Abstract

This paper quantifies the fiscal and distributional impact of tax expenditures related to public and private contributory pension schemes, affecting both contributions and pension benefits, in all EU Member States using EUROMOD, the EU-wide microsimulation model. Adopting a benchmark system in which pension contributions are exempt and taxes apply when benefits are received (EET system), we find that pension-related tax expenditures can have a sizeable impact on revenue and strong effects on inequality and poverty. Tax expenditures tend to be progressive on two levels: first, among pensioners, by favoring those with lower incomes, mainly as a result of the preferential treatment given to pension incomes; and, second, among people of working age, through a partial or no deduction of pension contributions, draining resources from those at the top of the income distribution. Moreover, embracing a lifetime perspective, tax expenditures tend to redistribute resources in favor of women and low-educated individuals.

Source: Contribution rates from EUROMOD country reports based on national legislation (https://www.euromod.ac.uk/using-euromod/country-reports/ retrieved February 5, 2018). Replacement rates from OECD, Pensions at a Glance 2017 (http://stats.oecd.org/retrieved February 5, 2018). Information is missing for Croatia, Cyprus, Lithuania, Malta, Bulgaria, Romania and Latvia. Contribution rates are the sum of the rates paid by employers and employees and refer to mandatory old-age pension schemes only. The net replacement rate is defined as the individual net pension entitlement divided by net pre-retirement earnings, taking account of personal income taxes and social security contributions paid by workers and pensioners. R2: 0.06

Source: Authors’ simulations with EUROMOD H0.34. Tax expenditures measured comparing the baseline with E-T counterfactuals. Croatia, Denmark, Luxembourg, Poland and Spain show a cost of pension-related tax expenditures, as a percentage of tax revenue in the baseline scenario, of close to 0 and so are not included in the figure. Gini indices in the baseline are reported in Table 4 in the Appendix

Source: Authors’ simulations with EUROMOD H0.34. Tax expenditures measured comparing the baseline with E-T counterfactuals. Change in equivalized disposable income (DPI) for individuals in 16 age groups. Income equivalized using the OECD modified equivalence scale. Different scales across countries

Source: Authors’ simulations with EUROMOD H0.34. Tax expenditures measured comparing the baseline with E-T counterfactuals. Change in equivalized disposable income (DPI) by decile groups based on equivalized disposable income in the baseline. Income equivalized using the OECD modified equivalence scale. Different scales across countries. Note The bars indicate the relative income changes by decile, decomposed for the three different household types as indicated by the different colors (Color figure online)

Source: Authors’ simulations with EUROMOD H0.34. Tax expenditures measured comparing the baseline with E-T counterfactuals. Croatia, Denmark, Hungary, Luxembourg, Malta, Poland, Spain, and the UK show a cost of tax expenditures on pension benefits, as a percentage of tax revenue in the baseline scenario, of around 0 and so are not labeled in the figure. R2: 0.35. Elderly poverty rates in the baseline are reported in Table 4 in the Appendix (Color figure online)

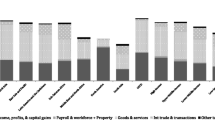

Source: Authors’ simulations with EUROMOD H0.34.Tax expenditures measured comparing the baseline with E-T counterfactuals. The present value of tax expenditures (as % of Gross Income in the baseline) based on a discount rate set at 2% and GDP nominal growth set at 1.3%. Different scales across countries

Similar content being viewed by others

Notes

The motivation behind the tax exemption of an employer’s contribution to an employee’s pension fund is that it is not considered “income” in tax law, because the employee has no choice about to how to spend the contribution (Cremer and Pestieau 2016).

A PAYG system is a pension system in which state retirement benefits are financed by contributions levied from current workers, as opposed to a funded system in which contributions are invested to pay for future pension benefits.

Alternative budgetary approaches are: the revenue gain approach which quantifies the increase in revenue that could be expected if a particular tax concession was to be removed; the revenue outlay method, which estimates the pre-tax expenditure required to achieve the same after-tax benefit if a given tax expenditure were to be replaced by a corresponding public expenditure program; and finally, the approach which adopts an explicitly dynamic perspective by estimating the present value of the tax savings associated with the tax expenditure (Swift 2006).

