Abstract

We propose a general framework for estimating the vulnerability to default by a central counterparty (CCP) in the credit default swaps market. Unlike conventional stress testing approaches, which estimate the ability of a CCP to withstand nonpayment by its two largest counterparties, we study the direct and indirect effects of nonpayment by members and/or their clients through the full network of exposures. We illustrate the approach for the U.S. credit default swaps market under shocks that are similar in magnitude to the Federal Reserve’s stress tests. The analysis indicates that conventional stress testing approaches may underestimate the potential vulnerability of the main CCP for this market.

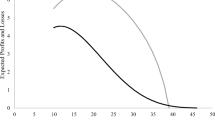

Source: Authors’ calculations, which use data provided by Markit Group Ltd.

Source: Authors’ analysis

Source: Authors’ calculations which use data provided to the OFR by The Depository Trust & Clearing Corporation and Markit Group Ltd.

Source: Authors’ calculations, which use data provided to the OFR by The Depository Trust & Clearing Corporation and Markit Group Ltd.

Source: Authors’ calculations, which use data provided to the OFR by The Depository Trust & Clearing Corporation and Markit Group Ltd.

Similar content being viewed by others

Notes

Poce et al. [27] study the Italian fixed income market instead of the derivatives market. They apply an exogenous shock to firms’ equity, estimate the impact on the assets of their counterparties using a Merton model, and then examine the impact on the CCP for the market in Italian government bonds (Cassa di Compensazione e Garanzia). Unlike the present study they do not have direct knowledge of firms’ network exposures, but must impute them. As in our study, however, they find that network contagion effects are substantial and imply a greater risk of CCP default than does the conventional Cover-2 standard.

The only other CCP in this market is CME Clearing, which in 2014 cleared less than 3% of the contracts and has since announced its exit from the market.

For more detail on the methodology underpinning these computations see [25].

This approach is consistent with CFTC Regulation 39.33(a) on the implementation of the Cover-2 standard, which assumes that the two largest BHCs default.

A similar model is used in Paddrik et al. [25] to analyze the extent to which the CCP contributes to network contagion.

In general, \(x \wedge y\) denotes the minimum of two real numbers x and y, and \([x]_+\) denotes the non-negative part of x.

Alternatively we could estimate the average transmission factor by the expression \((1/n) \sum _{i=0}^{n} (\bar{p}_i - p^*_i)/ s^*_i\). It can be shown that this yields a value at least as large as \(\tau ^*\) in (17).

We always assume that the CCP engages in variation margin gains haircutting (i.e., soft default) even when all other firms engage in hard default, due to the CCP’s contractual obligations to its members. Although \(\tilde{\Phi }(p)\) is not continuous in p, it is upper semicontinous and monotone decreasing in p, hence it has a greatest fixed point (see [25] for details).

In fact the U.S. authorities did not allow more than two large institutions (Lehman and Bear Stearns) to default during the recent financial crisis. The market implied default rates during the crisis also assigned a very low probability to four or more defaults [19].

References

Barker, R., Dickinson, A., Lipton, A., Virmani, R.: Systemic risks in CCP networks. arXiv preprint arXiv:1604.00254 (2016)

BCBS and IOSCO: Margin requirements for non-centrally-cleared derivatives. Technical Report, BIS and OICU-IOSCO, Basil, Switzerland (2015)

Calomiris, C.W.: The subprime turmoil: What’s old, what’s new, and what’s next. J. Struct. Finance 15(1), 6–52 (2009)

Campbell, S.D., Ivanov, I.: Empirically evaluating systemic risks in CCPs: the case of two CDS CCPs. SSRN: https://ssrn.com/abstract=2841076 (2016)

CFTC: Supervisory stress test of clearinghouses. A report by staff of the U.S. Commodity Futures Trading Commission, Washington, D.C. (2016)

Cont, R.: Credit default swaps and financial stability. Financ. Stab. Rev. 14, 35–43 (2010)

Cont, R., Kokholm, T.: Central clearing of OTC derivatives: bilateral vs multilateral netting. Stat. Risk Model. 31(1), 3–22 (2014)

Cont, R., Minca, A.: Credit default swaps and systemic risk. Ann. Oper. Res. 247(2), 523–547 (2016)

Cumming, F., Noss, J.: Assessing the adequacy of CCPs’ default resources. Bank of England Financial Stability Paper No. 26. (2013). https://ssrn.com/abstract=2363393

