Abstract

This study introduces quasi-geometric discounting into a simple growth model of common capital accumulation that takes consumption externalities into account. We examine how present bias affects economic growth and welfare, and we consider two equilibrium concepts: the non-cooperative Nash equilibrium (NNE) and the cooperative equilibrium (CE). We show that the growth rate in the NNE can be higher than that in the CE if individuals strongly admire the consumption of others regardless of the magnitude of present bias. Contrary to the results in the time-consistent case, we show that, when present bias is incorporated, the welfare level in the NNE can be higher than that in the CE in the initial period. However, in later periods, this relationship can be reversed depending on the difference in the speed of capital accumulation.

Similar content being viewed by others

Notes

Krusell et al. (2002) compare the market equilibrium to the planning equilibrium in a representative-agent model. Surprisingly, they show that the welfare level of the market equilibrium is higher than that of the planning equilibrium.

See Krusell et al. (2002).

Note that if individuals could commit to their future decisions, the problem of time inconsistency would not matter because they could not deviate from their future consumption schedule.

When \(\psi <0\), the uniqueness of \(\sigma ^{*}\) is always guaranteed. When \(0<\psi <1\), the sufficient condition for ensuring the uniqueness of \(\sigma ^{*}\) is \(\beta \ge 2\psi /1+\psi \). The proof is given in Appendix G. The numerical examples in this subsection satisfy this condition.

References

Alpizar, F., Carlsson, F., Johansson-Stenman, O.: How much do we care about absolute versus relative income and consumption? J. Econ. Behav. Organ. 56, 405–421 (2005)

Andersen, T.M., Bhattacharya, J.: Why mandate young borrowers to contribute to their retirement accounts? Econ. Theory (2019). https://doi.org/10.1007/s00199-019-01235-2

Benhabib, J., Radner, R.: The joint exploitation of a productive asset: a game-theoretic approach. Econ. Theory 2, 155–190 (1992)

Bisin, A., Lizzeri, A., Yariv, L.: Government policy with time inconsistent voters. Am. Econ. Rev. 105, 1711–1737 (2015)

Cao, D., Werning, I.: Saving and dissaving with hyperbolic discounting. Econometrica 86, 805–857 (2018)

Clark, A.E., Oswald, A.J.: Satisfaction and comparison income. J. Public Econ. 61, 359–381 (1996)

DellaVigna, S.: Psychology and economics: evidence from the field. J. Econ. Lit. 47, 315–372 (2009)

Dockner, E.J., Sorger, G.: Existence and properties of equilibria for a dynamic game on productive assets. J. Econ. Theory 71, 209–227 (1996)

Dockner, E.J., Nishimura, K.: Capital accumulation games with a non-concave production function. J. Econ. Behav. Organ. 57, 408–420 (2005)

Dockner, E., Wagener, F.: Markov perfect Nash equilibria in models with a single capital stock. Econ. Theory 56, 585–625 (2014)

Dupor, B., Liu, W.F.: Jealousy and equilibrium overconsumption. Am. Econ. Rev. 93, 423–428 (2003)

Easterlin, R.A.: Will raising the incomes of all increase the happiness of all? J. Econ. Behav. Organ. 27, 35–47 (1995)

Frederick, S., Loewenstein, G., O’Donoghue, T.: Time discounting and time preference: a critical review. J. Econ. Lit. 40, 351–401 (2002)

Goldman, S.M.: Intertemporally inconsistent preferences and the rate of consumption. Econometrica 47, 621–626 (1979)

Gordon, H.S.: The economic theory of a common property resource. J. Polit. Econ. 62, 124–142 (1954)

Hardin, G.: The tragedy of the commons. Science 162, 1243–1248 (1968)

Harris, C., Laibson, D.: Dynamic choice of hyperbolic consumers. Econometrica 69, 935–957 (2001)

Hori, K., Shibata, A.: Dynamic game model of endogenous growth with consumption externalities. J. Optim. Theory Appl. 145, 93–107 (2010)

Kagel, J.H., Kim, C., Moser, D.: Fairness in ultimatum games with asymmetric information and asymmetric payoffs. Games Econ. Behav. 13, 100–110 (1996)

Kang, M.: Welfare criteria for quasi-hyperbolic time preferences. Econ. Bull. 35, 2506–2511 (2015)

Krusell, P., Kuruscu, B., Smith, A.J.: Equilibrium welfare and government policy with quasi-geometric discounting. J. Econ. Theory 105, 42–72 (2002)

Laibson, D.: Hyperbolic discount functions, undersaving and savings policy. NBER Working Paper No. 5635 (1996)