Choosing a different benchmark would lead to different conclusions. See, for example, Collins and Hughes (2016), who analyzed the case of Ireland, showing the revenue costs of the existing tax reliefs for superannuation contributions. In our analysis, we show that, using counterfactual scenarios characterized by exempted contributions and taxed pension benefits, the age-related limits on the deductibility of superannuation contributions count as a negative tax expenditure and imply a net revenue gain. For transparency, in Table 3 in the Appendix, we also report empirical evidence of the fiscal effects of pension-related tax expenditures obtained when using counterfactuals characterized by taxed contributions and exempted pension benefits (i.e., counterfactuals T-E), which represent the most appropriate counterfactuals to describe the size of the pension-related tax expenditures with respect to an income tax benchmark.

Nevertheless, the numbers in Tables 2 and 3 allow us also to quantify the tax expenditures with respect to a "reference law" baseline (i.e., tax expenditures as deviations from the existing general tax rules without considering the issues related to double taxation of contributions and benefits). In particular, columns f and g of Table 3 provide a quantification of the revenue cost of the (partial or complete) deduction of contributions, while columns c and d of Table 2 provide a quantification of the revenue cost of the existing tax reliefs on pension benefits.

At the same time, because of a lack of detailed information in the underlying data, the EUROMOD simulations might not be able to capture all details embedded in the national tax legislation.

See https://www.euromod.ac.uk/using-euromod/country-reports (retrieved March 15, 2018).

Prime examples of the EU-level policy analysis with EUROMOD are its regular use for the Social Situation Monitor (retrieved March 15, 2018 from http://ec.europa.eu/social/main.jsp?catId=1049&) and increasing occurrence in annual country assessments as part of the European Semester (retrieved March 15, 2018, from http://ec.europa.eu/economy_finance/eu/index_en.htm). In addition, EUROMOD has been applied in numerous policy analyses at the national level.

The micro-data used for the UK come from the Family Resource Survey.

Alternative taxonomies group pension schemes according to whether they are public or private, but these can be misleading in a cross-country analysis.

Since 2013, a number of reforms to pension-related tax expenditures occurred, including abolishing tax relief on pension benefits (e.g., old-age asset allowance in the Netherlands, regional tax credit related to age in the Balearic Islands (Spain), seniority allowance in Slovenia and age allowance in the UK) and on contributions to third pillar schemes (e.g., tax relief abolished in Sweden and Slovakia).

Working-age households are those with at least one individual of working age and nobody in old age. Pensioner households are those with at least one individual in old age and nobody of working age.

References

Armstrong, A., Davis, E. P., & Ebell, M. (2015). An economic analysis of the existing taxation of pensions (EET) versus an alternative regime (TEE). London: NIESR Discussion Paper No 455.

Auerbach, A. (2012). The Mirrlees review: A US perspective. National Tax Journal, 65, 685–708.

Auerbach, A. J., Gokhale, J., & Kotlikoff, L. J. (1994). Generational accounting: A meaningful way to evaluate fiscal policy. Journal of Economic Perspectives, 8(1), 73–94.

Avram, S. (2018). Who benefits from the ‘hidden welfare state’? The distributional effects of personal income tax expenditure in six countries. Journal of European Social Policy, 28(3), 271–293.

Banks, J., & Diamond, P. (2010). The base for direct taxation. In J. Mirrlees, S. Adam, T. Besley, R. Blundell, S. Bond, R. Chote, M. Gammie, P. Johnson, G. Myles, & J. Poterba (Eds.), Dimensions of tax design: The Mirrlees review. Oxford: Oxford University Press for Institute for Fiscal Studies.

Bargain, O., Orsini, K., & Peichl, A. (2014). Comparing labor supply elasticities in Europe and the US: New results. Journal of Human Resources, 49, 723–838.

Barrios, S., Fatica, S., Martinez, D., & Mourre, G. (2018). The fiscal effects of work-related tax expenditures in Europe. Public Finance Review, 46(5), 793–820.

Booth, P., & Cooper, D. (2002). The tax treatment of UK defined contribution pension schemes. Fiscal Studies, 23, 77–104.

Bourguignon, F., & Spadaro, A. (2006). Microsimulation as a tool for evaluating redistribution policies. Journal of Economic Inequality, 4, 77–106.

Burman, L. E., Geissler, C., & Toder, E. J. (2008). How big are total individual income tax expenditures, and who benefits from them? American Economic Review, 98, 79–83.

Burman, L. E., & Phaup, M. (2012). Tax expenditures, the size and efficiency of government, and implications for budget reform. In J. Brown (Ed.), Tax policy and the economy (Vol. 26). Chicago: University of Chicago Press.

