Abstract

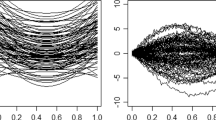

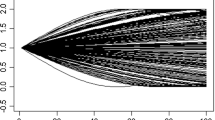

A linear multiple regression model in function spaces is formulated, under temporal correlated errors. This formulation involves kernel regressors. A generalized least-squared regression parameter estimator is derived. Its asymptotic normality and strong consistency is obtained, under suitable conditions. The correlation analysis is based on a componentwise estimator of the residual autocorrelation operator. When the dependence structure of the functional error term is unknown, a plug-in generalized least-squared regression parameter estimator is formulated. Its strong consistency is proved as well. A simulation study is undertaken to illustrate the performance of the presented approach, under different regularity conditions. An application to financial panel data is also considered.

Similar content being viewed by others

References

Aneiros-Pérez G, Vieu P (2006) Semi-functional partial linear regression. Stat Probab Lett 76:1102–1110

Aneiros-Pérez G, Vieu P (2008) Nonparametric time series prediction: a semi-functional partial linear modeling. J Multivar Anal 99:834–857

Benhenni K, Hedli-Griche S, Rachdi M (2017) Regression models with correlated errors based on functional random design. Test 26:1–21

Bosq D (2000) Linear processes in function spaces. Springer, New York

Bosq D, Ruiz-Medina MD (2014) Bayesian estimation in a high dimensional parameter framework. Electron J Stat 8:1604–1640

Cáceres MD, Legendre P (2008) Beals smoothing revisited. Oecologia 156:657–669

Cai T, Hall P (2006) Prediction in functional linear regression. Ann Stat 34:2159–2179

Chaouch M, Laib N, Louani D (2017) Rate of uniform consistency for a class of mode regression on functional stationary ergodic data. Stat Methods Appl 26:19–47

Chiou J, Múller HG, Wang JL (2004) Functional response models. Stat Sin 14:659–677

Crambes C, Kneip A, Sarda P (2009) Smoothing splines estimators for functional linear regression. Ann Stat 37:35–72

Cuevas A (2014) A partial overview of the theory of statistics with functional data. J Stat Plan Inference 147:1–23

Cuevas A, Febrero M, Fraiman R (2002) Linear functional regression: the case of a fixed design and functional response. Can J Stat 30:285–300

Da Prato G, Zabczyk J (2002) Second order partial differential equations in Hilbert spaces. Cambridge University Press, Cambridge

Dautray R, Lions JL (1985) Mathematical analysis and numerical methods for science and technology, vol 3. Spectral theory and applications. Springer, New York

Espejo RM, Fernández-Pascual R, Ruiz-Medina MD (2017) Spatial-depth functional estimation of ocean temperature from non-separable covariance models. Stoch Environ Res Risk Assess 31:39–51

Febrero-Bande M, Galeano P, Gonzalez-Manteiga W (2015) Functional principal component regression and functional partial least-squares regression: an overview and a comparative study. Int Stat Rev. https://doi.org/10.1111/insr.12116

Ferraty F, Vieu P (2006) Nonparametric functional data analysis: theory and practice. Springer, New York

Ferraty F, Vieu P (2011) Kernel regression estimation for functional data. In: Ferraty F, Romain Y (eds) The Oxford handbook of functional data analysis. Oxford University Press, Oxford, pp 72–129

Ferraty F, Goia A, Vieu P (2002) Functional nonparametric model for time series: a fractal approach for dimension reduction. Test 11:317–344

Ferraty F, Keilegom IV, Vieu P (2012) Regression when both response and predictor are functions. J Multivar Anal 109:10–28

Ferraty F, Goia A, Salinelli E, Vieu P (2013) Functional projection pursuit regression. Test 22:293–320

Fitzmaurice GM, Laird NM, Ware JH (2004) Applied longitudinal analysis. Wiley, New York

Geenens G (2011) Curse of dimensionality and related issues in nonparametric functional regression. Stat Surv 5:30–43

Goia A, Vieu P (2015) A partitioned single functional index model. Comput Stat 30:673–692

Goia A, Vieu P (2016) An introduction to recent advances in high/infinite dimensional statistics. J Multivar Anal 146:1–6

Guillas S (2001) Rates of convergence of autocorrelation estimates for autoregressive Hilbertian processes. Stat Probab Lett 55:281–291

Horváth L, Kokoszka P (2012) Inference for functional data with applications. Springer, New York

Hsing T, Eubank R (2015) Theoretical foundations of functional data analysis, with an introduction to linear operators. In: Wiley series in probability and statistics. Wiley, Chichester

Kara LZ, Laksaci A, Rachdi M, Vieu P (2017a) Uniform in bandwidth consistency for various kernel estimators involving functional data. J Nonparametric Stat 29:85–107

Kara LZ, Laksaci A, Rachdi M, Vieu P (2017b) Data-driven kNN estimation in nonparametric functional data analysis. J Multivar Anal 153:176–188

Ling N, Liu Y, Vieu P (2017) On asymptotic properties of functional conditional mode estimation with both stationary ergodic and responses MAR. In: Aneiros G, Bongiorno EG, Cao R, Vieu P (eds) Functional statistics and related fields. Springer, Switzerland, pp 173–178

Marx BD, Eilers PH (1999) Generalized linear regression on sampled signals and curves: a P-spline approach. Technometrics 41:1–13

Mas A (2004) Consistance du prédicteur dans le modèle ARH(1): le cas compact. Ann ISUP 48:39–48

Mas A (2007) Weak-convergence in the functional autoregressive model. J Multivar Anal 98:1231–1261

Morris JS (2015) Functional regression. Ann Rev Stat Its Appl 2:321–359

Ramsay JO, Silverman BW (2005) Functional data analysis, 2nd edn. Springer Series in Statistics. Springer, New York

Ruiz-Medina MD (2011) Spatial autoregressive and moving average Hilbertian processes. J Multivar Anal 102:292–305

Ruiz-Medina MD (2012a) New challenges in spatial and spatiotemporal functional statistics for high-dimensional data. Spat Stat 1:82–91

Ruiz-Medina MD (2012b) Spatial functional prediction from spatial autoregressive Hilbertian processes. Environmetrics 23:119–128

Ruiz-Medina MD (2016) Functional analysis of variance for Hilbert-valued multivariate fixed effect models. Statistics 50:689–715

Acknowledgements

This work has been supported in part by project MTM2015-71839-P of MINECO, Sapin (co-funded with FEDER funds). D. Miranda supported by FINCyT, Innóvate Perú.

Author information

Authors and Affiliations

Corresponding author

Electronic supplementary material

Below is the link to the electronic supplementary material.

Rights and permissions

About this article

Cite this article

Ruiz-Medina, M.D., Miranda, D. & Espejo, R.M. Dynamical multiple regression in function spaces, under kernel regressors, with ARH(1) errors. TEST 28, 943–968 (2019). https://doi.org/10.1007/s11749-018-0614-2

Received:

Accepted:

Published:

Issue Date:

DOI: https://doi.org/10.1007/s11749-018-0614-2

Keywords

- ARH(1) errors

- Dynamical functional multiple regression

- Firm leverage maps

- Generalized least-squared estimator

- Kernel regressors