Abstract

The average return on long-term bonds exceeds the return on short-term bills by a large amount over short investment horizons. A riding-the-yield-curve investment strategy takes advantage of the higher returns on longer term bonds. This strategy involves the purchase of bonds with maturities longer than the investment horizon and the sale of these bonds, before they mature, at the end of the investment horizon. Most of the literature that evaluates this strategy compares only ex post average returns or Sharpe ratios. In this paper, we use spanning tests to provide formal statistical evidence on the benefits of investing in long bonds when the investment horizon is short. The results for both the United States and Canada indicate that an investor with a short horizon is better off investing in short-term debt instruments than long-term bonds.

Similar content being viewed by others

Notes

Bolder et al. (2004) produce a similar table for an investment horizon of 180 days.

An alternative strategy which also exploits the upward slope in the yield curve is a bond ladder. This involves holding a balanced portfolio of bond maturities at all times. A portion of investments are redeemed each period and the proceeds re-invested to maintain the maturity structure of the ladder. This strategy takes advantage of the upward sloping yield curve, while minimizing liquidity risk (Siegel 2008). The key difference between a bond ladder and riding-the-yield-curve is that, with a bond ladder, bonds are held to maturity, while the riding strategy involves selling bonds before maturity. A key shortcoming of a laddering strategy, relative to riding-the-yield-curve, is that it assumes that only a fraction of resources are likely to be needed at short notice. While a bond ladder may be a useful strategy for cash managers who plan to rollover funds, it is not a useful strategy for investors who have a fixed amount of cash to invest for a short period.

A riding-the-yield-curve investment strategy can only yield excess returns if the simple version of the expectations hypothesis does not hold. Bieri and Chincarini (2005) note that, while still controversial, numerous studies have rejected the expectations hypothesis, so there may be an opportunity for riding-the-yield-curve to increase returns. See In and Batten (2005) for a recent study in which the expectations hypothesis cannot be rejected.

Other types of comparisons are also made. Grieves and Marcus (1992) examine whether a riding strategy can stochastically dominate a buy-and-hold strategy. Grieves et al. (1999) calculate the coefficient of relative risk aversion for which an investor would not benefit from riding. Ang et al. (1998) extend Grieves and Marcus (1992) by calculating coefficients of variation of returns as well as measures of first- and second-order stochastic dominance.

Dyl and Joehnk (1981), Ang et al. (1998) and Chua et al. (2005) provide evidence both in support of and against riding. Pelaez (1997) and Bieri and Chincarini (2005) conclude that the increase in risk from riding outweighs the benefit, while the results in Grieves and Marcus (1992), Grieves et al. (1999) and Mercer et al. (2009) tend to support a riding strategy.

For example, Grieves and Marcus (1992) and Grieves et al. (1999) consider only investments in 6-, 9- and 12-month bills. Ang et al. (1998) use a 3-month horizon and consider investments in a six-month bill or a 1-year horizon and a 2-year bond. Dyl and Joehnk (1981) analyze investments only in bills of maturities of less than 26 weeks, while Mercer et al. (2009) consider only 91 and 182-day Treasury bills. Pelaez (1997) considers only investments in a two-year bond, Pilotte and Sterbenz (2006) and Chua et al. (2005) analyze investments in a five-year bond. Bieri and Chincarini (2005) considers the broadest set of maturities—6, 9 months, 1, 2, 5, 7 and 10 years.

Petrella (2005) looks at small, medium and large cap stocks and finds some benefit to size diversification even when returns are highly correlated.

A well-understood approach to conditional spanning is to augment the investment opportunities set in the unconditional case with scaled returns as proposed in Bekaert and Urias (1996). A scaled return is the payoff of a portfolio that is managed on the basis of the realizations of selected indicators. Ferson and Siegel (2001, 2009) generalized the use of scaled returns by identifying an efficient use of conditioning information. As tests for spanning are linked to the estimation of the volatility bound on the stochastic discount factor, the literature that analyzes the role of conditioning information is large (see, for example, DeRoon and Nijman (2001) and Bekaert and Liu (2004)).

It is important to use Treasury bills and bonds only as Reilly et al. (2010) find significant differences across bonds with different ratings. Use of bonds with variable ratings could confuse a rating effect with the riding-the-yield curve effect.

An outlier is defined as an observation that is more than 2.5 standard deviations away from the mean. The standard deviations of US and Canadian excess bond returns are large. For example, for the US, the average one month holding period excess return is a mere 19.4 percent of the corresponding standard deviation. For Canada, it is only 13.3 percent. As the standard deviations of US and Canadian bond returns are large, the outlier definition used here eliminates few observations. The exact percentage of outliers deleted from the sample in each case is reported in the tables of results and is generally below 5 percent of the available observations.