Burton, M., & Sadiq, K. (2013). Tax expenditure management: A critical assessment. Cambridge: Cambridge University Press.

Caminada, K., & Goudswaard, K. (2008). Revenue effects of tax facilities for pension savings. Atlantic Economic Journal, 36, 233–246.

Chen, D. H. J., Beetsma, R. M. W. J., Ponds, E. H. M., & Romp, W. E. (2016). Intergenerational risk-sharing through funded pensions and public debt. Journal of Pension Economics & Finance, 15, 127–159.

Chetty, R., Friedman, J., Leth-Petersen, S., Heien Nielsen, T., & Olsen, T. (2014). Active vs. passive decisions and crowd-out in retirement savings accounts: Evidence from Denmark. Quarterly Journal of Economics, 129, 1141–1219.

Clinton, K., Kumhof, M., Laxton, D., & Mursula, S. (2011). Deficit reduction: Short-term pain for long-term gain. European Economic Review, 55, 118–139.

Collins, M. L., & Hughes, G. (2016). Tax expenditure on occupational pensions in Ireland: Relevance, cost and distribution. Dublin: Nevin Economic Research Institute, mimeo.

Cremer, H., & Pestieau, P. (2016). Taxing pensions. München: CESifo Working Paper No 5930.

Dilnot, A., & Johnson, P. (1993). The taxation of private pensions. IFS Reports No R43. London: Institute for Fiscal Studies.

Disney, R. (2007). Population ageing and the size of the welfare state: Is there a puzzle to explain? European Journal of Political Economy, 23, 542–553.

Doerrenberg, P., & Peichl, A. (2014). The impact of redistributive policies on inequality in OECD countries. Applied Economics, 46, 2066–2086.

Dolls, M., Doorley, K., Paulus, A., Schneider, H., & Sommer, E. (2019). Demographic change and the European income distribution. Journal of Economic Inequality, 17(3), 337–357.

Dolls, M., Fuest, C., & Peichl, A. (2012). Automatic stabilizers and economic crisis: US vs. Europe. Journal of Public Economics, 96, 279–294.

European Commission. (2010). Green paper towards adequate, sustainable and safe European pension systems. Brussels: European Commission.

European Commission (2017). The 2018 Ageing Report: Underlying assumptions and projection methodologies. Brussels: European Commission: Institutional Paper 065.

Feher, C., & Jousten, A. (2018). Taxation and pensions: An overview of interplay. In R. Holzmann & J. Piggott (Eds.), The taxation of pensions. Cambridge: MIT Press.

Figari, F., Matsaganis, M., & Sutherland, H. (2013). The financial well-being of older people in Europe and the redistributive effects of minimum pension schemes. Rivista Italiana degli Economisti—The Journal of the Italian Economic Association, 4, 149–174.

Figari, F., Paulus, A., & Sutherland, H. (2015). Microsimulation and policy analysis, Chapter 24. In A. B. Atkinson & F. Bourguignon (Eds.), Handbook of income distribution (Vol. 2B). Amsterdam: Elsevier.

Galasso, V., & Profeta, P. (2002). Political economy models of social security: A survey. European Journal of Political Economy, 18, 1–29.

Gruber, J., & Wise, D. A. (2004). Social security and retirement around the word: Micro-estimations. Chicago: University of Chicago Press.

Hall, R. E. (2010). Commentary on J. Banks and P. Diamond, the base for direct taxation. In J. Mirrlees, S. Adam, T. Besley, R. Blundell, S. Bond, R. Chote, M. Gammie, P. Johnson, G. Myles, & J. Poterba (Eds.), Dimensions of tax design: The Mirrlees review. Oxford: Oxford University Press for Institute for Fiscal Studies.

Holzmann, R., Robalino, D. A., & Takayama, N. (2009). Closing the coverage gap: The role of social pensions and other retirement income transfers. Washington, DC: World Bank.

Immervoll, H., Kleven, H. J., Kreiner, C. T., & Verdelin, N. (2011). Optimal tax and transfer programs for couples with extensive labor supply responses. Journal of Public Economics, 95, 1485–1500.

Kalyva, A., Astarita, C., Bauger, L., Fatica, S., Mourre, G., & Wöhlbier, F. (2014). Tax expenditures in direct taxation in EU Member States. European Economy, Occasional Papers 207. Brussels, Belgium: Directorate-General for Economic and Financial Affairs.

Matsaganis, M., & Leventi, C. (2014). The distributional impact of austerity and the recession in southern Europe. South European Society and Politics, 19, 393–412.

