Abstract

Empirical evidence suggests that firms often manipulate reported numbers to avoid debt covenant violations. We study how a firm’s ability to manipulate reports affects the terms of its debt contracts and the resulting investment and manipulation decisions that the firm implements. Our model generates novel empirical predictions regarding the use and the level of debt covenant, the interest rate, the efficiency of investment decisions, and the likelihood of covenant violations. For example, the model predicts that the optimal debt contract for firms with relatively strong (weak) corporate governance (i.e., cost of manipulation) induces overinvestment (underinvestment). Moreover, for firms with strong (weak) corporate governance, an increase in corporate governance quality leads to tighter (looser) covenant, more (less) frequent covenant violations and lower (higher) interest rate. Our model highlights that the interest rate, which is a common proxy for the cost of debt, neither accounts for the distortion of investment efficiency nor the expected manipulation costs arising under debt financing. We propose a measure of cost of debt capital that accounts for these effects.

Similar content being viewed by others

Notes

In this paper we restrict attention to debt financing and derive the optimal debt contract. While pure debt financing is not the optimal financing method in our setting, in additional analysis of an extended setting that includes hidden effort, we allow the firm to optimally choose the mix of debt and equity funding. Our numerical analysis demonstrates that the optimal mix includes both debt and equity. Hence the trade-off we identify in the baseline model qualitatively holds even under the optimal mix of debt and equity.

In the equilibrium of our model the manager’s payoff following liquidation is zero. However, our main results hold even if the manager obtains positive payoff following liquidation, as long as liquidation is ex-post costly to the manager compared to continuation of the project. Beneish and Press (1993) document that, in their sample, following technical covenant violation firms experience increased interest costs ranging between 0.84 and 1.63 percent of the market value of firms’ equity, and that costs of restructuring debt represent an average of 3.7% of the market value of equity.

A debt contract is not optimal in our setting, but there are frictions that would make it optimal. We have not modeled those frictions because we are most interested in debt contract design as opposed to broader financing contract design.

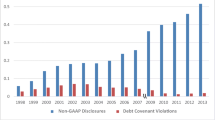

The empirical literature has provided ample evidence that managers take (costly) actions to avoid covenant violation. Some examples are DeFond and Jiambalvo (1994) which finds that “managers of firms approaching default respond with income-increasing accounting changes and that the default costs imposed by lenders and the accounting flexibility available to managers are important determinants of managers’ accounting responses.”

The specific cost function does not play an important role in the analysis. All the results qualitatively go through under any strictly increasing function of the magnitude of manipulation, e.g., quadratic cost function.

Violating a covenant is costly to the firm. The cost of a covenant violation can vary substantially across firms in terms of the type of cost and its magnitude. For example, covenant violation costs can be due to transfer of control rights; increased interest rate (that may lead to refinancing costs); lenders’ demand for partial or full repayment (which may lead to restructuring costs and modification of operations); and increased lender control and restrictions on assets sale, dividend payment, and investment activities (see e.g., Beneish and Press 1993).

We are allowing z to exceed the upper bound of the support of cash flows. While it is not natural to have a covenant that exceeds the highest possible outcome, this assumption does not drive any of the results in our model. As indicated earlier, the uniform distribution allows us to abstract from variation in the density of outcomes and simplifies the analysis.

We currently implicitly assume, and later show, that in equilibrium the lender always terminates the project following a covenant violation.

In general, the effect of z on expected misreporting costs is non-monotone. This is intuitive: the contract can eliminate misreporting costs by setting \(z = 0\), i.e., no covenant. Alternatively, the contract can mitigate misreporting by setting a very high covenant, so that misreporting is always too costly to the manager. (At the limit, such a contract awards all control rights to the lender.)

One can generalize the model to allow for positive lender bargaining power by modifying the participation constraint such that instead of receiving I the lender gets \(R>I\). In general, this would alter the debt contract’s efficiency. For example, in the limit as the manager’s residual surplus vanishes, his incentive to manipulate also vanishes, ensuring more efficient outcomes.

