchoux, J., Lions, P.-L., Touzi, N.: An application of Malliavin calculus to Monte Carlo methods in finance. Finance Stochast. 3, 391–412 (1999)

Franke, J., Härdle, W., Hafner, C.M.: Statistics of Financial Markets. Springer, Berlin (2004)

Freedman, D.: Brownian Motion and Diffusion. Holden Day, San Francisco (1971)

Frey, R., Patie, P.: Risk management for derivatives in illiquid markets: a simulation-study. In: Sandmann, K., Schönbucher, P. (eds.) Advances in Finance and Stochastics. Springer, Berlin (2002)

Frey, R., Stremme, A.: Market volatility and feedback effects from dynamic hedging. Math. Finance 7, 351–374 (1997)

Frutos, J. de: A spectral method for bonds. Comput. Oper. Res. 35, 64–75 (2008)

Fu, M.C., et al.: Pricing American options: a comparison of Monte Carlo simulation approaches. J. Comput. Finance 4(3), 39–88 (2001)

Fusai, G., Sanfelici, S., Tagliani, A.: Practical problems in the numerical solution of PDEs in finance. Rend. Studi Econ. Quant. 2001, 105–132 (2002)

Gander, M.J., Wanner, G.: From Euler, Ritz, and Galerkin to modern computing. SIAM Rev. 54, 627–666 (2012)

Geman, H., et al., eds.: Mathematical Finance. Bachelier Congress 2000. Springer, Berlin (2002)

Gentle, J.E.: Random Number Generation and Monte Carlo Methods. Springer, New York (1998)

Gerstner, T., Griebel, M.: Numerical integration using sparse grids. Numer. Algorithms 18, 209–232 (1998)

Gerstner, T., Griebel, M.: Dimension-adaptive tensor-product quadrature. Computing 71, 65–87 (2003)

Geske, R., Johnson, H.E.: The American put option valued analytically. J. Finance 39, 1511–1524 (1984)

Giles, M.: Variance reduction through multilevel Monte Carlo path calculations. In: Appleby, J.A.D., et al. (eds.) Numerical Methods for Finance. Chapman & Hall, Boca Raton (2008)

Giles, M., Glasserman, P.: Smoking adjoints: fast Monte Carlo methods. Risk 19, 88–92 (2006)

Gilks, W.R., Richardson, S., Spiegelhalter, D.J. (eds.): Markov Chain Monte Carlo in Practice. Chapman & Hall, Boca Raton (1996)

Glaser, J., Heider, P.: Arbitrage-free approximation of call price surfaces and input data risk. Quant. Finance 12, 61–73 (2012). doi:10.1080/14697688.2010.514005

Glasserman, P.: Monte Carlo Methods in Financial Engineering. Springer, New York (2004)

Glover, K.J., Duck, P.W., Newton, D.P.: On nonlinear models of markets with finite liquidity: some cautionary notes. SIAM J. Appl. Math. 70, 3252–3271 (2010)

Golub, G.H., Van Loan, C.F.: Matrix Computations, 3rd edn. The John Hopkins University Press, Baltimore (1996)

Goodman, J., Ostrov, D.N.: On the early exercise boundary of the American put option. SIAM J. Appl. Math. 62, 1823–1835 (2002)

Grandits, P.: Frequent hedging under transaction costs and a nonlinear Fokker-Planck PDE. SIAM J. Appl. Math. 62, 541–562 (2001)

Grüne, L., Kloeden, P.E.: Pathwise approximation of random ODEs. BIT 41, 710–721 (2001)

Hackbusch, W.: Multi-Grid Methods and Applications. Springer, Berlin (1985)

Hackbusch, W.: Elliptic Differential Equations: Theory and Numerical Treatment. Springer Series in Computational Mathematics, vol. 18. Berlin, Springer (1992)

Haentjens, T., in ’t Hout, K.: ADI finite difference discretization of the Heston-Hull-White PDE. In: Simos, T.E., et al. (eds.) Numerical Analysis and Applied Mathematics. AIP Conference Proceedings, vol. 1281, pp. 1995–1999 (2010)

Häggström, O.: Finite Markov Chains and Algorithmic Applications. Cambridge University Press, Cambridge (2002)

Hairer, E., Nørsett, S.P., Wanner, G.: Solving Ordinary Differential Equations I. Nonstiff Problems. Springer, Berlin (1993)

Halton, J.H.: On the efficiency of certain quasi-random sequences of points in evaluating multi-dimensional integrals. Numer. Math. 2, 84–90 (1960)

Hammersley, J.M., Handscomb, D.C.: Monte Carlo Methods. Methuen, London (1964)

