Abstract

This speech compares and contrasts two different interpretations of the current plight of the global economy. It argues that the world has been suffering not so much from a structural deficiency in aggregate demand—secular stagnation—but from the aftermath of financial booms gone wrong—financial cycle drag. This perspective suggests that the very low levels of interest rates that have prevailed are not necessarily equilibrium ones—consistent with the “natural rate”. And although it indicates that the headwinds from the financial bust, while very persistent, are temporary, it also points to a number of material risks ahead: further episodes of financial distress, a “debt trap” and, ultimately, a rupture in the open global economic order. To limit these risks, policies should be rebalanced towards structural measures and address more systematically the financial cycle.

Source: Drehmann et al. (2012), updated

Source: Borio et al. (2015a)

Source: Borio et al. (2016)

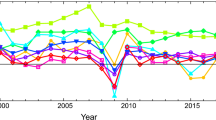

Source: Auer et al. (2017)

Sources: IMF, World Economic Outlook; OECD, Economic Outlook; national data; BIS calculations

Similar content being viewed by others

Notes

By “traditional” business cycle, I mean how economists and policymakers conceive and measure the typical fluctuations in output, as reflected in the specific statistical techniques (e.g. statistical filters). The notion of the financial cycle has a long historical tradition (see Drehmann et al. 2012 for references) and, as noted, was stressed again in BIS work going back at least to the early 2000s. For other empirical evidence on the financial cycle, see, e.g., Claessens et al. (2011), Aikman et al. (2015), De Bonis and Silvestrini (2014), Schüler et al. (2015), Einarsson et al. (2016) and Rünstler and Vlekke (2016).

See the BCBS (2010) survey and, in particular, Cerra and Saxena (2008) and, more recently, Ball (2014). Blanchard et al. (2015) find that other recessions too may have a similar effect. On the costs of credit booms in general, see Reinhart and Reinhart (2010), Jordà et al. (2013) and Mian et al. (2015); and on the experience of the Great Depression, see Eichengreen and Mitchener (2004).

On the role of globalisation in driving inflation, see Borio and Filardo (2007) and BIS (2014). For empirical studies reaching similar conclusions, see, e.g., Bianchi and Civelli (2013), Ciccarelli and Mojon (2010), Eickmeier and Moll (2009) and Pain et al. (2008); for others that disagree, see, e.g., Ihrig et al. (2010), Martínez-García and Wynne (2012) and Lodge and Mikolajun (2016).

This phenomenon has been greatly boosted by technology, which has allowed the relocation of production to lower-cost countries; see Baldwin (2016).

On some of the difficulties with this approach, see also Taylor and Wieland (2016). A second set of approaches assumes that the trend of the (long-term) rate tracks the natural rate and tries to explain it with reference to structural factors, such as demographics (e.g. Gagnon et al. 2016), generally not by estimating the link but showing that a calibrated model could reproduce the observed path.

That said, on the pitfalls in interpreting long-term yields as reflecting “market” expectations, see Shin (2017).

In a similar vein, Blanchard et al. (2017) argue that the low growth post-crisis has partly reflected temporary factors such as agents’ pessimism about future growth potential, in turn reflected in long-term yields that are too low compared with true growth prospects.

To be sure, lower interest rates can still sustain expenditures to the extent that they reduce debt service burdens and hence generate resources to repay debt. The point is that agents that realise they have borrowed too much would give priority to balance sheet repair and debt repayment, so that additional income would tend to be saved rather than spent, regardless of any restrictions on the supply of credit (Borio 2014a). On this, see also Koo (2003), who was the first to use the term “balance sheet recession”. While bearing some obvious similarities with his use of the term, the notion of a balance sheet recession here leads to somewhat different policy conclusions; see Borio (2014a) for a further elaboration. See also Bech et al. (2014) for empirical evidence on the importance of deleveraging and on the more muted effectiveness of monetary policy in the context of balance sheet recessions.

