Abstract

The shift away from coal is at the heart of the global low-carbon transition. Can governments of coal-producing countries help facilitate this transition and benefit from it? This paper analyses the case for coal taxes as supply-side climate policy implemented by large coal exporting countries. Coal taxes can reduce global carbon dioxide emissions and benefit coal-rich countries through improved terms-of-trade and tax revenue. We employ a multi-period equilibrium model of the international steam coal market to study a tax on steam coal levied by Australia alone, by a coalition of major exporting countries, by all exporters, and by all producers. A unilateral export tax has little impact on global emissions and global coal prices as other countries compensate for reduced export volumes from the taxing country. By contrast, a tax jointly levied by a coalition of major coal exporters would significantly reduce global emissions from steam coal and leave them with a net sector level welfare gain, approximated by the sum of producer surplus, consumer surplus, and tax revenue. Production taxes consistently yield higher tax revenues and have greater effects on global coal consumption with smaller rates of carbon leakages. Questions remain whether coal taxes by major suppliers would be politically feasible, even if they could yield economic benefits.

Similar content being viewed by others

Notes

Steam coal includes all hard coal that is not coking coal (used for steel production), as well as sub-bituminous brown coal (IEA/OECD 2013). It is mainly used for electricity generation and has by far the largest share in global extraction across the different types of coal.

A debate about constraints on coal exports in the interest of climate change mitigation is nascent in Australia, but to date has not been underpinned by quantitative analyses. See for instance, Peter Christoff (http://theconversation.com/why-australia-must-stop-exporting-coal-9698) and Brett Parris (http://theconversation.com/expanding-coal-exports-is-bad-news-for-australia-and-the-world-17937). A tax review proposed a resource rent tax including coal (Commonwealth of Australia 2010), which was legislated in 2012 but repealed in 2014. Relatedly, Martin (2014) suggests a coal-export safeguard regime to ensure that trade only occurs with partners that offset related CO2 emissions.

Recently, the literature on international steam coal markets gained some attention. In the tradition of Kolstad and Abbey (1984), two numerical equilibrium models of the international steam coal market have been developed: COALMOD-WORLD, which we further develop in this paper, and one model by Paulus and Trüby (2011) and Trüby and Paulus (2012).

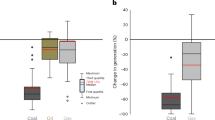

This welfare measure does not represent any economy-wide effects that flow from changed prices and resource allocations within an economy.

Kalkuhl and Brecha (2013) speak of climate rents, which are created by the climate policy-induced scarcity of remaining CO2 emissions. In this context, Eisenack et al. (2012) find that—depending on the allocation rule—a global carbon cap may leave resource owners better off compared to a business-as-usual.

The Electronic Supplementary Materials (ESM) contain the complete mathematical formulation of the model for the case of coal taxes—both on production and on exports-only—as well as a list of all endogenous variables and parameters.

Numerical applications of MPECs can be found in a wide range of disciplines and research questions. In contrast to analyses of market power with similar players on both the upper and lower level (cf. Siddiqui and Gabriel 2013; Trüby 2013; Gabriel and Leuthold 2010), our framework allows for the analysis of economic policy decisions given the reaction of market participants. Similar applications include Matar et al. (2015) on optimal investment credits to increase energy efficiency and reduce oil consumption in Saudi-Arabia, Bard et al. (2000)on the optimal incentive to encourage the production of biomass, Labbé et al. (1998) on the optimal toll setting for a road network, and Scaparra and Church (2008) on the cost-efficient way to protect a service system from being disrupted by saboteurs or terrorists. To the best of our knowledge, our study is the first that numerically analyses a supply-side climate policy implementation (at the upper level) on an international fossil fuel market (at the lower level).

A complete list of nodes can be found in the ESM.

The exporters’ grand coalition consists of Australia, Colombia, Mozambique, Indonesia, Poland, Russia, South Africa, Ukraine, the USA, and Venezuela.

Note that we only indirectly account for substitution with other fossil fuels through inverse demand functions. A relative price increase in coal, e.g. through coal taxes, could partly ramp up the consumption of natural gas and crude oil, leading to increased emissions from these sources. Nevertheless, since coal is the most carbon-intensive fossil fuel, global emissions would likely decline.