To gain some intuition for the U-shape of \(\mathcal {K}\left (\tau \right ) \), note that a low value of \(\tau \) (i.e., when the probability of continuation is high) means the lender is unlikely to get control rights. As such, for low values of \(\tau \) the lender demands a large face value to break even. As \(\tau \) increases, the lender gets extra control rights: we add more signals under which the project is terminated —which is consistent with the lender’s ex-post incentive for \(s=\tau \)— and hence the lender is willing to accept a lower face value. This continues up to a certain value of \(\tau \) for which the termination threshold, \(\tau \), is ex-post optimal from the lender’s standpoint, that is, for \(s=\tau \) the lender is indifferent between continuation and termination. As we further increase \(\tau \), the contract starts inducing excessive termination, even from the lender’s ex-post standpoint; hence, the lender demands additional compensation in terms of face value (recall \(\mathcal {K}\left (\cdot \right ) \) is derived assuming the lender can commit to terminating the project when he acquires control rights). As such, the face value for which the lender breaks even is a U-shape function of \(\tau \).

Naturally, \(\hat {\rho }\) depends on c and \(\hat {c}\) depends on \(\rho \). See Fig. 4.

Allowing for renegotiation when the manager meets the covenant —and is thus allowed to continue the project— seems empirically less realistic.

A positive face value would mean the contract has room for increasing \(\tau ^{\ast }\)—thereby decreasing the cost of manipulation— while still satisfying the lender’s participation constraint.

One could think of x as the firm’s true net worth, and r as a report about the firm’s net worth.

References

Aghion, P., & Bolton, P. (1992). An incomplete contracts approach to financial contracting. The Review of Economic Studies, 59(3), 473–494.

Ball, R., Bushman, R.M., Vasvari, F.P. (2008). The debt-contracting value of accounting information and loan syndicate structure. Journal of Accounting Research, 46(2), 247–287.

Beneish, M.D., & Press, E. (1993). Costs of technical violation of accounting-based debt covenants . The Accounting Review, 68(2), 233–257.

Beyer, A. (2013). Conservatism and aggregation: The effect on cost of equity capital and the efficiency of debt contracts. Rock Center for Corporate Governance at Stanford University Working Paper, (120).

Beyer, A., Guttman, I., Marinovic, I. (2014). Optimal contracts with performance manipulation. Journal of Accounting Research, 52(4), 817–847.

Bharath, S.T., Sunder, J., Sunder, S.V. (2008). Accounting quality and debt contracting. The Accounting Review, 83(1), 1–28.

Caskey, J., & Hughes, J.S. (2012). Assessing the impact of alternative fair value measures on the efficiency of project selection and continuation. The Accounting Review, 87(2), 483–512. https://doi.org/10.2308/accr-10201 https://doi.org/10.2308/accr-10201.

Chava, S., & Roberts, M.R. (2006). Is financial contracting costly? an empirical analysis of debt covenants and corporate investment. Rodney l white center for financial research-working papers-, 19.

Cornelli, F., & Yosha, O. (2003). Stage financing and the role of convertible securities. The Review of Economic Studies, 70(1), 1–32.

Costello, A., & Wittenwerg-Moerman, R. (2011). The impact of financial reporting quality on debt contracting: evidence from internal control weakness reports. Journal of Accounting Research, 49(1), 97–136.

DeFond, M.L., & Jiambalvo, J. (1994). Debt covenant violation and manipulation of accruals. Journal of Accounting and Economics, 17(1), 145–176.

Dessein, W. (2005). Information and control in ventures and alliances. The Journal of Finance, 60(5), 2513–2549.

Dichev, I.D., & Skinner, D.J. (2002). Large–sample evidence on the debt covenant hypothesis. Journal of Accounting Research, 40(4), 1091–1123.

Dutta, S., & Fan, Q. (2014). Equilibrium earnings management and managerial compensation in a multiperiod agency setting. Review of Accounting Studies, 19(3), 1047–1077.

Dye, R. (1988). Earnings management in an overlapping generations model. Journal of Accounting research, 26, 195–235.