The mechanisms are discussed in detail in, e.g., Borio and Disyatat (2011), Borio (2014b), Shin (2012), Bruno and Shin (2014) and McCauley et al. (2015). See also Rey (2013) for the notion of a global financial cycle and Hofmann and Bogdanova (2012), updated in BIS (2016), for evidence that globally policy interest rates are unusually low compared with traditional benchmarks.

Between 2009 and the third quarter of 2016, US dollar credit to non-banks outside the United States increased by some 50%, to some $10.5 trillion, and it roughly doubled to those in emerging market economies alone, to around $3.6 trillion.

Rajan (2014) refers to this process as “competitive easing“.

It is often argued that such measures would depress demand, at least in the short term, and hence possibly make matters worse. But the empirical evidence suggests otherwise for a broad range of measures. See Bouis et al. (2012).

References

Aikman, D., A. Haldane, and B. Nelson. 2015. Curbing the credit cycle. The Economic Journal 125: 1072–1109.

Arseneau, D., and M. Kiley. 2014. The role of financial imbalances in assessing the state of the economy. FEDS Notes 2014-04-18, Board of Governors of the Federal Reserve System.

Atkeson, A., and P. Kehoe. 2004. Deflation and depression: Is there an empirical link? American Economic Review 94 (2):99–103.

Auer, R., C. Borio, and A. Filardo. 2017. The globalisation of inflation: The growing importance of global value chains. BIS Working Papers, No. 602, January.

Baldwin, R. 2016. The great convergence: Information technology and the new globalization. Cambridge: Belknap Press.

Ball, L. 2014. Long-term damage from the Great Recession in OECD countries. European Journal of Economics and Economic Policies 11 (2):149–160.

Ball, L., and S. Mazumder. 2011. Inflation dynamics and the great recession. NBER Working Papers, No. 17044, May.

Bank for International Settlements. 2014. 84th Annual Report, June.

Bank for International Settlements. 2015. 85th Annual Report, June.

Bank for International Settlements. 2016. 86th Annual Report, June.

Bank for International Settlements. 2017. BIS Quarterly Review, March.

Basel Committee on Banking Supervision. 2010. An assessment of the long-term economic impact of stronger capital and liquidity requirements, July.

Bean, C., C. Broda, T. Ito, and R. Kroszner. 2015. Low for long? Causes and consequences of persistently low interest rates. Geneva Reports on the World Economy, No. 17, International Center for Monetary and Banking Studies. London: CEPR Press.

Bech, M., E. Kharroubi, and L. Gambacorta. 2014. Monetary policy in a downturn: Are financial crises special? International Finance 7(1):99–119 (Also available as BIS Working Papers, No 388).

Bernanke, B. 2005. The global saving glut and the US current account deficit. Sandridge Lecture Richmond, 10 March.

Bernanke, B. 2015. Why are interest rates so low, part 2: Secular stagnation, Brookings. https://www.brookings.edu/blog/ben-bernanke/2015/03/31/why-are-interest-rates-so-low-part-2-secular-stagnation/.

Bianchi, F., and A. Civelli. 2013. Globalization and inflation: Structural evidence from a time-varying VAR approach. Economic Research Initiatives at Duke (ERID) Working Papers, No. 157, July.

Blagrave, P., R. García-Saltos, D. Laxton, and F. Zhang. 2015. A simple multivariate filter for estimating potential output. IMF Working Papers, WP/15/79.

Blanchard, O., E. Cerutti, and L. Summers. 2015. Inflation and activity—two explorations and their monetary policy implications. NBER Working Papers, No. 21726, November.

Blanchard, O., G. Lorenzoni, and J.-P. L’Huillier. 2017. Short-run effects of lower productivity growth. A twist on the secular stagnation hypothesis. NBER Working Papers, No. 23160, February.