Hämmerlin, G., Hoffmann, K.-H.: Numerical Mathematics. Springer, Berlin (1991)

Han, H., Wu, X.: A fast numerical method for the Black–Scholes equation of American options. SIAM J. Numer. Anal. 41, 2081–2095 (2003)

Harrison, J.M., Pliska, S.R.: Martingales and stochastic integrals in the theory of continuous trading. Stoch. Process. Appl. 11, 215–260 (1981)

Hart, J.F.: Computer Approximations. Wiley, New York (1968)

Haug, E.G.: The Complete Guide to Option Pricing Formulas, 2nd edn. 2007. McGraw-Hill, New York (1998)

He, C., Kennedy, J.S., Coleman, T., Forsyth, P.A., Li, Y., Vetzal, K.: Calibration and hedging under jump diffusion. Rev. Deriv. Res. 9, 1–35 (2006)

Heider, P.: A condition number for the integral representation of American options. J. Comput. Finance 11(2), 95–103 (2007/08)

Heider, P.: A second-order Nyström-type discretization for the early-exercise curve of American put options. Int. J. Comput. Math. 86, 982–991 (2009)

Heider, P.: Numerical methods for non-linear Black–Scholes equations. Appl. Math. Finance 17, 59–81 (2010)

Heider, P., Schaeling, D.: Numerical methods for American options in nonlinear Black–Scholes models. Preprint, Universität Köln (2010)

Heston, S.L.: A closed-form solution for options with stochastic volatility with applications to bond and currency options. Rev. Financ. Stud. 6, 327–343 (1993)

Heston, S., Zhou, G.: On the rate of convergence of discrete-time contingent claims. Math. Finance 10, 53–75 (2000)

Higham, D.J.: An algorithmic introduction to numerical solution of stochastic differential equations. SIAM Rev. 43, 525–546 (2001)

Higham, D.J.: An Introduction to Financial Option Valuation. Cambridge University Press, Cambridge (2004)

Higham, D.J., Kloeden, P.E.: Numerical methods for nonlinear stochastic differential equations with jumps. Numer. Math. 101, 101–119 (2005)

Higham, N.J.: Accuracy and Stability of Numerical Algorithms. SIAM, Philadelphia (1996)

Higham, N.J.: Computing the nearest correlation matrix — a problem from finance. IMA J. Numer. Anal. 22, 329–343 (2002)

Hilber, N., Matache, A.-M., Schwab, C.: Sparse wavelet methods for option pricing under stochastic volatility. J. Comput. Finance 8(4), 1–42 (2005)

Hofmann, N., Platen, E., Schweizer, M.: Option pricing under incompleteness and stochastic volatility. Math. Finance 2, 153–187 (1992)

Hoggard, T., Whalley, A.E., Wilmott, P.: Hedging option portfolios in the presence of transaction costs. Adv. Futur. Options Res. 7, 21–35 (1994)

Holmes, A.D., Yang, H.: A front-fixing finite element method for the valuation of American options. SIAM J. Sci. Comput. 30, 2158–2180 (2008)

Honoré, P., Poulsen, R.: Option pricing with EXCEL. In: Nielsen, S. (ed.): Programming Languages and Systems in Computational Economics and Finance, pp. 369–402. Kluwer, Amsterdam (2002)

Huang, J.-Z., Subrahmanyam, M.G., Yu, G.G.: Pricing and hedging American options: a recursive integration method. Rev. Financ. Stud. 9, 227–300 (1996)

Hull, J.C.: Options, Futures, and Other Derivatives, 4th edn. Prentice Hall, Upper Saddle River (2000)

Hull, J., White, A.: The use of the control variate technique in option pricing. J. Financ. Quant. Anal. 23, 237–251 (1988)

Hunt, P.J., Kennedy, J.E.: Financial Derivatives in Theory and Practice. Wiley, Chichester (2000)

Ikonen, S., Toivanen, J.: Pricing American options using LU decomposition. Appl. Math. Sci. 1, 2529–2551 (2007)

Ikonen, S., Toivanen, J.: Operator splitting methods for pricing American options under stochastic volatility. Numer. Math. 113, 299–324 (2009)

Ingersoll, J.E.: Theory of Financial Decision Making. Rowmann and Littlefield, Savage (1987)

Int-Veen, R.: Avoiding numerical dispersion in option valuation. Report Universität Köln 2002; Comput. Vis. Sci. 10, 185–195 (2007)

Isaacson, E., Keller, H.B.: Analysis of Numerical Methods. Wiley, New York (1966)