Dyreng, S., Hillegeist, S., Penalva, F. (2011). Earnings management to avoid debt covenant violations and future performance. Technical report Working Paper, Duke University, Arizona State University.

Fischer, P., & Verrecchia, R. (2000). Reporting bias. The Accounting Review, 75(2), 229–245.

Gao, P. (2013). A measurement approach to conservatism and earnings management. Journal of Accounting and Economics, 55(2), 251–268.

Garleanu, N., & Zwiebel, J. (2009). Design and renegotiation of debt covenants. Review of Financial Studies, 22(2), 749–781.

Gigler, F., Kanodia, C., Sapra, H., Venugopalan, R. (2009). Accounting conservatism and the efficiency of debt contracts. Journal of Accounting Research, 47 (3), 767–797.

Goex, R.F., & Wagenhofer, A. (2009). Optimal impairment rules. Journal of Accounting and Economics, 48(1), 2–16.

Graham, J.R., Li, S., Qiu, J. (2008). Corporate misreporting and bank loan contracting. Journal of Financial Economics, 89(1), 44–61.

Grossman, S.J., & Hart, O.D. (1986). The costs and benefits of ownership: a theory of vertical and lateral integration. Journal of Political Economy, 94(4), 691–719.

Guttman, I., Kadan, O., Kandel, E. (2006). A rational expectations theory of kinks in financial reporting. The Accounting Review, 81(4), 811–848.

Hart, O.D. (1995). Firms, contracts, and financial structure. Oxford: Clarendon. ISBN: 978-0-19-828881-7.

Hart, O., & Moore, J. (1990). Property rights and the nature of the firm. Journal of Political Economy, 98(6), 1119–1158.

Hebert, B. (2015). Moral hazard and the optimality of debt. Available at SSRN 2185610.

Innes, R.D. (1990). Limited liability and incentive contracting with ex-ante action choices. Journal of Economic Theory, 52(1), 45–67.

Kim, J.B., Song, B.Y., Zhang, L. (2011). Internal control weakness and bank loan contracting: evidence from sox section 404 disclosures. The Accounting Review, 86(4), 1157–1188.

Laux, V. (2017). Debt covenants, renegotiation, and accounting manipulation.

Li, J. (2013). Accounting conservatism and debt contracts: efficient liquidation and covenant renegotiation. Contemporary Accounting Research, 30(3), 1082–1098.

Liang, P.J. (2000). Accounting recognition, moral hazard, and communication*. Contemporary Accounting Research, 17(3), 458–490.

Roberts, M.R., & Sufi, A. (2009). Renegotiation of financial contracts: evidence from private credit agreements. Journal of Financial Economics, 93(2), 159–184.

Sengupta, P. (1998). Corporate disclosure quality and the cost of debt. The Accounting Review, 73(4), 459–474.

Sridhar, S.S., & Magee, R.P. (1996). Financial contracts, opportunism, and disclosure management. Review of Accounting Studies, 1(3), 225–258.

Stein, J.C. (1989). Efficient capital markets, inefficient firms: a model of myopic corporate behavior. The Quarterly Journal of Economics, 104(4), 655–669.

Sweeney, A.P. (1994). Debt-covenant violations and managers’ accounting responses. Journal of accounting and Economics, 17(3), 281–308.

Townsend, R.M. (1979). Optimal contracts and competitive markets with costly state verification. Journal of Economic Theory, 21(2), 265–293.

Yu, F. (2005). Accounting transparency and the term structure of credit spreads. Journal of Financial Economics, 75(1), 53–84.

Author information

Authors and Affiliations

Corresponding author

Additional information

We thank Cyrus Aghamolla, Tim Baldenius (discussant), Anne Beyer, Jeremy Bertomeu, Paul Fischer (editor), Stephen Hillegeist (discussant), Beatrice Michaeli (discussant), Ningzhong Li, Stefan Reichelstein, Stephen Ryan, Paul Povel, Andy Skrzypacz, Felipe Varas, and Jeff Zwiebel for helpful comments; and seminar participants at Berkeley, New York University, University of Texas Dallas, UCLA and conference participants at Colorado Accounting Research Conference, Accounting Workshop in Basel, Stanford Summer Camp and Review of Accounting Studies Conference.

