Abstract

Dynamic factor models based on Kalman Filter techniques are frequently used to nowcast GDP. This study deals with the selection of indicators for this practice. We propose a two-tiered mechanism which is shown in a case study to produce more accurate nowcasts than a benchmark stochastic process and a standard model including extreme bounds fragile indicators. Our pseudo-ex-ante forecast nearly measures up to the genuine ex-ante forecast of the European Commission.

Similar content being viewed by others

Notes

In practice, an ADFM modifies the exact dynamic factor model by Stock and Watson (1991) to account for problems of different frequency and asynchronous publication of series underlying the real-time forecast in applying a Kalman Filter strategy to fill up the series. For a more exact distinction see, e.g., Luciani (2014). Notably, Giannone et al. (2008), technically, were the first to develop the nowcasting methodology in large scale nowcasting models.

We refer to small-scale as diffusion index forecasts (Stock and Watson 2002) based on rather small two-digit numbers sets of indicators.

If standard EBA is defined by the seminal approaches advocated in Levine and Renelt (1992), in Sala-i-Martin (1997), sometimes referred to as “modified EBA”, and in Hoover and Perez (2004, pp. 774–775), our approach is a hybrid version of all three of them. Following Levine and Renelt (1992), we consider one focus variable (in our notation c). Like Sala-i-Martin (1997) we take into account exactly (and not at most as in Levine and Renelt 1992) three “doubtful” variables in the conditioning set. And, as in Hoover and Perez (2004), we abstract from any other fixed subset of series (or, in general, variables) that we always include as covariates. However, we stick with the “strict” robustness definition of Levine and Renelt (1992) and also do not likelihood weight estimates.

It remains for future work to apply the numerical strategy used by Hoover and Perez (2004) in the cross-sectional growth regression context also in the (D)EBA time series context. Similarly, growing computational power will allow to alleviate the first caveat in our list.

See Müller and Köberl (2012) for a genuine ex-ante nowcasting experiment.

We are thankful to one of the anonymous referees to whom we owe this suggestion to referring to actual institutional forecasts as benchmark.

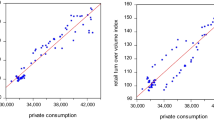

One reason for doing so is that one might be bothered that by merely dropping some indicators in the derivation of the common factor raises the weight of the stock exchange for real estate and finance index in the constitution of the factor and through this channel alone gives the (D)EBA based factor a comparative advantage. However, as can be seen from Table 2, the FE difference between the two factors remains if we leave out the recent crisis which is generally seen to be rooted in Spanish housing price dynamics. Interestingly, the FE for the model with the 14 core variables and the benchmark AR(2) process is almost the same excluding the crisis.

References

Aruoba, S., Diebold, F. X., & Scotti, C. (2009). Real-time measurement of business conditions. Journal of Business and Economic Statistics, 27, 417–427.

Breitung, J., & Eickmeier, S. (2006). Dynamic factor models. Advances in Statistical Analysis, 90, 27–42.

Camacho, M., & Doménech, R. (2012). MICA-BBVA: A factor model of economic and financial indicators for short-term GDP forecasting. Journal of the Spanish Economic Association, 3, 475–497.

Camacho, M., & Garcia-Serrador, A. (2014). The euro-STING revisited: The usefulness of financial indicators to obtain euro area GDP. Journal of Forecasting, 33, 186–197.

Camacho, M., & Perez-Quiros, G. (2010). Introducing the euro-STING: Short-term indicator of euro area growth. Journal of Applied Econometrics, 25, 663–694.

Carstensen, K., Wohlrabe, K., & Ziegler, C. (2011). Predictive ability of business cycle indicators under test. Journal of Economics and Statistics, 231, 82–106.

Castle, J. L., Fawcett, N. W. P., & Hendry, D. F. (2009). Nowcasting is not just contemporaneous forecasting. National Institute Economic Review, 210, 71–89.

Chamberlain, G., & Leamer, E. E. (1976). Matrix weighted averages and posterior bounds. Journal of the Royal Statistical Society Series B, 38, 73–84.

Chauvet, M., & Potter, S. (2013). Forecasting output. In G. Elliott & A. Timmermann (Eds.), Handbook of economic forecasting (Vol. 2A, pp. 141–194). Amsterdam: Elsevier.