With overlapping investment horizons, since neighboring observations rely, to some extent, on common information, the regression errors in the spanning test equation may be correlated across time, which violates the standard independence assumption underlying the test. This does not occur with non-overlapping observations. Bremer et al. (2011) also note that overlapping horizons can bias test results. The disadvantage of utilizing non-overlapping observations is that the parameters and test statistics are estimated with a smaller number of observations than if the observations are allowed to overlap. None of the conclusions change if we use overlapping observations rather than non-overlapping observations. (The results with overlapping observations are available by request from the authors.) Some riding-the-yield-curve studies, such as Grieves and Marcus (1992), also do not use overlapping observations, but many studies, particularly those with longer investment horizons, employ samples with overlapping observations (for example, Grieves et al. (1999), Ang et al. (1998), Bolder et al. (2004), and Bieri and Chincarini (2005)).

Estimation of the multivariate regression is undertaken using an exactly identified two-step Generalized Method of Moments methodology that incorporates the Newey-West spectral matrix with T1/3 lags.

We use semi-parametric bootstrapping techniques as described in Davidson and MacKinnon (2004, Sect. 4.6).

For consistency with the previous section, we present two equally-weighted (EW) portfolios of short-term debt instruments for the one-month investment horizon. The first EW portfolio includes the returns of the 3, 6-month and 1-year Treasury bills, while the second EW portfolio excludes the 3-month bill.

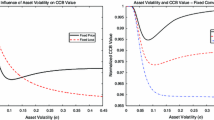

The expanded frontiers (the dotted lines) in Fig. 1a and b are associated with the same set of long and short-term maturities. Nevertheless, these lines differ to a small extent because the alternative portfolio in each case is an equally-weighted portfolio of the alternative assets, rather than an unconstrained portfolio. The imposition of the equal weights constraint for the two alternative portfolios, which is necessitated by the multicollinearity of returns, causes the small difference in the dotted lines. The dotted lines look more different in these figures than they actually are because the scales on the vertical and horizontal axes of the two figures are different.

To investigate whether the lack of diversification gains offered by a portfolio of longer maturity bonds is robust for different sample sub-periods, the tests for spanning and equality of the Sharpe ratios were re-evaluated for all possible rolling windows of 10 years in length, spaced 1 month apart, for both the US and Canada. The results of these tests are almost always consistent with the results for the whole sample reported in the tables.

References

Ang S, Alles L, Allen D (1998) Riding the yield curve: an analysis of international evidence. J Fixed Income 8(3):57–74

Bekaert G, Liu J (2004) Conditioning information and variance bounds on pricing kernels. Rev Financial Stud 17(2):339–378

Bekaert G, Urias MS (1996) Diversification, integration and emerging market closed-end funds. J Finance 51(3):835–869

Bieri DS, Chincarini LB (2005) Riding the yield curve: a variety of strategies. J Fixed Income 15(2):6–35

Bolder DJ, Johnson G, Metzler A (2004) An empirical analysis of the Canadian term structure of zero-coupon interest rates. Bank of Canada. Working Paper 2004-48

Bremer R, Buchanan BG, English PC II (2011) The advantages of using quarterly returns for long-term event studies. Rev Quant Finance Acc 36:491–516

Chua CT, Koh WTH, Ramaswamy K (2005) Comparing returns of US treasuries versus equities: implications for market and portfolio efficiency. Appl Financial Econ 15:1213–1218

Davidson R, MacKinnon JG (2004) Econometric theory and methods. Oxford University, Oxford

DeRoon FA, Nijman TE (2001) Testing for mean-variance spanning: a survey. J Empir Finance 8:111–155

DeRoon FA, Nijman TE, Werker BJM (2001) Testing for mean-variance spanning with short sales constraints and transactions costs: the case of emerging markets. J Finance 56(2):721–742

Dyl EA, Joehnk MD (1981) Riding the yield curve: does it work? J Portfol Manage 7(3):13–17

Errunza V, Hogan K, Hung MW (1999) Can the gains from international diversification be achieved without trading abroad? J Finance 54(6):2075–2107

Eun CS, Huang W, Lai S (2008) International diversification with large-and small-cap stocks. J Financial Quant Anal 43:489–524

Ferson WE, Siegel AF (2001) The efficient use of conditioning information in portfolios. J Finance 56(3):967–982

Ferson WE, Siegel AF (2009) Testing portfolio efficiency with conditioning information. The Rev Financial Stud 22(7):2535–2558

Galvani V, Plourde A (2010) Portfolio diversification in energy markets. Energy Econ 32(2):257–268

Grieves R, Marcus AJ (1992) Riding the yield curve: reprise. J Portfol Manage 18(4):67–76

Grieves R, Mann SV, Marcus AJ, Ramanlal P (1999) Riding the bill curve. J Portfol Manage 25(3):74–82