Appendix

Appendix

Proof of Lemma 1

Observe that

Using the lender’s participation constraint, while assuming \(\tau <K,\) yields

Solving for \(\mathcal {\mathcal {K}}\) yields

The function \(\mathcal {K}\left (\cdot \right ) \) is defined over \([0,\hat {\tau }]\) where \(\hat {\tau }\in \left (0,h\right ) \) is given by the solution to

Furthermore, observe that \(\frac {d\mathcal {K}\left (\tau \right ) }{d\tau } |_{\tau = 0}=h-\sqrt {h^{2}-2Ih}<0\). Also, it’s easy to verify that \(\frac {d \mathcal {K}\left (\tau \right ) }{d\tau }|_{\tau =\hat {\tau }}=\infty \) . The equation \(\frac {d\mathcal {K}\left (\tau \right ) }{d\tau }= 0\) has two solutions. We argue by contradiction that only one of the two solutions is in \([0,\hat {\tau }]\). By the Intermediate Value Theorem, at least one solution must lie in this interval, given that \( \frac {d\mathcal {K}}{d\tau }|_{\tau = 0}<0\) and \(\frac {d\mathcal {K}}{d\tau } |_{\tau =\hat {\tau }}>0\). If both solutions lay in this interval, then the equation

would have at least three solutions, which is a contradiction. Hence, the function \(\mathcal {K}\left (\tau \right ) \) has a unique minimum over the interval \(\left [ 0,\hat {\tau }\right ] \), denoted \(\tau ^{+}\), given by

□

Remark 1

In equilibrium \(\tau ^{\ast }\leq K^{\ast }\).

Proof of Remark 1

In equilibrium, the lender’s participation constraint is binding (otherwise, slightly decreasing the contract’s face value K, while holding constant the termination threshold \(\tau \), would satisfy the lender’s participation constraint and increase the manager’s expected payoff, despite increasing the expected manipulation cost). Hence,

For any \(s>K\) the continuation value to the lender is independent of s since

Suppose \(\tau ^{\ast }>K\). This implies that the lender’s expected payoff from continuation, given \(\tau ^{\ast }\), is strictly greater than his payoff upon termination, which is L. That is

Therefore, the lender strictly prefers to continue the project when \(s=\tau ^{\ast }\). The manager always prefers to continue the project. This implies there is a feasible contract that offers the lender the same face value and a lower threshold, and does not induce higher expected manipulation cost. Such a contract Pareto dominates the assumed contract; hence, a contract with \(\tau ^{\ast }>K^{\ast }\) is suboptimal. □

Proof of Lemma 2

We need to show that in any equilibrium \(\mathcal {K}^{\prime }\left (\tau \right ) \leq 0\). Let \(\left \{ z^{\ast },K^{\ast }\right \} \) be the equilibrium threshold and face value, then the manager’s expected payoff can be written as

where \(z^{\ast }\) is the solution to the manager’s misreporting constraint,

Let us consider an alternative contract \(\left \{ z^{o},K^{\ast }\right \} \) such that \(z^{o}=z^{\ast }-\varepsilon \) for small ε > 0. Define \(s^{o}\) as the solution to Eq. (11) such that \(c\left (z^{o}-s^{o}\right ) =\mathbb {E}\left (\max \left (x-K^{\ast }\right ) |s^{o}\right ) \). From Eq. (11), we see that \(z^{o}<z^{\ast }\) implies \(s^{o}<\tau ^{\ast }\). If \(\mathcal {K}^{\prime }\left (\tau ^{\ast }\right ) >0\) then the contract \( \left \{ z^{o},K^{\ast }\right \} \) is feasible. Indeed, recall that the set of feasible contracts is defined by

where, as shown before, \(\mathcal {K}\left (\cdot \right ) \) is a U -shaped function over \(\left [ 0,\hat {\tau }\right ] \). We will consider two cases: \(\tau ^{\ast }\leq K\) and τ∗ > K.