Additional figures and tables are provided in the ESM. There, we also present guiding Base Case results.

Note that this rebound effect is expressed on a country-basis, i.e. 73.3% of reduced Australian emissions from production are compensated by other producers. The rebound effect would be even higher (75.9%) when expressed on a policy-basis, i.e. how much of Australian emissions from export supply are compensated making the shift to domestic consumers explicit. The two types of carbon leakage only differ for coal taxes on exports while they coincide for coal taxes on the entire production.

To put this reduction into perspective, note the recent closure of a large lignite power plant which emitted around 15 MtCO2 per year is expected to reduce emissions by 5 MtCO2 per year in the short term (Jotzo and Mazouz 2015) and more in the long term.

We test the sensitivity of the results to the members of the coalition by adding the USA (see the ESM). We find a substantial increase in tax revenues and CO2 emission reductions, while the US share in additional revenue is small.

With 74.7% the rebound effect is even larger than in the Tax AUS scenario. This can be explained by characteristics of the new coalition members South Africa and Colombia. While both exporters do not compensate in Tax AUS due to capacity restrictions, it is their reduced supply in the Tax Coalition scenario that is (partly) compensated by (mainly) India and China.

Setting these results in perspective, this reduction corresponds to reduced profits for marginal suppliers (or even losses in the case of long-term contracts, or stranded infrastructure investments), while local infra-marginal suppliers could be net benefiters of increased prices. This is in contrast to a demand-side policy, which depresses prices and puts all producers at a disadvantage.

References

Bard JF, Plummer J, Sourie JC (2000) A bilevel programming approach to determining tax credits for biofuel production. Eur J Oper Res 120(1):30–46. https://doi.org/10.1016/S0377-2217(98)00373-7

Böhringer C, Rosendahl KE, Schneider J (2014) Unilateral climate policy: can OPEC resolve the leakage problem? Energy J 35(4):79–100

Brander JA, Spencer BJ (1985) Export subsidies and international market share rivalry. J Int Econ 18(1–2):83–100. https://doi.org/10.1016/0022-1996(85)90006-6

Burniaux J-M, Oliveira Martins J (2012) Carbon leakages: a general equilibrium view. Economic Theory 49(2):473–495. https://doi.org/10.1007/s00199-010-0598-y

Collier P, Venables AJ (2014) Closing coal: economic and moral incentives. Oxf Rev Econ Policy 30(3):492–512. https://doi.org/10.1093/oxrep/gru024

Collins K, Mendelevitch R (2015) Leaving coal unburned: options for demand-side and supply-side policies. 87. DIW Roundup. German Institute for Economic Research (DIW Berlin), Berlin. http://www.diw.de/documents/publikationen/73/diw_01.c.526889.de/diw_roundup_91_en.pdf

Commonwealth of Australia (2010) Australia’s future tax system. Report to the treasurer. Commonwealth of Australia, Department of Treasury

DEE (2016) Australias emissions projections 2016. Australian Government, Department of Environment and Energy, Camberra

Eisenack K, Edenhofer O, Kalkuhl M (2012) Resource rents: the effects of energy taxes and quantity instruments for climate protection. Energy Policy, Special Section: Frontiers of Sustainability 48:159–166. https://doi.org/10.1016/j.enpol.2012.05.001

Fæhn T, Hagem C, Lindholt L, Mæland S, Rosendahl E (2017) Climate policies in a fossil fuel producing country—demand versus supply side policies. Energy J 38(1):77–102. https://doi.org/10.5547/01956574.38.1.tfae

Gabriel SA, Leuthold FU (2010) Solving discretely-constrained MPEC problems with applications in electric power markets. Energy Econ 32(1):3–14. https://doi.org/10.1016/j.eneco.2009.03.008

Haftendorn C, Holz F, von Hirschhausen C (2012a) The end of cheap coal? A techno-economic analysis until 2030 using the COALMOD-World model. Fuel 102(December):305–325. https://doi.org/10.1016/j.fuel.2012.04.044