Bordo, M., and A. Redish. 2004. Is deflation depressing: Evidence from the Classical Gold Standard. In Deflation: Current and historical perspectives, ed. R. Burdekin, and P. Siklos. Cambridge: Cambridge University Press.

Borio, C. 2007. Monetary and prudential policies at a crossroads? New challenges in the new century. Moneda y Crédito 224: 63–101.

Borio, C. 2014a. The financial cycle and macroeconomics: What have we learnt. Journal of Banking & Finance 45: 182–198.

Borio, C. 2014b. The international monetary and financial system: Its Achilles heel and what to do about it. BIS Working Papers, No. 456, August.

Borio, C. 2014c. Monetary policy and financial stability: What role in prevention and recovery? Capitalism and Society 9(2):Article 1 (Also available as BIS Working Papers, No. 440, January 2014).

Borio, C. 2014d. Macroprudential frameworks: (too) great expectations? Central Banking Journal 25th Anniversary issue, August (Also available in BIS Speeches).

Borio, C., and P. Disyatat. 2011. Global imbalances and the financial crisis: Link or no link? BIS Working Papers, No. 346, May (Revised and extended version of 2010. Global imbalances and the financial crisis: Reassessing the role of international finance. Asian Economic Policy Review 5:198–216).

Borio, C., P. Disyatat, and M. Juselius. 2016. Rethinking potential output: Embedding information about the financial cycle. Oxford Economic Papers (Also available as BIS Working Papers, No. 404, February 2013).

Borio, C., and M. Drehmann. 2009. Assessing the risk of banking crises—revisited. BIS Quarterly Review March:29–46.

Borio, C., and A. Filardo. 2004. Looking back at the international deflation record. North American Journal of Economics and Finance 15(3):287–311.

Borio, C., and A. Filardo. 2007. Globalisation and inflation: New cross-country evidence on the global determinants of domestic inflation. BIS Working Papers, No. 227, May.

Borio, C., M. Erdem, A. Filardo, and B. Hofmann. 2015. The costs of deflations: A historical perspective. BIS Quarterly Review March:31–54.

Borio, C., C. Furfine, and P. Lowe. 2001. Procyclicality of the financial system and financial stability: Issues and policy options. In Marrying the macro- and micro-prudential dimensions of financial stability, 1–57. BIS Papers, No. 1, March.

Borio, C., E. Kharroubi, C. Upper, and F. Zampolli. 2015a. Labour reallocation and productivity dynamics: Financial causes, real consequences. BIS Working Papers, No. 534, December.

Borio, C., and P. Lowe. 2002. Asset prices, financial and monetary stability: Exploring the nexus. BIS Working Papers, No. 114, July.

Bouis, R., O. Causa, L. Demmou, R. Duval, and A. Zdzienicka. 2012. The short-term effects of structural reforms: An empirical analysis. OECD Economics Department Working Papers, No. 949, March.

Bruno, V., and H. S. Shin. 2014. Cross-border banking and global liquidity. BIS Working Papers, No. 458, September.

Cerra, V., and S. Saxena. 2008. Growth dynamics: The myth of economic recovery. American Economic Review 98 (1):439–457.

Ciccarelli, M., and B. Mojon. 2010. Global inflation. Review of Economics and Statistics 92: 524–535.

Claessens, S., M. Kose, and M. Terrones. 2011. Financial cycles: What? How? When? IMF Working Papers, WP/11/76.

Coibion, O., and Y. Gorodnichenko. 2015. Is the Phillips curve alive and well after all? Inflation expectations and the missing disinflation. American Economic Journal: Macroeconomics 7 (1):197–232.

Crockett, A. 2000. In search of anchors for financial and monetary stability. Speech at the SUERF Colloquium, Vienna, 27–29 April (available in BIS Speeches and, in extended form, with C Borio (co-author), as Greek Economic Review, vol. 20, No. 2, Autumn, pp 1–14).