Domanski, D., Gambacorta, L., Picillo, C.: Central clearing: trends and current issues. BIS Q. Rev (2015). https://ssrn.com/abstract=2700257

Duffie, D., Scheicher, M., Vuillemey, G.: Central clearing and collateral demand. J. Financ. Econ. 116(2), 237–256 (2015)

Eisenberg, L., Noe, T.: Systemic risk in financial systems. Manag. Sci. 47(2), 236–249 (2001)

Evanoff, D.D., Russo, D., Steigerwald, R., et al.: Policymakers, researchers, and practitioners discuss the role of central counterparties. Econ. Perspect. Q IV, 2–21 (2006)

France, V.G., Kahn, C.M.: Law as a constraint on bailouts: emergency support for central counterparties. J. Financ. Intermediation 28, 22–31 (2016)

FRB: Stress tests and capital planning: comprehensive capital analysis and review. Technical Report, Board of Governors of the Federal Reserve System (2016)

Garratt, R., Zimmerman, P.: Does central clearing reduce counterparty risk in realistic financial networks? Staff Report. Federal Reserve Bank of New York 717 (2015)

Garratt, R., Zimmerman, P.: Centralized netting in financial networks. J. Bank. Finance (2017). https://doi.org/10.1016/j.jbankfin.2017.12.008

Ghamami, S., Glasserman, P.: Does OTC derivatives reform incentivize central clearing? J. Financ. Intermediation 32, 76–87 (2017)

Giglio, S.: Credit default swap spreads and systemic financial risk. In: Proceedings, Federal Reserve Bank of Chicago, vol. 10(9), pp. 104–141 (2011)

Glasserman, P., Young, H.P.: How likely is contagion in financial networks? J. Bank. Finance 50, 383–399 (2015)

Heath, A., Kelly, G., Manning, M.: Central counterparty loss allocation and transmission of financial stress. Reserve Bank of Australia Research Discussion Paper 2015-02 (2015)

Heath, A., Kelly, G., Manning, M., Markose, S., Shaghaghi, A.R.: CCPs and network stability in OTC derivatives markets. J. Financ. Stab. 27, 217–233 (2016)

Luo, L.S.: Bootstrapping default probability curves. J. Credit Risk 1(4), 169–179 (2005)

Nahai-Williamson, P., Ota, T., Vital, M., Wetherilt, A.: Central counterparties and their financial resources—a numerical approach. Bank of England Financial Stability Paper 19 (2013)

Paddrik, M., Rajan, S., Young, H.P.: Contagion in derivatives markets. Manag. Sci. (forthcoming) (2019)

Pirrong, C.: A bill of goods: central counterparties and systemic risk. J. Financ. Mark. Infrastruct. 2(4), 55–85 (2014)

Poce, G., Cimini, G., Gabrielli, A., Zaccaria, A., Baldacci, G., Polito, M., Rizzo, M., Sabatini, S.: What do central counterparties default funds really cover? A network-based stress test answer. arXiv preprint arXiv:1611.03782 (2016)

Powell, J.H.: A financial system perspective on central clearing of derivatives. In: The New International Financial System: Analyzing the Cumulative Impact of Regulatory Reform, pp. 47–59. World Scientific (2016)

Tarski, A.: A lattice-theoretical fixpoint theorem and its applications. Pac. J. Math. 5(2), 285–309 (1955)

Zigrand, J.-P.: What do network theory and endogenous risk theory have to say about the effects of central counterparties on systemic stability? Financ. Stab. Rev. 14, 153–158 (2010)

Author information

Authors and Affiliations

Corresponding author

Additional information

Publisher's Note

Springer Nature remains neutral with regard to jurisdictional claims in published maps and institutional affiliations.

We thank Randall Dodd, Marco Espinosa, Samim Ghamami, Dasol Kim, Bruce Tuckman, Stathis Tompaidis, Julie Vorman, and Bob Wasserman for their valuable comments. Additionally we would like to thank OFR’s ETL, Applications Development, Data Services, Legal, and Systems Engineering teams for collecting and organizing the data necessary to make this project possible. Views and opinions expressed are those of the authors and do not necessarily represent official positions or policy of the OFR or the U.S. Department of the Treasury.

Rights and permissions

About this article

Cite this article

Paddrik, M., Young, H.P. How safe are central counterparties in credit default swap markets?. Math Finan Econ 15, 41–57 (2021). https://doi.org/10.1007/s11579-019-00243-z

Received:

Accepted:

Published:

Issue Date:

DOI: https://doi.org/10.1007/s11579-019-00243-z