Laibson, D.: Golden eggs and hyperbolic discounting. Q. J. Econ. 112, 443–77 (1997)

Levhari, D., Mirman, L.J.: The great fish war: an example using a dynamic Cournot–Nash solution. Bell J. Econ. 11, 322–334 (1980)

Liu, L., Niu, Y., Wang, Y., Yang, J.: Optimal consumption with time-inconsistent preferences. Econ. Theory (2019). https://doi.org/10.1007/s00199-019-01228-1

Liu, W.-F., Turnovsky, S.J.: Consumption externalities, production externalities and long-run macroeconomic efficiency. J. Public Econ. 89, 1097–1129 (2005)

Ljungqvist, L., Uhlig, H.: Tax policy and aggregate demand management under catching up with the joneses. Am. Econ. Rev. 90, 356–366 (2000)

Long, N.V., Wang, S.: Resource-grabbing by status-conscious agents. J. Dev. Econ. 89, 39–50 (2009)

Mino, K.: Growth and bubbles with consumption externalities. Jpn. Econ. Rev. 59, 33–53 (2008)

Mino, K., Nakamoto, Y.: Heterogeneous conformism and wealth distribution in a neoclassical growth model. Econ. Theory 62, 689–717 (2016). https://doi.org/10.1007/s00199-015-0923-6

Mitra, T., Sorger, G.: Extinction in common property resource models: an analytically tractable example. Econ. Theory 57, 41–57 (2014). https://doi.org/10.1007/s00199-013-0799-2

Nowak, A.S.: A multigenerational dynamic game of resource extraction. Math. Soc. Sci. 51, 327–336 (2006)

Nowak, A.S.: On a noncooperative stochastic game played by internally cooperating generations. J. Optim. Theory Appl. 144, 88–106 (2009)

O’Donoghue, T., Rabin, M.: Doing it now or later. Am. Econ. Rev. 89, 103–124 (1999)

O’Donoghue, T., Rabin, M.: Present bias: lessons learned and to be learned. Am. Econ. Rev. 105, 273–279 (2015)

Phelps, E.S., Pollak, R.A.: On second-best national saving and game-equilibrium growth. Rev. Econ. Stud. 35, 185–199 (1968)

Senik, C.: When information dominates comparison learning from Russian subjective panel data. J. Public Econ. 88, 2099–2123 (2004)

Senik, C.: Ambition and jealousy: income interactions in the ‘old’ Europe versus the ‘new’ Europe and the united states. Economica 75, 495–513 (2008)

Strotz, R.H.: Myopia and inconsistency in dynamic utility maximization. Rev. Econ. Stud. 23, 165–180 (1956)

Tornell, A., Velasco, A.: The tragedy of the commons and economic growth: why does capital flow from poor to rich countries? J. Polit. Econ. 100, 1208–1231 (1992)

Turnovsky, S.J., Monteiro, G.: Consumption externalities, production externalities, and efficient capital accumulation under time non-separable preferences. Eur. Econ. Rev. 51, 479–504 (2007)

Zizzo, D.J., Oswald, A.J.: Are people willing to pay to reduce others’ incomes? Annales d’Économie et de Statistique 63(64), 39–65 (2001)

Author information

Authors and Affiliations

Corresponding author

Additional information

Publisher's Note

Springer Nature remains neutral with regard to jurisdictional claims in published maps and institutional affiliations.

The authors are grateful to two anonymous referees for their useful comments and suggestions. We also thank Hiroki Arato, Takeo Hori, Keiichi Morimoto, and participants of the 11th meeting of Association of Behavioral Economics and Finance at Doshisha University, and Economic Theory and Policy Workshop at Aoyama Gakuin University. Any errors are our responsibility.

Appendices

Appendices

1.1 A. Proof of Proposition 1

\(0<\sigma ^n<A/N\) must be satisfied because \(k^{\prime }=(A-N\sigma ^n)k>0\). We denote the left (right)-hand side of (14) as \(f(\sigma ^n)\) (\(g(\sigma ^n)\)). Differentiating \(f(\sigma ^n)\) with respect to \(\sigma ^n\) leads to

Note that \(\psi <1\). Differentiating \(f^\prime (\sigma ^n)\) with respect to \(\sigma ^n\) results in

Note that when \(0<\eta <1\), \(\psi <0\) holds. On the other hand, when \(\eta >1\), \(0<\psi <1\) holds. Moreover, \(f(0)=A^{1-\psi }\) and \(f(A/N)=0\) hold. Differentiating \(g(\sigma ^n)\) with respect to \(\sigma ^n\) leads to