De Bonis, R., and A. Silvestrini. 2014. The Italian financial cycle: 1861–2011. Cliometrica 8 (3):301–334.

Drehmann, M., C. Borio, and K. Tsatsaronis. 2011. Anchoring countercyclical capital buffers: The role of credit aggregates. International Journal of Central Banking 7 (4):189–240.

Drehmann, M., C. Borio, and K. Tsatsaronis. 2012. Characterising the financial cycle: Don’t lose sight of the medium term!. BIS Working Papers, No. 380, November.

Eichengreen, B., and K. Mitchener. 2004. The Great Depression as a credit boom gone wrong. Research in Economic History 22: 183–237.

Eichengreen, B., D. Park, and K. Shin. 2016. Deflation in Asia: Should the dangers be dismissed? ADB Economics Working Paper Series, No. 490, January.

Eickmeier, S., and K. Moll. 2009. The global dimension of inflation: Evidence from factor-augmented Phillips curves. ECB, Working Paper Series, No. 1011, February.

Einarsson, B., K. Gunnlaugsson, T. Ólafsson, and T. Pétursson. 2016. The long history of financial boom-bust cycles in Iceland. Part II: Financial cycles. Central Bank of Iceland Working Papers, No. 72.

Faust, J., and E. Leeper. 2015. The myth of normal: The bumpy story of inflation and monetary policy. Paper presented at the Federal Reserve Bank of Kansas City Economic Policy Symposium on Inflation dynamics and monetary policy, Jackson Hole, 27–29 August.

Faust, J., and J. Wright. 2013. Forecasting inflation. In Handbook of Economic Forecasting, edited by Graham Elliott, Clive Granger and A. Timmermann, vol. 2, 2–56. North-Holland: Elsevier

Fisher, I. 1933. The debt-deflation theory of great depressions. Econometrica 1(4):337–357.

Gagnon, E., K. Johannsen, and D. López-Salido. 2016. Understanding the New Normal: The role of demographics. Finance and Economics Discussion Series, No. 2016-080, Board of Governors of the Federal Reserve System.

Gordon, R. 2012. Is US economic growth over? Faltering innovation confronts the six headwinds. NBER Working Papers, No. 18315, August.

Gordon, R. 2013. The Phillips curve is alive and well: Inflation and the NAIRU during the slow recovery. NBER Working Papers, No. 19390, August.

Hofmann, B., and B. Bogdanova. 2012. Taylor rules and monetary policy: A global ‘Great Deviation’? BIS Quarterly Review September:37–49.

Ihrig, J., S. Kamin, D. Lindner, and J. Márquez. 2010. Some simple tests of the globalization and inflation hypothesis. International Finance 13: 343–375.

International Monetary Fund (IMF) (2013): “The dog that didn’t bark: has inflation been muzzled or was it just sleeping”, World Economic Outlook, April, Chapter 3.

Jordà, O., M. Schularick, and A. Taylor. 2013. When credit bites back. Journal of Money, Credit and Banking 45(2):3–28.

Juselius, M., C. Borio, P. Disyatat, and M. Drehmann. 2016. Monetary policy, the financial cycle and ultralow interest rates. BIS Working Papers, No. 569, July (Forthcoming in the International Journal of Central Banking).

Koo, R. 2003. Balance sheet recession: Japan’s struggle with uncharted economics and its global implications. Singapore: Wiley.

Laubach, T., and J. Williams. 2003. Measuring the natural rate of interest. The Review of Economics and Statistics 85(4):1063–1070.

Lodge, D., and I. Mikolajun. 2016. Advanced economy inflation: The role of global factors. ECB, Working Paper Series, No. 1948, August.

Martínez-García, E., and M. Wynne. 2012. Global slack as a determinant of US inflation. Federal Reserve Bank of Dallas, Globalization and Monetary Policy Institute Working Papers, No. 123.