Jacod, J., Protter, P.: Probability Essentials, 2nd edn. Springer, Berlin (2003)

Jäckel, P.: Monte Carlo Methods in Finance. Wiley, Chichester (2002)

Jaillet, P., Lamberton, D., Lapeyre, B.: Variational inequalities and the pricing of American options. Acta Appl. Math. 21, 263–289 (1990)

Jamshidian, F.: An analysis of American options. Rev. Futur. Mark. 11, 72–80 (1992)

Jiang, L., Dai, M.: Convergence of binomial tree method for European/American path-dependent options. SIAM J. Numer. Anal. 42, 1094–1109 (2004)

Johnson, H.E.: An analytic approximation for the American put price. J. Financ. Quant. Anal. 18, 141–148 (1983)

Jonen, C.: An efficient implementation of a least-squares Monte Carlo method for valuing American-style options. Int. J. Comput. Math. 86, 1024–1039 (2009)

Jonen, C.: Efficient Pricing of High-Dimensional American-Style Derivatives: A Robust Regression Monte Carlo method. PhD dissertation, Universität Köln (2011). http://kups.ub.uni-koeln.de/4442

Joshi, M.S.: The Concepts and Practice of Mathematical Finance. Cambridge University Press, Cambridge (2003)

Ju, N.: Pricing an American option by approximating its early exercise boundary as a multipiece exponential function. Rev. Financ. Stud. 11, 627–646 (1998)

Kaebe, C., Maruhn, J.H., Sachs, E.W.: Adjoint-based Monte Carlo calibration of financial market models. Finance Stochast. 13, 351–379 (2009)

Kahaner, D., Moler, C., Nash, S.: Numerical Methods and Software. Prentice Hall Series in Computational Mathematics. Prentice Hall, Englewood Cliffs (1989)

Kallast, S., Kivinukk, A.: Pricing and hedging American options using approximations by Kim integral equations. Eur. Finance Rev. 7, 361–383 (2003)

Kallsen, J.: A didactic note on affine stochastic volatility models. In: Kabanov, Y., et al. (eds.) From Stochastic Calculus to Mathematical Finance. Springer, Berlin (2006)

Kamrad, B., Ritchken, P.: Multinomial approximating models for options with k state variables. Manag. Sci. 37, 1640–1652 (1991)

Kangro, R., Nicolaides, R.: Far field boundary conditions for Black-Scholes equations. SIAM J. Numer. Anal. 38, 1357–1368 (2000)

Kantorovich, L.W., Akilov, G.P.: Functional Analysis in Normed Spaces. Pergamon Press, Elmsford (1964)

Karatzas, I., Shreve, S.E.: Brownian Motion and Stochastic Calculus, 2nd edn. Springer Graduate Texts. Springer, New York (1991)

Karatzas, I., Shreve, S.E.: Methods of Mathematical Finance. Springer, New York (1998)

Kat, H.M.: Pricing Lookback options using binomial trees: an evaluation. J. Financ. Eng. 4, 375–397 (1995)

Kebaier, A.: Statistical Romberg extrapolation: a new variance reduction method and applications to option pricing. Ann. Appl. Probab. 15, 2681–2705 (2005)

Kemna, A.G.Z., Vorst, A.C.F.: A pricing method for options based on average asset values. J. Bank. Finance 14, 113–129 (1990)

Khaliq, A.Q.M., Voss, D.A., Yousuf, M.: Pricing exotic options with L-stable Padé schemes. J. Bank. Finance 31, 3438–3461 (2007)

Kim, J.: The analytic valuation of American options. Rev. Financ. Stud. 3, 547–572 (1990)

Kirkpatrick, S., Gelatt, C.D., Vecchi, M.P.: Optimization by simulated annealing. Science 220, 671–680 (1983)

Klassen, T.R.: Simple, fast and flexible pricing of Asian options. J. Comput. Finance 4(3), 89–124 (2001)

Kloeden, P.E., Platen, E.: Numerical Solution of Stochastic Differential Equations. Springer, Berlin (1992)

Knuth, D.: The Art of Computer Programming, vol. 2. Addison-Wesley, Reading (1995)

Kocis, L., Whiten, W.J.: Computational investigations of low-discrepancy sequences. ACM Trans. Math. Softw. 23, 266–294 (1997)

Korn, R., Müller, S.: The decoupling approach to binomial pricing of multi-asset options. J. Comput. Finance 12(3), 1–30 (2009)

Kou, S.G.: A jump diffusion model for option pricing. Manag. Sci. 48, 1086–1101 (2002)