When \(\tau ^{\ast }\leq K\) a manager with a signal \(s=\tau ^{\ast }\) obtains positive expected payoff only if the signal is wrong, in which case his payoff from continuation is independent of \(\tau ^{\ast }\). This implies that \(z^{\ast }-\tau ^{\ast }\) is independent of \(\tau ^{\ast }\). In such a case, offering the contract \(\left \{ z^{o},K^{\ast }\right \} \) is preferable to the lender, increases the likelihood of continuation (which is beneficial to the manager), and will have no effect on the manager’s expected manipulation cost. As such, the contract \(\left \{ z^{o},K^{\ast }\right \} \) is feasible and strictly dominates the contract \(\left \{ z^{\ast },K^{\ast }\right \} \) for which \(\mathcal {K}^{\prime }\left (\tau ^{\ast }\right ) >0\).

When \(\tau ^{\ast }>K\) a manager with a signal \(s=\tau ^{\ast }\) obtains positive expected payoff both when the signal is informative and when it is uninformative. In this case, the manager’s expected payoff from continuation is increasing in \(\tau ^{\ast }\). This implies that \(z^{\ast }-\tau ^{\ast }\) is also increasing in \(\tau ^{\ast }\). To show that the contract \(\left \{ z^{o},K^{\ast }\right \} \) dominates \(\left \{ z^{\ast },K^{\ast }\right \} \) for which \(\mathcal {K}^{\prime }\left (\tau ^{\ast }\right ) >0\) note that decreasing τ∗ to \(s^{0}\) decreases the magnitude of the manipulation for each \(s\in \left [ \tau ^{\ast },h\right ] \); hence, the expected payoff of these types is higher under the contract \(\left \{ z^{o},K^{\ast }\right \} \) . All types \(s\in \left (s^{0},\tau ^{\ast }\right ) \) (who didn’t manipulate and terminated the project under \(\left \{ z^{\ast },K^{\ast }\right \} \)) prefer to manipulate and continue the project and hence prefer \(\left \{ z^{o},K^{\ast }\right \} \) over \(\left \{ z^{\ast },K^{\ast }\right \} \). Since the lender also prefers the contract \( \left \{ z^{o},K^{\ast }\right \} \), this contract is feasible and strictly dominates the contract \(\left \{ z^{\ast },K^{\ast }\right \} \) for which \( \mathcal {K}^{\prime }\left (\tau ^{\ast }\right ) >0\). □

Lemma 3

\(z^{\ast }>h\rightarrow \frac {dz^{\ast }}{dc}<0\) .

Proof of Lemma 3

Let \(\zeta \left (\tau \right ) \) be the covenant that induces a cutoff τ when the face value is \(\mathcal {K}\left (\tau \right ) \), or:

Now, \(\frac {\partial \zeta \left (\tau \right ) }{\partial c}<0\). Also we know that \(\mathcal {K}^{\prime }\left (\tau ^{\ast }\right ) \leq 0,\) which implies that \(\left . \frac {d\zeta \left (\tau \right ) }{d\tau }\right \vert _{\tau =\tau ^{\ast }}>0\) (given Lemma 2). Finally, by Lemma 4, we know that \(z^{\ast }>h\Rightarrow \frac { d\tau ^{\ast }}{dc}\) \(<0\). Taken together these results imply that when \( z^{\ast }=h,\)

□

Lemma 4

Suppose \(\rho \geq \hat {\rho }\) , then there is a unique \( \tilde {c}>\hat {c}\) such that \(z^{\ast }>h\) if and only if \(c<\tilde {c}\) .

Proof of Lemma 4

Clearly \(\lim _{c\rightarrow \infty }z^{\ast }=\tau ^{FB}<h\). Also, when ρ is large and c is small we have z∗ > h and

Taking limits \(\lim _{c\rightarrow 0}\tau ^{\ast }=\frac {h-\sqrt {\frac {h\left (h\rho -4\rho I + 2\rho L-2L + 2\rho ^{2}I + 2I\right )}{\rho }}}{1-\rho }>\tau ^{FB},\) hence \(\lim _{c\rightarrow 0}z^{\ast }=\infty \).