Haftendorn C, Kemfert C, Holz F (2012b) What about coal? Interactions between climate policies and the global steam coal market until 2030. Energy Policy 48:274–283. https://doi.org/10.1016/j.enpol.2012.05.032

Harstad B (2012) Buy coal! A case for supply-side environmental policy. J Polit Econ 120(1):77–115. https://doi.org/10.1086/665405

Hoel M (2013) Supply side climate policy and the green paradox. 4094. CESifo Working Paper Series. CESifo Group Munich, Munich

Holz F, Haftendorn C, Mendelevitch R, von Hirschhausen C (2015) The COALMOD-world model: coal markets until 2030. In: Morse RK, Thurber MC (eds) The global coal market - supplying the major fuel for emerging economies. Cambridge University Press, Cambridge, pp 411–472

Holz F, Haftendorn C, Mendelevitch R, von Hirschhausen C (2016) DIW Berlin: a model of the international Steam Coal Market (COALMOD-World). DIW Data Documentation 85. DIW Berlin, Berlin. http://www.diw.de/documents/publikationen/73/diw_01.c.546364.de/diw_datadoc_2016-085.pdf

IEA/OECD (2012a) World energy outlook 2012. World energy outlook. International Energy Agency, OECD Publishing, Paris. https://doi.org/10.1787/weo-2012-en

IEA/OECD (2012b) Coal information 2012. Coal information. International Energy Agency, OECD Publishing, Paris. https://doi.org/10.1787/coal-2012-en

IEA/OECD (2013) Coal information 2013. International Energy Agency, OECD Publishing, Paris. https://doi.org/10.1787/coal-2013-en

IEA/OECD (2015) World energy outlook 2015. World energy outlook. International Energy Agency, OECD Publishing, Paris. https://doi.org/10.1787/weo-2015-en

IEA/OECD (2016a) World energy outlook 2016. World energy outlook. International Energy Agency, OECD Publishing, Paris. https://doi.org/10.1787/weo-2016-en

IEA/OECD (2016b) Coal information 2016. Coal information. International Energy Agency, OECD Publishing, Paris. http://www.oecd-ilibrary.org/energy/coal-information-2016_coal-2016-en

IEA/OECD (2016c) Medium-term coal market report 2016. International Energy Agency, OECD Publishing, Paris. http://www.Oecd-Ilibrary.Org/Content/Book/Mtrcoal-2016-En

Johansson DJA, Azar C, Lindgren K, Persson TA (2009) OPEC strategies and oil rent in a climate conscious world. Energy J 30(3):23–50

Jotzo F, Mazouz S (2015) Brown coal exit: a market mechanism for regulated closure of highly emissions intensive power stations. Economic Analysis and Policy 48:71–81. https://doi.org/10.1016/j.eap.2015.11.003

Kalkuhl M, Brecha RJ (2013) The carbon rent economics of climate policy. Energy Econ 39:89–99. https://doi.org/10.1016/j.eneco.2013.04.008

Kolstad CD, Abbey DS (1984) The effect of market conduct on international steam coal trade. Eur Econ Rev 24(1):39–59. https://doi.org/10.1016/0014-2921(84)90012-6

Kolstad CD, Wolak FA Jr (1985) Strategy and market structure in western coal taxation. Rev Econ Stat 67(2):239–249

Labbé M, Marcotte P, Savard G (1998) A bilevel model of taxation and its application to optimal highway pricing. Manag Sci 44(12):1608–1622

Lazarus M, Erickson P, Tempest K (2015) Supply-side climate policy: the road less taken. Stockholm Environment Institute, Working Paper, no. SEI-WP-2015-13 (October):1–24

Liski M, Tahvonen O (2004) Can carbon tax eat OPEC’s rents? J Environ Econ Manag 47(1):1–12. https://doi.org/10.1016/S0095-0696(03)00052-4

Martin A (2014) Commodity exports and transboundary atmospheric impacts: regulating coal in an era of climate change. Environmental Politics 23(4):590–609. https://doi.org/10.1080/09644016.2014.891788

Matar W, Murphy F, Pierru A, Rioux B (2015) Lowering Saudi Arabia’s fuel consumption and energy system costs without increasing end consumer prices. Energy Econ 49:558–569. https://doi.org/10.1016/j.eneco.2015.03.019