Kovalov, P., Linetsky, V., Marcozzi, M.: Pricing multi-asset American options: a finite element method-of-lines with smooth penalty. J. Sci. Comput. 33, 209–237 (2007)

Kreiss, H.O., Thomée, V., Widlund, O.: Smoothing of initial data and rates of convergence for parabolic difference equations. Commun. Pure Appl. Math. 23, 241–259 (1970)

Kröner, D.: Numerical Schemes for Conservation Laws. Wiley, Chichester (1997)

Krylov, N.V.: Controlled Diffusion Processes. Springer, Heidelberg (1980)

Kwok, Y.K.: Mathematical Models of Financial Derivatives. Springer, Singapore (1998)

Kwok, Y.K., Leung, K.S., Wong, H.Y.: Efficient options pricing using the Fast Fourier Transform. In: Duan, J.-C., Härdle, W.K., Gentle, J.E. (eds.) Handbook of Computational Finance, pp. 579–604. Springer, Berlin (2012)

Lambert, J.D.: Numerical Methods for Ordinary Differential Systems. The Initial Value Problem. Wiley, Chichester (1991)

Lamberton, D., Lapeyre, B.: Introduction to Stochastic Calculus Applied to Finance. Chapman & Hall, London (1996)

Lange, K.: Numerical Analysis for Statisticians. Springer, New York (1999)

L’Ecuyer, P.: Tables of linear congruential generators of different sizes and good lattice structure. Math. Comput. 68, 249–260 (1999)

Leentvaar, C.C.W., Oosterlee, C.W.: On coordinate transformation and grid stretching for sparse grid pricing of basket options. J. Comput. Math. 222, 193–209 (2008)

Lehn, J.: Random number generators. GAMM-Mitteilungen 25, 35–45 (2002)

Leisen, D.P.J.: Pricing the American put option: a detailed convergence analyis for binomial models. J. Econ. Dyn. Control 22, 1419–1444 (1998)

Leisen, D.P.J.: The random-time binomial model. J. Econ. Dyn. Control 23, 1355–1386 (1999)

Leisen, D.P.J., Reimer, M.: Binomial models for option valuation – examining and improving convergence. Appl. Math. Finance 3, 319–346 (1996)

Leland, H.E.: Option pricing and replication with transaction costs. J. Finance 40, 1283–1301 (1985)

Levy, G.: Computational finance using C and C#. Elsevier, Amsterdam (2008)

Longstaff, F.A., Schwartz, E.S.: Valuing American options by simulation: a simple least-squares approach. Rev. Financ. Stud. 14, 113–147 (2001)

Lord, R., Fang, F., Bervoets, F., Oosterlee, C.W.: A fast and accurate FFT-based method for pricing early-exercise options under Lévy processes. SIAM J. Sci. Comput. 30, 1678–1705 (2008)

Lux, T.: The socio-economic dynamics of speculative markets: interacting agents, chaos, and the fat tails of return distributions. J. Econ. Behav. Organ. 33, 143–165 (1998)

Lyons, T.J.: Uncertain volatility and the risk-free synthesis of derivatives. Appl. Math. Finance 2, 117–133 (1995)

Lyuu, Y.-D.: Financial Engineering and Computation. Principles, Mathematics, Algorithms. Cambridge University Press, Cambridge (2002)

MacMillan, L.W.: Analytic approximation for the American put option. Adv. Futur. Opt. Res. 1, 119–139 (1986)

Madan, D.B., Seneta, E.: The variance-gamma (V.G.) model for share market returns. J. Bus. 63, 511–524 (1990)

Mainardi, R., Roberto, M., Gorenflo, R., Scalas, E.: Fractional calculus and continuous-time finance II: the waiting-time distribution. Physica A 287, 468–481 (2000)

Maller, R.A., Solomon, D.H., Szimayer, A.: A multinomial approximation for American option prices in Lévy process models. Math. Finance 16, 613–633 (2006)

Mandelbrot, B.B.: A multifractal walk down Wall Street. Sci. Am. 280, 70–73 (1999)

Manteuffel, T.A., White, A.B., Jr.: The numerical solution of second-order boundary value problems on nonuniform meshes. Math. Comput. 47, 511–535 (1986)

Marchesi, M., Cinotti, S., Focardi, S., Raberto, M.: Development and testing of an artificial stock market. In: Bischi, G.I. (ed.) Proceedings Urbino 2000 (2000)

Marsaglia, G.: Random numbers fall mainly in the planes. Proc. Natl. Acad. Sci. USA 61, 23–28 (1968)

Marsaglia, G., Bray, T.A.: A convenient method for generating normal variables. SIAM Rev. 6, 260–264 (1964)