Finally, Lemma 3 proves that \(z^{\ast }=h\rightarrow \frac { dz^{\ast }}{dc}<0,\) so there is only one value \(\tilde {c}\) such that \( z^{\ast }=h,\) and \(z^{\ast }<h\) if and only if \(c>\tilde {c}\). Now, when \( z^{\ast }=h,\) the optimal threshold satisfies

so at \(c=\tilde {c}\) there is over-continuation, i.e., \(\tau ^{\ast }\left (\tilde {c}\right ) <\tau ^{FB}\). □

Lemma 5

If \(c\geq \tilde {c}\) the equilibrium entails over-continuation. Formally \(\tau ^{\ast }\leq \tau ^{FB}\) .

Proof of Lemma 5

See proof of Proposition 1. □

Corollary 2

There is \(\bar \rho \) such that for all \(\rho \geq \bar \rho \) and all \(c>0\) the optimal debt contract includes a covenant.

Proof of Corollary 2

First, we show that using a covenant is optimal when \(\rho \in \left (1-\varepsilon ,1\right ) \) , even as \(c\rightarrow 0\). The optimal threshold, in the absence of manipulation, is defined as:

By assumption \(V^{FB}>\mathbb {E}\left (x\right ) \). We argue that for \(\rho \) high enough, the debt contract includes a covenant, even as \(c\rightarrow 0\). Suppose we implement τFB as the contract’s threshold (perhaps sub-optimally) and set the face value accordingly at \(\mathcal {K}\left (\tau ^{FB}\right ) \) to satisfy the lender’s participation constraint. Assuming the contract leads to \(z\left (\tau ^{FB}\right ) >h\) (which we can always guarantee by making c small enough), then the expected payoff of the manager is

Now, since

This means we can select \(\rho \ \)close to 1, denoted \(\rho ^{+}\), to ensure

Of course, for a fixed \(c,\) a large \(\rho \) may lead to \(\zeta \left (\tau ^{FB}\right ) <h\). So to ensure \(\zeta \left (\tau ^{FB}\right ) >h,\) we pick \( c\) small enough, say \(c_{0}\), such that

This proves that using a covenant is optimal for sufficiently high \(\rho ,\) even as \(c\rightarrow 0\). □

Lemma 6

\(\lim _{c\rightarrow 0}\tau ^{\ast }=\frac {h-\sqrt {\frac { h\left (h\rho -4\rho I + 2\rho L-2L + 2\rho ^{2}I + 2I\right ) }{\rho }}}{1-\rho }>\tau ^{FB}\) and when \(z^{\ast }>h,\) \(\lim _{\rho \rightarrow 1}\tau ^{\ast }=\frac {L-ch}{1-c}<\tau ^{FB}\) .

Proof of Lemma Lemma 6

To obtain the \(\lim _{c\rightarrow 0}\tau ^{\ast }\) we take the first order condition of the manager’s optimization program with respect to \(\tau \), assuming \(\tau ^{\ast }>h\):

which leads to the first order condition

Now, taking the limit as \(c\rightarrow 0\) and solving for \(\tau \) yields

We argue that \(\lim _{c\rightarrow 0}\tau ^{\ast }>\tau ^{FB}\). In effect,

and

When \(\rho >\hat {\rho },\) and \(c\leq \tilde {c}\), the optimal debt contract includes a covenant. Taking the limit of the FOC as \(\rho \rightarrow 1\) and solving for \(\tau ^{\ast }\) yields

□

Corollary 3

When \(z^{\ast }\leq h,\ \frac {\partial \tau ^{\ast }}{\partial c}>0\) and \(\frac {\partial K^{\ast }}{\partial c}<0\) .