McGlade C, Ekins P (2015) The geographical distribution of fossil fuels unused when limiting global warming to 2 °C. Nature 517(7533):187–190. https://doi.org/10.1038/nature14016

Meinshausen M, Meinshausen N, Hare W, Raper SCB, Frieler K, Knutti R, Frame DJ, Allen MR (2009) Greenhouse-gas emission targets for limiting global warming to 2°C. Nature 458(7242):1158–1162. https://doi.org/10.1038/nature08017

Paulus M, Trüby J (2011) Coal lumps vs. electrons: how do Chinese bulk energy transport decisions affect the global steam coal market? Energy Econ 33(6):1127–1137. https://doi.org/10.1016/j.eneco.2011.02.006

Rogner H-H, Aguilera RF, Archer C, Bertani R, Bhattacharya SC, Dusseault MB, Gagnon L et al (2012) Energy resources and potentials. In: Global energy assessment—toward a sustainable future. Cambridge University Press/International Institute for Applied Systems Analysis, Cambridge, pp 423–512 www.globalenergyassessment.org

Scaparra MP, Church RL (2008) A bilevel mixed-integer program for critical infrastructure protection planning. Comput Oper Res 35(6):1905–1923. https://doi.org/10.1016/j.cor.2006.09.019

Siddiqui S (2011) Solving two-level optimization problems with applications to robust design and energy markets. Dissertation at University of Maryland. College Park. https://drum.lib.umd.edu/handle/1903/12255

Siddiqui S, Gabriel SA (2013) An SOS1-based approach for solving MPECs with a natural gas market application. Networks and Spatial Economics 13(2):205–227. https://doi.org/10.1007/s11067-012-9178-y

Sinn H-W (2008) Public policies against global warming: a supply side approach. Int Tax Public Financ 15(4):360–394. https://doi.org/10.1007/s10797-008-9082-z

Steckel JC, Edenhofer O, Jakob M (2015) Drivers for the renaissance of coal. Proc Natl Acad Sci 112(29):E3775–E3781. https://doi.org/10.1073/pnas.1422722112

Trüby J (2013) Strategic behaviour in international metallurgical coal markets. Energy Econ 36:147–157. https://doi.org/10.1016/j.eneco.2012.12.006

Trüby J, Paulus M (2012) Market structure scenarios in international steam coal trade. Energy J 33(3):91–123. https://doi.org/10.5547/01956574.33.3.4

Acknowledgments

We thank Franziska Holz, Christian von Hirschhausen, Hanna Brauers, Steven A. Gabriel, Clément Haftendorn, Daniel Huppmann, Kai Lessmann, Claudia Kemfert, and Sauleh Siddiqui for helpful discussions and feedback as well as the participants at the Annual Meeting of the German Economic Association in Münster, the EAERE Annual Conference in Helsinki, the IAEE conferences in Düsseldorf and Rome, and at the Berlin Research Seminar on Environment, Resource and Climate Economics. We also thank three anonymous referees for their critical reading and constructive suggestions and guest editors Michael Lazarus and Harro van Asselt for their comments. Philipp M. Richter and Roman Mendelevitch gratefully acknowledge financial support from the DIW Graduate Center as well as funding by the German Ministry of Education and Research (BMBF) within the research framework “Economics of Climate Change” in grant no. 01LA1135B. Frank Jotzo acknowledges funding from the Coal Transitions project led by IDDRI and Climate Strategies and funded by the KR Foundation.

Author information

Authors and Affiliations

Corresponding author

Additional information

This article is part of a Special Issue on ‘Fossil Fuel Supply and Climate Policy’ edited by Harro van Asselt and Michael Lazarus.

Electronic supplementary material

ESM 1

(DOCX 1641 kb)

Rights and permissions

About this article

Cite this article

Richter, P.M., Mendelevitch, R. & Jotzo, F. Coal taxes as supply-side climate policy: a rationale for major exporters?. Climatic Change 150, 43–56 (2018). https://doi.org/10.1007/s10584-018-2163-9

Received:

Accepted:

Published:

Issue Date:

DOI: https://doi.org/10.1007/s10584-018-2163-9