Marsaglia, G., Tsang, W.W.: The ziggurat method for generating random variables. J. Stat. Softw. 5(8), 1–7 (2000)

Mascagni, M.: Parallel pseudorandom number generation. SIAM News 32, 5 (1999)

Matache, A.-M., von Petersdorff, T., Schwab, C.: Fast deterministic pricing of options on Lévy driven assets. Report 2002–11, Seminar for Applied Mathematics, ETH Zürich (2002)

Matsumoto, M., Nishimura, T.: Mersenne twister: a 623-dimensionally equidistributed uniform pseudorandom number generator. ACM Trans. Model. Comput. Simul. 8, 3–30 (1998)

Mayo, A.: Fourth order accurate implicit finite difference method for evaluating American options. In: Proceedings of Computational Finance, London (2000)

McCarthy, L.A., Webber, N.J.: Pricing in three-factor models using icosahedral lattices. J. Comput. Finance 5(2), 1–33 (2001/02)

McDonald, R.L., Schroder, M.D.: A parity result for American options. J. Comput. Finance 1(3), 5–13 (1998)

Mel’nikov, A.V., Volkov, S.N., Nechaev, M.L.: Mathematics of Financial Obligations. American Mathematical Society, Providence (2002)

Merton, R.C.: Theory of rational option pricing. Bell J. Econ. Manag. Sci. 4, 141–183 (1973)

Merton, R.: Option pricing when underlying stock returns are discontinous. J. Financ. Econ. 3, 125–144 (1976)

Merton, R.C.: Continuous-Time Finance. Blackwell, Cambridge (1990)

Metwally, S.A.K., Atiya, A.: Using Brownian bridge for fast simulation of jump-diffusion processes and barrier options. J. Derv. 10, 43–54 (2002)

Meyer, G.H.: Numerical Investigation of early exercise in American puts with discrete dividends. J. Comput. Finance 5(2), 37–53 (2002)

Mikosch, T.: Elementary Stochastic Calculus, with Finance in View. World Scientific, Singapore (1998)

Mil’shtein, G.N.: Approximate integration of stochastic differential equations. Theory Probab. Appl. 19, 557–562 (1974)

Milshtein, G.N.: A method of second-order accuracy integration of stochastic differential equations. Theory Probab. Appl. 23, 396–401 (1978)

van Moerbeke, P.: On optimal stopping and free boundary problems. Rocky Mt. J. Math. 4, 539–578 (1974)

Moro, B.: The full Monte. Risk 8, 57–58 (1995)

Morokoff, W.J.: Generating quasi-random paths for stochastic processes. SIAM Rev. 40, 765–788 (1998)

Morokoff, W.J., Caflisch, R.E.: Quasi-random sequences and their discrepancies. SIAM J. Sci. Comput. 15, 1251–1279 (1994)

Morton, K.W.: Numerical Solution of Convection-Diffusion Problems. Chapman & Hall, London (1996)

Musiela, M., Rutkowski, M.: Martingale Methods in Financial Modelling, 2nd edn. 2005. Springer, Berlin (1997)

Neftci, S.N.: An Introduction to the Mathematics of Financial Derivatives. Academic Press, San Diego (1996)

Newton, N.J.: Continuous-time Monte Carlo methods and variance reduction. In: Rogers, L.C.G., Talay, D. (eds.) Numerical Methods in Finance, pp. 22–42. Cambridge University Press, Cambridge (1997)

Niederreiter, H.: Quasi-Monte Carlo methods and pseudo-random numbers. Bull. Am. Math. Soc. 84, 957–1041 (1978)

Niederreiter, H.: Random Number Generation and Quasi-Monte Carlo Methods. Society for Industrial and Applied Mathematics, Philadelphia (1992)

Niederreiter, H., Jau-Shyong Shiue, P. (eds.): Monte Carlo and Quasi-Monte Carlo methods in scientific computing. In: Proceedings of a Conference at the University of Nevada, Las Vegas, Nevada, USA, 1994. Springer, New York (1995)

Nielsen, B.F., Skavhaug, O., Tveito, A.: Penalty and front-fixing methods for the numerical solution of American option problems. J. Comput. Finance 5(4), 69–97 (2002)

Nielsen, B.F., Skavhaug, O., Tveito, A.: Penalty methods for the numerical solution of American multi-asset option problems. J. Comput. Appl. Math. 222, 3–16 (2008)

Nielsen, L.T.: Pricing and Hedging of Derivative Securities. Oxford University Press, Oxford (1999)