Proof of Corollary 3

From Lemma 5, we know that \(z^{\ast }\leq h\Rightarrow \) \( \chi ^{\prime }\left (\tau ^{\ast }\right ) >0\). Hence \(\frac {\partial \chi ^{\prime }\left (\tau ^{\ast }\right ) }{\partial c}=-\frac {1}{c}\chi ^{\prime }\left (\tau ^{\ast }\right ) <0\). Now the first order condition is

This in turn implies that the face value decreases in c. □

Corollary 4

When \(z^{\ast }\geq h\) , \(\frac {\partial \tau ^{\ast }}{\partial c}<0\) and \(\frac {\partial K^{\ast }}{\partial c}>0\) .

Proof of Corollary 4

For a given \(\tau \) (such that \(\zeta \left (\tau \right ) \geq h\)) we can write the manager’s expected payoff as

The cross partial derivative is

which means that in equilibrium

□

Proof of Proposition 1

First we show that the contract includes a covenant if and only if precision ρ is high enough. Recall that \(\hat {\rho }\) is defined by

\(\hat {\rho }\) is the precision level such that the firm is indifferent between using a covenant and not using one. Next we argue that the firm will use a covenant if and only if \(\rho \geq \hat {\rho }\). Suppose, by contradiction, that for some \(\rho \in \left (\hat {\rho },1\right ) \) the firm does not use a covenant. Then we have that

To prove that this leads to a contradiction, we construct a feasible contract that yields payoffs above \(E\left (x\right ) -I\). Indeed, consider a contract implementing the same threshold \(\tau ^{\ast }\left (\hat {\rho } \right ) \) and face value \(K^{\ast }\left (\hat {\rho }\right ) \) as under precision \(\hat {\rho }\). This new contract strictly satisfies the lender’s participation constraint. Furthermore,

Hence, the contract we have constructed yields both higher continuation cash flows and lower misreporting costs under \(\rho \) than the optimal debt contract under \(\hat {\rho }\), hence it must dominate a no-covenant contract. To prove the other direction suppose \(\rho <\hat {\rho },\) but the debt contract includes a covenant, so

Then consider using \(\left \{ \tau ^{\ast }\left (\rho \right ) ,K^{\ast }\left (\rho \right ) \right \} \) under precision \(\hat {\rho }\). If this contract was feasible under precision \(\rho \) it must also be feasible under \(\hat {\rho }\) given that \(\hat {\rho }>\rho \). Clearly, this contract must give the manager a higher payoff under \(\hat {\rho }\) than under \(\rho ,\) hence

which is a contradiction. Next, we show that when \(\rho \geq \hat {\rho }\) there is over-continuation if and only if the cost of misreporting is higher than \(\hat {c}\). Define \(\tau ^{\ast }\left (c\right ) \) as

First, Corollary 2 demonstrates that \(\lim _{c\downarrow 0}\tau ^{\ast }\left (c\right ) >\tau ^{FB}\). Also, Corollary 3 and Corollary 4 prove that \(\tau ^{\ast }\left (c\right ) \) decreases (resp. increases) in c for \(c\geq \tilde {c}\) (resp. \(c<\tilde {c}\)) where \(\tilde {c}\) is defined as \(\zeta \left (\tau ^{\ast }\left (\tilde {c}\right ) \right ) =h\) (i.e, the value of c such that the equilibrium covenant is equal to h). Finally, \(\lim _{c\rightarrow \infty }\tau ^{\ast }\left (c\right ) =\tau ^{FB}\). Taken together these observations establish that there is a unique \(\hat {c}\) defined

such that if \(c\leq \hat {c}\) (resp. \(c>\hat {c}\)) there is over-termination (resp. over-continuation).

Consider uniqueness of the optimal threshold \(\tau ^{\ast }\). When \(z^{\ast }\geq h\) the proof follows by contradiction. In this case, the first order condition of \(V^{\prime }(\tau )=\chi ^{\prime }(\tau )\) is a third order polynomial and has at most three real solutions, but the smallest solution is negative. The other two consecutive solutions cannot be both maxima, hence the maximum must be unique. When \(z^{\ast }<h\) the first order condition is a fourth order polynomial, so there can be (at most) two local maxima of \({\Pi } \left (\tau \right ) \) . Now, we will show that one of the maxima lies on \([\frac {h}{1-\rho },\infty ),\) being outside the relevant range. Indeed,

and

This means there is at least one local maxima in \([\frac {h}{1-\rho },\infty )\) which proves the optimal threshold is unique. □

Proof of Proposition 2

First we prove the comparative statics with respect to c. As before, we define

(Note that \(\tau ^{\ast }\left (c\right ) \) is not necessarily the optimal threshold since the optimal debt contract may use no covenant, in which case \(z^{\ast }=\tau ^{\ast }= 0\).)