Diebold, F. X., & Mariano, R. S. (1995). Comparing predictive accuracy. Journal of Business and Economic Statistics, 13, 253–265.

Doz, C., Giannone, D., & Reichlin, L. (2012). A quasi maximum likelihood approach for large approximate dynamic factor models. Review of Economics and Statistics, 94, 1014–1024.

Durlauf, S. N., Johnson, P. A., & Temple, J. R. W. (2009). The methods of growth econometrics. In T. C. Mills & K. Patterson (Eds.), Palgrave handbook of econometrics. Applied econometrics (Vol. 2, pp. 1119–1179). New York: Palgrave Macmillan.

Elliott, G., Gargano, A., & Timmermann, A. (2013). Complete subset re-gressions. Journal of Econometrics, 177, 357–373.

Fowles, R., & Loeb, P. D. (1995). Effects of policy-related variables on traffic fatalities: An extreme bounds analysis using time-series data. Southern Economic Journal, 62, 359–366.

Gassebner, M., Gutmann, J., & Voigt, S. (2016). When to expect a coup d’ état? An extreme bounds analysis of coup determinants. Public Choice, 169, 293–313.

Giannone, D., Reichlin, L., & Small, D. (2008). Nowcasting: The real-time informational content of macroeconomic data. Journal of Monetary Economics, 55, 665–676.

Harvey, D. I., Leybourne, S. J., & Newbold, P. (1997). Testing the equality of prediction mean square errors. International Journal of Forecasting, 13, 281–291.

Hoover, K. D., & Perez, S. J. (2004). Truth and robustness in cross-country growth regressions. Oxford Bulletin of Economics and Statistics, 66, 765–798.

Leamer, E. E. (1982). Sets of posterior means with bounded variance priors. Econometrica, 50, 725–736.

Leamer, E. E. (1983). Let’s take the con out of econometrics. American Economic Review, 73, 31–43.

Levine, R., & Renelt, D. (1992). A sensitivity analysis of cross-country growth regressions. American Economic Review, 82, 942–963.

Luciani, M. (2014). Forecasting with approximate dynamic factor models: The role of non-pervasive shocks. International Journal of Forecasting, 30, 20–29.

Müller, C., & Köberl, E. (2012). Catching a floating treasure: A genuine ex-ante forecasting experiment in real time. KOF Working Papers 12-297, KOF Swiss Economic Institute, ETH Zurich.

Moosa, I. A. (2009). The determinants of foreign direct investment in MENA countries: An extreme bounds analysis. Applied Economics Letters, 16, 1559–1563.

Sala-i-Martin, X. X. (1997). I have just run two million regressions. American Economic Review, 87, 178–183.

Stock, J., & Watson, M. (1991). A probability model of the coincident economic indicators. In K. Lahiri & G. Moore (Eds.), Leading economic indicators: New approaches and forecasting records (pp. 63–89). Cambridge: Cambridge University Press.

Stock, J., & Watson, M. (2002). Macroeconomic forecasting using diffusion indexes. Journal of Business and Economic Statistics, 20, 147–162.

Sturm, J.-E., Berger, H., & De Haan, J. (2005). Which variables explain decision on IMF credits? An extreme bounds analysis, Economics and Politics, 17, 177–213.

Author information

Authors and Affiliations

Corresponding author

Additional information

We thank the editor, Michael Graff, two anonymous referees, Katja Heinisch, Esther Ruiz, Domenico Giannone, Massimiliano Marcellino, Rolf Scheufele, Christian Schuhmacher, and participants of seminars at the University of Leipzig, the IWH-CIREQ Macroeconometric Workshop on Forecasting and Big Data, and the IWH-IEW Workshop on Nowcasting and Forecasting for many comments and suggestions that markedly improved our paper.

Rights and permissions

About this article

Cite this article

Duarte, P., Süssmuth, B. Implementing an Approximate Dynamic Factor Model to Nowcast GDP Using Sensitivity Analysis. J Bus Cycle Res 14, 127–141 (2018). https://doi.org/10.1007/s41549-018-0026-0

Received:

Accepted:

Published:

Issue Date:

DOI: https://doi.org/10.1007/s41549-018-0026-0