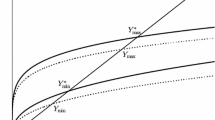

Moreover, \(g(0)=A\delta \) and \(g(A/(N-\beta (1-\alpha )))=0\) hold. Note that when \(N>\beta (1-\alpha )\), \(A/(N-\beta (1-\alpha ))>A/N\) holds. On the other hand, when \(N<\beta (1-\alpha )\), \(A/(N-\beta (1-\alpha ))<0\) holds. From these results, we can graphically examine the existence of the NNE. Figure 5 shows \(f(\sigma ^n)\) and \(g(\sigma ^n)\) when \(N>\beta (1-\alpha )\). Figure 6 shows \(f(\sigma ^n)\) and \(g(\sigma ^n)\) when \(N<\beta (1-\alpha )\). Depending on the magnitude of \(\eta \), there are two cases: (a) and (b). Panels (a) and (b) of Figs. 5 and 6 show that there exists a unique symmetric linear NNE, \(\sigma ^{n*}>0\) if \(A^{-\psi }>\delta \).

Determination of \(\sigma ^n\) when \(N>\beta (1-\alpha )\)

Determination of \(\sigma ^n\) when \(N<\beta (1-\alpha )\)

Determination of \(\sigma ^c\)

1.2 B. Proof of Proposition 2

\(0<\sigma ^c<A/N\) must be satisfied because \(k^{\prime }=(A-N\sigma ^c)k>0\). We denote the left (right)-hand side of (24) as \(q(\sigma ^c)\) (\(m(\sigma ^c)\)). Differentiating \(q(x^c)\) with respect to \(\sigma ^c\) leads to

Note that \(\psi <1\). Differentiating \(q^\prime (\sigma ^c)\) with respect to \(\sigma ^c\) results in

Note that when \(0<\eta <1\), \(\psi <0\) holds. On the other hand, when \(\eta >1\), \(0<\psi <1\) holds. Moreover, \(q(0)=A^{1-\psi }\) and \(q(A/N)=0\) hold. The graph of \(m(\sigma ^c)\) is a straight line:

Moreover, \(m(0)=A\delta \) and \(m(A/N(1-\beta ))=0\) hold. Note that when \(0<\beta <1\), \(A/N(1-\beta )>A/N\) holds. From these results, we can graphically examine the existence of the CE. Figure 7 shows \(q(\sigma ^c)\) and \(m(\sigma ^c)\). Depending on the magnitude of \(\eta \), there are two cases: (a) and (b). Panels (a) and (b) of Fig. 7 show that there exists a unique symmetric linear CE, \(\sigma ^{c*}>0\), if \(A^{-\psi }>\delta \).

1.3 C. Proof of Proposition 3

Note that \(g(\sigma ^n)\) (\(m(\sigma ^c)\)) is the right-hand side of (14) ((24)). We first show that the two growth rates coincide when \(N = 1-\alpha \). When \(N=1-\alpha \), equation (14) is clearly equivalent to (24). Thus, \(\sigma ^{n*}=\sigma ^{c*}\), that is, the two growth rates coincide.

We next examine the following two cases: (1) \(N>1-\alpha \) and (2) \(N<1-\alpha \).

The relationship between \(\sigma ^{n*}\) and \(\sigma ^{c*}\) when \(N>1-\alpha \)

1.3.1 \((1)\ N>1-\alpha \)

When \(N>1-\alpha \), \(N>\beta (1-\alpha )\) must hold. From (A1) and (B1), the graphs of \(g(\sigma ^n)\) and \(m(\sigma ^c)\) are the downward-sloping straight lines. We also obtain

Moreover, \(g(0)=m(0)=A\delta \) holds. Therefore the graph of \(m(\sigma ^c)\) is above that of \(g(\sigma ^n)\). From these results, we can graphically examine the relationship between the two rates of consumption, \(\sigma ^{n*}\) and \(\sigma ^{c*}\) as in Fig. 8. Depending on the magnitude of \(\eta \), there are two cases: (a) and (b). Panels (a) and (b) of Fig. 8 show that when \(N>1-\alpha \),

which means that \(G^c> G^n\).

1.3.2 \((2)\ N<1-\alpha \)

We must distinguish the following two cases: (2-1) \(N<\beta (1-\alpha )\ (<1-\alpha )\) and (2-2) \(\beta (1-\alpha )<N\ (<1-\alpha )\).

