Abstract

The analysis of time-varying correlation between stock prices and exchange rates in the context of international investments has been well researched in the literature in last few years. In this paper, we study the interdependence of exchange rates and stock prices for seven countries (Canada, Japan, Denmark, Hong Kong, Singapore, Mexico and Brazil). To do so, we both use the DCC-FIEGARCH and FIAPARCH-DCC models during the period spanning from January 1, 2000 until January 1, 2016. The empirical results suggest asymmetric responses in stock prices-exchange rates linkages, a high persistence of the conditional correlation. They also show bidirectional spillovers effects between different series. Moreover, the results indicate different behavior of exchange rates-stock prices nexus during the crisis periods, suggesting the need for specific policy measures. Finally, our findings offer investors, portfolios managers and policymakers insights on international portfolios and monetary.

Similar content being viewed by others

Notes

The use of such frequency allows to better analyze the statistical propriety of the long memory volatility. Weekly data do not permit to study the relationships between stock prices and exchange rates given that they do not take into account efficiently long memory while monthly data may be insufficient to track short-term developments.

References

Abed R, Maktouf S (2016) Long memory and asymmetric effects between exchange rates and stock returns. Adv Manag Appl Econ 5:45–78

Abraham A, Seyyed J (2006) Information transmission between the Gulf equity markets of Saudi Arabia and Bahrain. Res Int Bus Finance 20:276–285

Afshan S, Sharif A, Loganathan N, Jammazi R (2018) Time-frequency causality between stock prices and exchange rates: further evidences from cointegration and wavelet analysis. Phys A Stat Mech Appl 495:225–244

Alagidede P, Panagiotidis T, Zhang X (2011) Causal relationship between stock prices and exchange rates. J Int Trade Econ Dev 20(1):67–86

Anshul J, Biswal C (2016) Dynamic linkages among oil price, gold price, exchange rate, and stock market in India. Res Pol 49:179–185

Attari J, Safdar L (2013) The relationship between macroeconomic volatility and the stock market volatility: empirical evidence from Pakistan. Pak J Commer Soc Sci 7(2):309–320

Bahmani-Oskooee M, Saha S (2016) Do exchange rate changes have symmetric or asymmetric effects on stock prices? Glob Finance J 31:57–72

Bashir U, Yu Y, Hussain M, Zebende F (2016) Do foreign exchange and equity markets co-move in Latin American region? Detrended cross-correlation approach. Phy A Stat Mech Appl 462:889–897

Boero G, Silvapulle P, Tursunalieva A (2011) A. Modelling the bivariate dependence structure of exchange rates before and after the introduction of the euro: a semiparametric approach. Int J Finance Econ 16:357–374

Bollerslev T, Mikkelsen O (1996) Modelling and Pricing Long Memory in Stock Market Volatility. J Econ 73:151–184

Chkili W, Aloui C, Nguyen K (2011) Asymmetric effects and long memory in dynamic volatility relationships between stock returns and exchange rates. J Int Finance Mark 22:738–757

Conrad C, Karanasos M, Zeng N (2011) Multivariate fractionally integrated APARCH modeling of stock market volatility: a multi-country study. J Empir Finance 18:147–159

Dahir et al (2018) Revisiting the dynamic relationship between exchange rates and stock prices in BRICS countries: a wavelet analysis. Borsa Istanb Rev 18(2):101–113

Dimitriou D, Kenourgios D (2013) Financial crises and dynamic linkages among international currencies. J Inter Fin Mark 26:319–332

Engle R, Ito T, Lin W (1990) Meteor showers or heat waves? Heteroskedastic intra-daily volatility in the foreign exchange market. Econmics 58:525–542

Engle R, Ng K (1993) Measuring and testing the impact of news on volatility. J Finance 48:1749–1778

Engle R (2002) Dynamic conditional correlation: A simple class of multivariate generalized autoregressive conditional heteroskedasticity models. J Bus Econ Stat 20:339–350

Geweke J, Porter-Hudak S (1983) The estimation and application of long memory time series models. J Time Ser Anal 4:221–238

Giovannini et al (2006) Modeling and forecasting cointegrated relationships among heavy oil and product prices. Energ Econ 27:831–848

Guima R, Hong GF (2016) Dynamic Connectedness of Asian Equity Markets. Bor Istanb Rev 17:25–48

Hosking M (1980) The multivariate portmanteau statistic. J Am Stat Assoc 75:602–608

Kang S, Cheong C, Yoon S (2010) Long memory volatility in Chinese stock markets. Phys A 389:1425–1433

Kasman A, Kasman S, Torun E (2009) Dual long-memory property in returns and volatility: evidence from the CEE countries stock markets. Emerg Mark Rev 10:122–139