Huberman G, Kandel S (1987) Mean-variance spanning. J Finance 42(4):873–888

In F, Batten JA (2005) Expectations and equilibrium in high-grade Australian bond markets. Rev Pac Basin Financial Mark Policies 8(4):573–592

Jobson JD, Korkie B (1982) Potential performance and tests of portfolio efficiency. J Financial Econ 10:433–466

Jobson JD, Korkie B (1984) On the Jensen measure and marginal improvements in portfolio performance: a note. J Finance 39(1):245–251

Jobson JD, Korkie B (1989) A performance interpretation of multivariate tests of asset set intersection, spanning, and mean-variance efficiency. J Financial Quant Anal 24(2):185–204

Kai L, Asani S, Wang Z (2003) Diversification benefits of emerging markets subject to portfolio constraints. J Empir Finance 10(1–2):57–80

Kan R, Zhou G (2008) Tests of mean-variance spanning. Social Sciences Research Network. http://ssrn.com/abstract=231522. Accessed 9 December 2008

Kempf A, Memmel C (2005) On the estimation of the global minimum variance portfolio. Centre for Financial Research. Working paper No. 05-02

Korn O, Koziol C (2006) Bond portfolio optimization: a risk-return approach. J Fixed Income 15(4):48–60

Li W, Wang SS (2007) Ownership restriction, information diffusion speed, and the performance of technical trading rules in Chinese domestic and foreign shares markets. Rev Pac Basin Financial Mark Policies 10(4):585–617

Marshall BR, Young MR, Cahan R (2008) Are candlestick technical trading strategies profitable in the Japanese equity market? Rev Quant Finance Acc 31:191–207

Mercer J, Moore M, Winters D (2009) Do traders benefit from riding the T-bill yield curve? J Portfol Manage 36(1):131–140

Newey WK, West KD (1987) A simple positive semi-definite, heteroskedasticity and autocorrelation consistent covariance matrix. Econometrica 55:703–708

Pelaez RF (1997) Riding the yield curve: term premiums and excess returns. Rev Financial Econ 6(1):113–119

Petrella G (2005) Are Euro area small cap stocks and asset class? Evidence from mean-variance spanning tests. Eur Financial Manage 11(2):229–253

Pilotte EA, Sterbenz FP (2006) Sharpe and treynor ratios on treasury bonds. J Business 79(1):149–180

Reilly FK, Wright DJ, Gentry JA (2010) An analysis of credit risk spreads for high yield bonds. Rev Quant Finance Acc 35:179–205

Roll R (1971) Investment diversification and bond maturity. J Finance 26(1):51–66

Siegel LB (2008) Alternatives and liquidity: will spending and capital calls eat your ‘modern’ portfolio? J Portfol Manage 35(1):103–114

Van Zijl T (1987) Risk decomposition: variance or standard deviation - a reexamination and extension. J Financial Quant Anal 22(2):237–247

Wang KY, Peng SC, Huang YS (2009) The intraday performance of contrarian strategies: evidence from the Taiwan Stock Exchange. Rev Pac Basin Financial Mark Policies 12(4):655–674

Acknowledgments

We thank Constance Smith and two anonymous referees for helpful comments on an earlier draft.

Author information

Authors and Affiliations

Corresponding author

Appendix 1: Description of the data and data sources

Appendix 1: Description of the data and data sources

One month holding period yields (HPY) are calculated as in Bolder et al. (2004, 25–6), except that we use the exact number of days between monthly observations rather than an approximation:

where

-

HPY(t,N,T) = the holding period yield on a bond maturing in T years that is purchased at time t and held for N days,

-

d = N/(number of days in the year),

-

z(t,t+T) = the continuously compounded yield at time t on a zero-coupon bond that matures in T years.

The holding period yield reported for a particular date (observation) is the ex post yield realized from an investment made 1 month (3 months) prior to that date, where 1 month (3 months) is the length of the investment horizon. All yields are continuously compounded at annual rates.

The US yields used to calculate the holding period yields are constant maturity nominal US Treasury yields as of the last business day of the month. These were downloaded from the website of the Board of Governors of the US Federal Reserve. The methodology used to estimate the zero-coupon Treasury yield curves is described on the website of the Office of Debt Management, Department of the Treasury.

The Canadian zero-coupon yields are for the last business day of each month and were downloaded from the website of the Bank of Canada. The methodology used to calculate the Government of Canada zero-coupon bond yields is described in Bolder et al. (2004).

Rights and permissions

About this article

Cite this article

Galvani, V., Landon, S. Riding the yield curve: a spanning analysis. Rev Quant Finan Acc 40, 135–154 (2013). https://doi.org/10.1007/s11156-011-0267-7

Published:

Issue Date:

DOI: https://doi.org/10.1007/s11156-011-0267-7