Øksendal, B.: Stochastic Differential Equations. Springer, Berlin (1998)

Omberg, E.: The valuation of American put options with exponential exercise policies. Adv. Futur. Opt. Res. 2, 117–142 (1987)

Oosterlee, C.W.: On multigrid for linear complementarity problems with application to American-style options. Electron. Trans. Numer. Anal. 15, 165–185 (2003)

Panini, R., Srivastav, R.P.: Option pricing with Mellin transforms. Math. Comput. Model. 40, 43–56 (2004)

Papageorgiou, A., Traub, J.F.: New results on deterministic pricing of financial derivatives. Columbia University Report CUCS-028-96 (1996)

Paskov, S., Traub, J.: Faster valuation of financial derivatives. J. Portf. Manag. 22, 113–120 (1995)

Pelsser, A., Vorst, T.: The binomial model and the Greeks. J. Deriv. 1, 45–49 (1994)

Peyret, R., Taylor, T.D.: Computational Methods for Fluid Flow. Springer, New York (1983)

Pham, H.: Optimal stopping, free boundary, and American option in a jump-diffusion model. Appl. Math. Optim. 35, 145–164 (1997)

Pironneau, O., Hecht, F.: Mesh adaption for the Black & Scholes equations. East-West J. Numer. Math. 8, 25–35 (2000)

Platen, E.: An introduction to numerical methods for stochastic differential equations. Acta Numer. 8, 197–246 (1999)

Pliska, S.R.: Introduction to Mathematical Finance. Discrete Time Models. Blackwell, Malden (1997)

Pooley, D.M., Forsyth, P.A., Vetzal, K.R.: Numerical convergence properties of option pricing PDEs with uncertain volatility. IMA J. Numer. Anal. 23, 241–267 (2003)

Pooley, D.M., Forsyth, P.A., Vetzal, K., Simpson, R.B.: Unstructured meshing for two asset barrier options. Appl. Math. Finance 7, 33–60 (2000)

Pooley, D.M., Vetzal, K.R., Forsyth, P.A.: Convergence remedies for non-smooth payoffs in option pricing. J. Comput. Finance 6(4), 25–40 (2003)

Press, W.H., Teukolsky, S.A., Vetterling, W.T., Flannery, B.P.: Numerical Recipes in FORTRAN. The Art of Scientific Computing, 2nd edn. Cambridge University Press, Cambridge (1992)

Protter, P.E.: Stochastic Integration and Differential Equations. Springer, Berlin (2004)

Quarteroni, A., Sacco, R., Saleri, F.: Numerical Mathematics. Springer, New York (2000)

Quecke, S.: Efficient numerical methods for pricing American options under Lévy models. PhD-dissertation, Universität Köln (2007). http://kups.ub.uni-koeln.de/2018

Rannacher, R.: Finite element solution of diffusion problems with irregular data. Numer. Math. 43, 309–327 (1984)

Rebonato, R.: Interest-Rate Option Models: Understanding, Analysing and Using Models for Exotic Interest-Rate Options. Wiley, Chichester (1996)

Reisinger, C.: Numerische Methoden für hochdimensionale parabolische Gleichungen am Beispiel von Optionspreisaufgaben. PhD Thesis, Universität Heidelberg (2004)

Rendleman, R.J., Bartter, B.J.: Two-state option pricing. J. Finance 34, 1093–1110 (1979)

Revuz, D., Yor, M.: Continuous Martingales and Brownian Motion. Springer, Berlin (1991)

Ribeiro, C., Webber, N.: A Monte Carlo method for the normal inverse Gaussian option valuation model using an inverse Gaussian bridge. Working paper, City University, London (2002)

Ribeiro, C., Webber, N.: Valuing path dependent options in the variance-gamma model by Monte Carlo with a gamma bridge. J. Comput. Finance 7(2), 81–100 (2003/04)

Ripley, B.D.: Stochastic Simulation. Wiley Series in Probability and Mathematical Statistics. Wiley, New York (1987)

Risken, H.: The Fokker-Planck Equation. Springer, Berlin (1989)

Rogers, L.C.G.: Monte Carlo valuation of American options. Math. Finance 12, 271–286 (2002)

Rogers, L.C.G., Shi, Z.: The value of an Asian option. J. Appl. Probab. 32, 1077–1088 (1995)

Rogers, L.C.G., Talay, D. (eds.): Numerical Methods in Finance. Cambridge University Press, Cambridge (1997)

Rubinstein, M.: Implied binomial trees. J. Finance 69, 771–818 (1994)

Rubinstein, M.: Return to oz. Risk 7(11), 67–71 (1994)