Lemma 3 proves there is a unique value of \(c,\) denoted \(\tilde { c},\) such that the covenant is \(z^{\ast }=h\). If \(c<\tilde {c}\) (resp. \(c> \tilde {c}\)) the covenant is larger (smaller) than h. On the other hand,

Hence, sign\(\left \{ \frac {\partial \tau ^{\ast }\left (c\right ) }{\partial c} \right \} =\textit {sign}\left (\frac {-\partial \chi ^{\prime }\left (\tau ^{\ast }\left (c\right ) \right ) }{\partial c}\right ) \) . Now when \(c<\tilde {c,}\) we have \(\frac {-\partial \chi ^{\prime }\left (\tau ^{\ast }\left (c\right ) \right ) }{\partial c}<0,\) hence \(\frac {\partial \tau ^{\ast }\left (c\right ) }{\partial c}<0\). When \(c>\tilde {c},\) we have \(\frac {-\partial \chi ^{\prime }\left (\tau ^{\ast }\left (c\right ) \right ) }{\partial c}=-\frac {1}{c}\chi ^{\prime }\left (\tau ^{\ast }\left (c\right ) \right ) <0,\) and \(\chi ^{\prime }\left (\tau ^{\ast }\left (c\right ) \right ) >0,\) hence \(\frac { \partial \tau ^{\ast }\left (c\right ) }{\partial c}>0\). Also, since \(\frac { \partial K^{\ast }}{\partial c}=\mathcal {K}^{\prime }\left (\tau ^{\ast }\right ) \frac {\partial \tau ^{\ast }\left (c\right ) }{\partial c}\) the sign \(\left (-\frac {\partial K^{\ast }}{\partial c}\right ) =\textit {sign}\left (\frac { \partial \tau ^{\ast }\left (c\right ) }{\partial c}\right ) ,\) since \( \mathcal {K}^{\prime }\left (\tau ^{\ast }\right ) <0\). Consider the comparative statics with respect to \(\rho \). Consider the \(z^{\ast }>h\) case. We have:

For \(c\approx 0\), we have \(\tau ^{\ast }\approx L\). Plugging \(\tau ^{\ast }\approx L\) above yields \(\lim _{\rho \rightarrow 1}\frac {\partial \tau ^{\ast }}{\partial \rho }\approx \allowbreak \frac {-L^{2}+ 2h\left (I-L\right ) }{-{\Pi }_{\tau \tau }2h^{2}}\) which is negative as \(L\rightarrow I\). This shows that \(\tau ^{\ast }\) may decrease in \(\rho ,\) for sufficiently high \(\rho \) and small c. However, we can verify that even in this case, we have \(\lim _{\rho \rightarrow 1,c\rightarrow 0}\frac {\partial K^{\ast }}{ \partial \rho }<0\). Consider the \(z^{\ast }<h\) case. It’s easy to verify \( \lim _{\rho \rightarrow 1}{\Pi }_{\tau \rho }^{\ast }=\frac {E\left (x\right ) -\tau ^{\ast }}{4h}\). Since \(\tau ^{\ast }<E\left (x\right ) ,\) this implies that \(\lim _{\rho \rightarrow 1}\frac {\partial \tau ^{\ast }}{\partial \rho } >0\). □

Rights and permissions

About this article

Cite this article

Guttman, I., Marinovic, I. Debt contracts in the presence of performance manipulation. Rev Account Stud 23, 1005–1041 (2018). https://doi.org/10.1007/s11142-018-9450-6

Published:

Issue Date:

DOI: https://doi.org/10.1007/s11142-018-9450-6