Meade, J. E. (1978). The structure and reform of direct taxation. London: George Allen and Unwin.

Mirrlees, J., Adam, S., Besley, T., Blundell, R., Bond, S., Chote, R., et al. (2011). Tax by design: The Mirrlees review. Oxford: Oxford University Press for Institute for Fiscal Studies.

OECD. (2003). Revenue Statistics 1965–2002. Special features: Tax reliefs and the interpretation of tax-to-GDP ratios. Paris: OECD Publishing.

OECD. (2010). Tax expenditure in OECD countries. Paris: OECD Publishing.

OECD. (2015). Pensions at a Glance 2015: OECD and G20 indicators. Paris: OECD Publishing.

OECD. (2016). OECD Pensions Outlook 2016. Paris: OECD Publishing.

Romaniuk, K. (2013). Pension fund taxation and risk-taking: Should we switch from the EET to the TEE regime? Annals of Finance, 9, 573–588.

Stebbing, A., & Spies-Butcher, B. (2010). Universal welfare by “other means”? Social tax expenditures and the Australian dual welfare state. Journal of Social Policy, 39, 585–606.

Surrey, S. (1973). Pathways to tax reform: The concept of tax expenditures. Cambridge: Harvard University Press.

Sutherland, H., & Figari, F. (2013). EUROMOD: The European Union tax-benefit microsimulation model. International Journal of Microsimulation, 6, 4–26.

Swift, Z. L. (2006). Managing the effects of tax expenditures on national budgets. World Bank Policy Research Working Paper 3927. Washington, DC: World Bank.

Ter Rele, H. (2007). Measuring the lifetime redistribution achieved by Dutch taxation, cash transfer and non-cash benefits programs. Review of Income and Wealth, 53(2), 335–362.

Toder, E. J. (2000). Tax cuts or spending—Does it make a difference? National Tax Journal, 53, 361–371.

Toder, E. J. (2009). Taxation of saving for retirement: Current rules and alternative reform approaches. Washington: Tax Policy Center, Urban Institute and Bookings Institution.

Whitehouse, E. (2005). Taxation: The tax treatment of funded pensions. World Bank Pension Reform Primer Series. Washington, DC: World Bank.

Zaidi, A., Grech, A., & Fuchs, M. (2006). Pension policy in EU25 and its possible impact on elderly poverty. CASE 116. London: London School of Economics.

Acknowledgements

Funding was provided by Joint Programming Initiative More Years, Better Lives (Grant No. CIRCLE). The results presented here are based on EUROMOD version H0.34. EUROMOD is developed by ISER at the University of Essex, in collaboration with national teams from the EU member states. We are indebted to Holly Sutherland and the many people who have contributed to the development of EUROMOD. The process of updating EUROMOD is supported by the European Union Programme for Employment and Social Innovation ‘Easi’ (2014–2020). We use microdata from the EU Statistics on Incomes and Living Conditions (EU-SILC) made available by NSIs and Eurostat under Contract EUSILC 2011/55 and (for the UK) the Family Resources Survey data made available by the Department of Work and Pensions via the UK Data Archive. We are grateful to M. Belloni, A. Jousten, S. Riscado, A. Brender, M. Cioffi, M. Savegnano and participants at the presentations at the University of Antwerp (March 2017), IMA Conference (June 2017), CEF Ljubljana (April 2018), Banca d’Italia (March 2018), JRC Fiscal Policy analysis seminars (June 2018), CeRP Workshop (July 2019) for helpful comments. F. Coda Moscarola, F. Figari and L. Gandullia acknowledge the support of CeRP Collegio Carlo Alberto through the JPI MYBL (Project “Care and Income Redistributive Cycles in the Lives of the Europeans”). The findings, interpretations and conclusions expressed in this paper are entirely those of the authors. They should not be attributed to the European Commission. Any mistakes are the authors’ only.

Author information

Authors and Affiliations

Corresponding author

Additional information

Publisher's Note

Springer Nature remains neutral with regard to jurisdictional claims in published maps and institutional affiliations.

Appendix

Appendix

Rights and permissions

About this article

Cite this article

Barrios, S., Coda Moscarola, F., Figari, F. et al. Size and distributional pattern of pension-related tax expenditures in European countries. Int Tax Public Finance 27, 1287–1320 (2020). https://doi.org/10.1007/s10797-019-09580-7

Published:

Issue Date:

DOI: https://doi.org/10.1007/s10797-019-09580-7