Rubinstein, R.Y.: Simulation and the Monte Carlo Method. Wiley, New York (1981)

Ruppert, D.: Statistics and Finance. An Introduction. Springer, New York (2004)

Saad, Y.: Iterative Methods for Sparse Linear Systems, 2nd edn. SIAM, Philadelphia (2003)

Saito, Y., Mitsui, T.: Stability analysis of numerical schemes for stochastic differential equations. SIAM J. Numer. Anal. 33, 2254–2267 (1996)

Sato, K.-I.: Lévy Processes and Infinitely Divisible Distributions. Cambridge University Press, Cambridge (1999)

Schöbel, R., Zhu, J.: Stochastic volatility with an Ornstein-Uhlenbeck process: an extension. Eur. Finance Rev. 3(1), 23–46 (1999)

Schönbucher, P.J., Wilmott, P.: The feedback effect of hedging in illiquid markets. SIAM J. Applied Mathematics 61, 232–272 (2000)

Schoenmakers, J.G.M., Heemink, A.W.: Fast Valuation of Financial Derivatives. J. Comput. Finance 1, 47–62 (1997)

Schoutens, W.: Lévy Processes in Finance. Wiley, Chichester (2003)

Schuss, Z.: Theory and Applications of Stochastic Differential Equations. Wiley Series in Probability and Mathematical Statistics. Wiley, New York (1980)

Schwarz, H.R.: Numerical Analysis. Wiley, Chichester (1989)

Schwarz, H.R.: Methode der finiten Elemente. Teubner, Stuttgart (1991)

Seydel, R.: Practical Bifurcation and Stability Analysis, 3rd edn. Springer Interdisciplinary Applied Mathematics, vol. 5. Springer, New York (2010)

Seydel, R.U.: Lattice approach and implied trees. In: Duan, J.-C., Härdle, W.K., Gentle, J.E. (eds.) Handbook of Computational Finance, pp. 551–577. Springer, Berlin (2012)

Seydel, R.U.: Risk and computation. In: Glau, K., Scherer, M., Zagst, R. (eds.) Innovations in Quantitative Risk Management, pp. 305–316. Springer, Heidelberg (2015)

Shiryaev, A.N.: Essentials of Stochastic Finance. Facts, Models, Theory. World Scientific, Singapore (1999)

Shreve, S.E.: Stochastic Calculus for Finance II. Continuous-Time Models. Springer, New York (2004)

Smith, G.D.: Numerical Solution of Partial Differential Equations: Finite Difference Methods, 2nd edn. Clarendon Press, Oxford (1978)

Smithson, C.: Multifactor options. Risk 10(5), 43–45 (1997)

Spanier, J., Maize, E.H.: Quasi-random methods for estimating integrals using relatively small samples. SIAM Rev. 36, 18–44 (1994)

Stauffer, D.: Percolation models of financial market dynamics. Adv. Complex Syst. 4, 19–27 (2001)

Steele, J.M.: Stochastic Calculus and Financial Applications. Springer, New York (2001)

Steiner, M., Wallmeier, M., Hafner, R.: Baumverfahren zur Bewertung diskreter Knock-Out-Optionen. OR Spektrum 21, 147–181 (1999)

Stoer, J., Bulirsch, R.: Introduction to Numerical Analysis. Springer, Berlin (1996)

Stoer, J., Witzgall, C.: Convexity and Optimization in Finite Dimensions I. Springer, Berlin (1970)

Stojanovic, S.: Computational Financial Mathematics Using MATHEMATICA. Birkhäuser, Boston (2003)

Strang, G.: Computational Science and Engineering. Wellesley, Cambridge (2007)

Strang, G., Fix, G.: An Analysis of the Finite Element Method. Prentice-Hall, Englewood Cliffs (1973)

Sweby, P.K.: High resolution schemes using flux limiters for hyperbolic conservation laws. SIAM J. Numer. Anal. 21, 995–1011 (1984)

Tavella, D., Randall, C.: Pricing Financial Instruments. The Finite Difference Method. Wiley, New York (2000)

Tezuka, S.: Uniform Random Numbers: Theory and Practice. Kluwer, Dordrecht (1995)

Thomas, D.B., Luk, W., Leong, P.H.W., Villasenor, J.D.: Gaussian random number generators. ACM Comput. Surv. 39(4), Article 11 (2007)

Thomas, J.W.: Numerical Partial Differential Equations: Finite Difference Methods. Springer, New York (1995)

Thomas, J.W.: Numerical Partial Differential Equations. Conservation Laws and Elliptic Equations. Springer, New York (1999)