McCauley, R., P. McGuire, and V. Sushko. 2015. Global dollar credit: Links to US monetary policy and leverage. Economic Policy 30(82):189–229.

Melolinna, M., and M. Tóth. 2016. Output gaps, inflation and financial cycles in the UK. Bank of England, Staff Working Papers, No. 585.

Mian, A., A. Sufi, and E. Verner. 2015. Household debt and business cycles worldwide. NBER Working Papers, No. 21581, September.

Pain, N., I. Koske, and M. Sollie. 2008. Globalisation and OECD consumer price inflation. OECD Journal: Economic Studies 1: 1–32.

Rajan, R. 2014. Competitive monetary easing: Is it yesterday once more? Washington: Brookings Institution.

Rajan, R. 2015. Panel remarks at the IMF Conference, Rethinking Macro Policy III, Washington DC, 15–16 April.

Reinhart, C., and V. Reinhart. 2010. After the fall. NBER Working Papers, No. 16334, September.

Rey, H. 2013. Dilemma not trilemma: The global financial cycle and monetary policy independence. Paper presented at the Federal Reserve Bank of Kansas City Economic Policy Symposium on Global dimensions of unconventional monetary policy, Jackson Hole, 22–24 August.

Rogoff, K. 2015. Debt supercycle, not secular stagnation. Article on VoxEU.org, 22 April. www.voxeu.org/article/debt-supercycle-not-secular-stagnation.

Rünstler, G., and M. Vlekke. 2016. Business, housing and credit cycles. ECB, Working Paper Series, No. 1915, June.

Schüler, Y., P. Hiebert, and T. Peltonen. 2015. Characterising the financial cycle: A multivariate and time-varying approach. ECB, Working Paper Series, No. 1846, September.

Selgin, G. 1997. Less than zero: The case for a falling price level in a growing economy. IEA Hobart Paper, No. 132, The Institute of Economic Affairs, April, London.

Shin, H.S. 2012. Global banking glut and loan risk premium. IMF Economic Review 60(2):155–192.

Shin, H.S. 2017. How much should we read into shifts in long-dated yields? Speech at the US Monetary Policy Forum, New York City, 3 March.

Stock, J., and M. Watson. 2007. Why has US inflation become harder to forecast? Journal of Money, Credit and Banking 39(1):3–33.

Summers, L. 2014. Reflections on the ‘New Secular Stagnation Hypothesis’. In Secular stagnation: Facts, causes and cures. VoxEU.org eBook, edited by C. Teulings and R. Baldwin. London: CEPR Press.

Summers, L. 2016. Macroeconomic policy and secular stagnation. Mundell-Fleming Lecture, at the Seventeenth Jacques Polak Annual Research Conference, Macroeconomics after the Great Recession, IMF, Washington DC, 3–4 November.

Taylor, J., and V. Wieland. 2016. Finding the equilibrium real interest rate in a fog of policy deviations. Business Economics 51(3):147–154.

Teulings, C., and R. Baldwin (eds.). 2014. Secular stagnation: facts, causes and cures, a VoxEU.org book. London: CEPR Press.

Acknowledgements

I would like to thank Raphael Auer, Piti Disyatat, Dietrich Domanski, Andy Filardo, Jonathan Kearns, Marco Lombardi, Robert McCauley, Phurichai Rungcharoenkitkul, Hyun Song Shin and Fabrizio Zampolli for helpful comments.

Author information

Authors and Affiliations

Corresponding author

Additional information

Speech delivered at the NABE Economic Policy Conference, March 7, 2017.

Electronic supplementary material

Below is the link to the electronic supplementary material.

Rights and permissions

About this article

Cite this article

Borio, C. Secular stagnation or financial cycle drag?. Bus Econ 52, 87–98 (2017). https://doi.org/10.1057/s11369-017-0035-3

Published:

Issue Date:

DOI: https://doi.org/10.1057/s11369-017-0035-3