Kenourgios D, Samitas A, Paltalidis N (2011) Financial crises and stock market contagion in a multivariate time-varying asymmetric framework. J Int Finance Mark Inst Mon 21:92–106

Kitamura Y (2010) Testing for intraday interdependence and volatility spillover among the euro, the pound and Swiss franc markets. Res Int Bus Finance 24:158–270

Koutmos G et al (1995) Asymmetric volatility transmission in international stock markets. J Int Money Finance 14:747–762

Lean H, Teng K (2013) Integration of world leaders and emerging powers into the Malaysian stock market: a DCC-MGARCH approach. Econ Model 32:333–342

Lee J, Strazicich MC (2004) Minimum LM unit root test with one structural break. Int J Finance Econ 6:4–17

Leung H, Schiereck D, Schroeder F (2017) Volatility spillovers and determinants of contagion: Exchange rate and equity markets during crises. Econ Model 61:169–180

Lin H (2012) The comovement between exchange rates and stock prices in the Asian emerging markets. Int Rev Econ Finance 22(1):161–172

Lin W, Engle R, Ito T (1994) Do bulls and bears move across borders? International transmission of stock returns and volatility. Rev Financ Stud 7:507–538

Li W, McLeod A (1981) Distribution of the residual autocorrelations in multivariate ARMA time series models. J R Stat Soc 43:231–239

Lopes H (2002) Sequential analysis of stochastic volatility models: Some econometric applications. Phys Rev 47:777–780

McLeod I, Li K (1983) Diagnostic checking ARMA time series models using squared residual autocorrelations. J Time Ser Anal 4:269–273

Melvin T, Melvin B (2003) The global transmission of voltility in the foreign exchange market. Rev Econ Stat 85:670–679

Mitra R (2017) Stock market and foreign exchange market integration in South Africa. World Dev Perspect 6:32–34

Pan S, Fok R, Liu Y (2007) Dynamic linkages between exchange rates and stock prices: evidence from East Asian markets. Int Rev Econ Finance 16:503–520

Pan Y, Liu S, Tse D (1999) The impact of order and mode of market entry on profitability and market share. J Int Bus Stud 30:81–114

Tsai C (2012) The relationship between stock price index and exchange rate in Asian markets: A quantile regression approach. J Inter Fin Mark, instit Money 50:609–621

Tse K, Tsui A (2002) A multivariate GARCH model with time-varying correlations. J Bus Econ Stat 20:351–362

Tule M et al (2018) Volatility of stock market returns and the naira exchange rate. Glob Financ J 35:97–105

Ülkü N, Demirci E (2012) Joint dynamics of foreign exchange and stock markets in emerging Europe. J Int Finance Mark Inst Money 22(1):55–86

Weber E, Zhang Y (2012) Common influences, spillover and integration in Chinese stock markets. J Empir Finance 19:382–394

Xie Z, Chen S, Wu A (2020) The foreign exchange and stock market nexus: new international evidence. Int Rev Econ Finance 67:240–266

Yang S, Doong S (2004) Price and volatility spillovers between stock prices and exchange rates: empirical evidence from the G-7 countries. Int J Bus Econ 3:139–153

Zhao H (2010) Dynamic relationship between exchange rate and stock price: evidence from China. Res Int Bus Finance 24(2):103–112

Author information

Authors and Affiliations

Corresponding author

Additional information

Publisher's Note

Springer Nature remains neutral with regard to jurisdictional claims in published maps and institutional affiliations.

Appendices

Appendix 1

Appendix 2

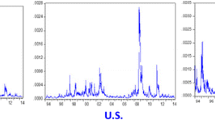

See Figs. 3, 4, 5, 6, 7, 8 and 9.

Dynamic behavior of conditional correlation between exchange rate and index prices for Brazil

Dynamic behavior of conditional correlation between exchange rate and index prices for Canada

Dynamic behavior of conditional correlation between exchange rate and index prices for Singapore

Dynamic behavior of conditional correlation between exchange rate and index prices for Japan

Dynamic behavior of conditional correlation between exchange rate and index prices for Mexico

Dynamic behavior of conditional correlation between exchange rate and index prices for Hong Kong

Dynamic behavior of conditional correlation between exchange rate and index prices for Danemark

Rights and permissions

About this article

Cite this article

Moussa, W., Bejaoui, A. & Mgadmi, N. Asymmetric Effect and Dynamic Relationships Between Stock Prices and Exchange Rates Volatility. Ann. Data. Sci. 8, 837–859 (2021). https://doi.org/10.1007/s40745-020-00295-9

Received:

Revised:

Accepted:

Published:

Issue Date:

DOI: https://doi.org/10.1007/s40745-020-00295-9