Tian, Y.: A modified lattice approach to option pricing. J. Futur. Mark. 13, 563–577 (1993)

Tian, Y.: A flexible binomial option pricing model. J. Futur. Mark. 19, 817–843 (1999)

Tilley, J.A.: Valuing American options in a path simulation model. Trans. Soc. Actuar. 45, 83–104 (1993)

Topper, J.: Finite element modeling of exotic options. In: OR Proceedings 1999, pp. 336–341 (2000)

Topper, J.: Financial Engineering with Finite Elements. Wiley, New York (2005)

Traub, J.F., Wozniakowski, H.: The Monte Carlo algorithm with a pseudo-random generator. Math. Comput. 58, 323–339 (1992)

Trottenberg, U., Oosterlee, C., Schüller, A.: Multigrid. Academic Press, San Diego (2001)

Tsay, R.S.: Analysis of Financial Time Series. Wiley, New York (2002)

van der Vorst, H.A.: Bi-CGSTAB: a fast and smoothly converging variant of Bi-CG for the solution of nonsymmetric linear systems. SIAM J. Sci. Stat. Comput. 13, 631–644 (1992)

Varga, R.S.: Matrix Iterative Analysis. Prentice Hall, Englewood Cliffs (1962)

Vellekoop, M.H., Nieuwenhuis, J.W.: Efficient pricing of derivatives on assets with discrete dividends. Appl. Math. Finance 13, 265–284 (2006)

Vichnevetsky, R.: Computer Methods for Partial Differential Equations. Volume I. Prentice-Hall, Englewood Cliffs (1981)

Villeneuve, S., Zanette, A.: Parabolic ADI methods for pricing American options on two stocks. Math. Oper. Res. 27, 121–149 (2002)

Vretblad, A.: Fourier Analysis and Its Applications. Springer, New York (2003)

Wallace, C.S.: Fast pseudorandom numbers for normal and exponential variates. ACM Trans. Math. Softw. 22(1), 119–127 (1996)

Wang, X., Phillips, P.C.B., Yu, J.: Bias in estimating multivariate and univariate diffusion. J. Econ. 161, 228–245 (2011)

Wesseling, P.: Principles of Computational Fluid Dynamics. Springer, Berlin (2001)

Wilmott, P.: Derivatives. Wiley, Chichester (1998)

Wilmott, P., Dewynne, J., Howison, S.: Option Pricing. Mathematical Models and Computation. Oxford Financial Press, Oxford (1996)

Wloka, J.: Partial Differential Equations. Cambridge University Press, Cambridge (1987)

Zagst, R.: Interest-Rate Management. Springer, Berlin (2002)

Zhang, J.E.: A semi-analytical method for pricing and hedging continuously sampled arithmetic average rate options. J. Comput. Finance 5(1), 59–79 (2001)

Zhao, Y., Ziemba, W.T.: Hedging errors with Leland’s option model in the presence of transaction costs. Finance Res. Lett. 4, 49–58 (2007)

Zhu, Y.-I., Wu, X., Chern, I.-L.: Derivative Securities and Difference Methods. Springer, New York (2004)

Zienkiewicz, O.C.: The Finite Element Method in Engineering Science. McGraw-Hill, London (1977)

Zvan, R., Forsyth, P.A., Vetzal, K.R.: Robust numerical methods for PDE models of Asian options. J. Comput. Finance 1(2), 39–78 (1997/98)

Zvan, R., Forsyth, P.A., Vetzal, K.R.: Penalty methods for American options with stochastic volatility. J. Comput. Appl. Math. 91, 199–218 (1998)

Zvan, R., Forsyth, P.A., Vetzal, K.R.: Discrete Asian barrier options. J. Comput. Finance 3(1), 41–67 (1999)

Zvan, R., Vetzal, K.R., Forsyth, P.A.: PDE methods for pricing barrier options. J. Econ. Dyn. Control 24, 1563–1590 (2000)

Author information

Authors and Affiliations

Rights and permissions

Copyright information

© 2017 Springer-Verlag London Ltd.

About this chapter

Cite this chapter

Seydel, R.U. (2017). Pricing of Exotic Options. In: Tools for Computational Finance. Universitext. Springer, London. https://doi.org/10.1007/978-1-4471-7338-0_6

Download citation

DOI: https://doi.org/10.1007/978-1-4471-7338-0_6

Published:

Publisher Name: Springer, London

Print ISBN: 978-1-4471-7337-3

Online ISBN: 978-1-4471-7338-0

eBook Packages: Mathematics and StatisticsMathematics and Statistics (R0)