The relationship between \(\sigma ^{n*}\) and \(\sigma ^{c*}\) when \(N<\beta (1-\alpha )\ (<1-\alpha )\)

1.3.3 \((2-1)\ N<\beta (1-\alpha )\ (<1-\alpha )\)

From (A1) and (B1), the graph of \(g(\sigma ^n)\) is the upward-sloping straight line and the graph of \(m(\sigma ^c)\) is the downward-sloping straight line. We can graphically examine the relationship between the two rates of consumption, \(\sigma ^{n*}\) and \(\sigma ^{c*}\) (Fig. 9). Depending on the magnitude of \(\eta \), there are two cases: (a) and (b). Panels (a) and (b) of Fig. 9 show that when \(N<\beta (1-\alpha )\),

which means that \(G^c< G^n\).

1.3.4 \((2-2)\ \beta (1-\alpha )<N \ (<1-\alpha )\)

The graphs of \(g(\sigma ^n)\) and \(m(\sigma ^c)\) are the downward-sloping straight lines. Contrary to the case of (1) \(N>1-\alpha \), from (A1) and (B1), we obtain

Thus, the graph of \(m(\sigma ^c)\) is below that of \(g(\sigma ^n)\). We can graphically examine the relationship between the two rates of consumption, \(\sigma ^{n*}\) and \(\sigma ^{c*}\) (Fig. 10). Depending on the magnitude of \(\eta \), there are two cases: (a) and (b). Panels (a) and (b) of Fig. 10 show that when \(\beta (1-\alpha ) <N\),

which means that \(G^c< G^n\).

The relationship between \(\sigma ^{n*}\) and \(\sigma ^{c*}\) when \(\beta (1-\alpha )<N \ (<1-\alpha )\)

The effect of a decrease in \(\beta \) on \(\sigma ^n\) when \(N>\beta (1-\alpha )\)

The effect of a decrease in \(\beta \) on \(\sigma ^n\) when \(N<\beta (1-\alpha )\)

The effect of a decrease in \(\beta \) on \(\sigma ^c\)

1.4 D. Proof of Lemma 1

Note that \(f(\sigma ^n)\) (\(q(\sigma ^c)\)) is the left-hand side of (14) ((24)) and \(g(\sigma ^n)\) (\(m(\sigma ^c)\)) is the right-hand side of (14) ((24)). We show that a decrease in \(\beta \) reduces the growth rates \(G^n\) and \(G^c\). From (14) and (24), the partial derivatives of \(g(\sigma ^n)\) and \(m(\sigma ^c)\) with respect to \(\beta \) are as follows:

This shows that a decrease in \(\beta \) shifts the graphs of \(g(\sigma ^n)\) and \(m(\sigma ^c)\) downward. Moreover, \(\beta \) does not affect \(f(\sigma ^n)\) and \(q(\sigma ^c)\). Thus, we can draw Figs. 11, 12 and 13. Figure 11 shows the effect of a decrease in \(\beta \) on \(\sigma ^n\) when \(N>\beta (1-\alpha )\). Figure 12 shows the effect of a decrease in \(\beta \) on \(\sigma ^n\) when \(N<\beta (1-\alpha )\). Figure 13 shows the effect of a decrease in \(\beta \) on \(\sigma ^c\). Depending on the magnitude of \(\eta \), there are two cases: (a) and (b). Panels (a) and (b) of Figs. 11, 12 and 13 show that decreases in \(\beta \) increase \(\sigma ^{n*}\) and \(\sigma ^{c*}\), which means that decreases in \(\beta \) decrease the growth rates, \(G^n\) and \(G^c\).

1.5 E. Derivation of (27)

If each consumption is symmetric and constant over time, we can calculate the utility of the individuals in period t as follows:

The third equality holds because of \(k_{j+1}=(A-N\sigma ^{i})k_{j}\), \(j=0,1,2, \cdots \). We assume that \(0<\delta (A-N\sigma ^{i})^{\psi }<1\) to guarantee the finiteness of the welfare level. We can rewrite the above utility as follows:

1.6 F. Derivation of (28)

From (27) and \(k_{j+1}=(A-N\sigma ^{i})k_{j}\), \(j=0,1,2, \cdots \), we can calculate

1.7 G. Proof of the uniqueness of \(\sigma ^{*}\)

From (27), differentiating \(W(k_0)\) with respect to \(\sigma \) leads to

From (3), (25), and (26), \(G \equiv A-N\sigma \). Let us define \(L(G ) \equiv 1+(1-\beta )\delta (G )^{\psi }\{ \delta (G )^{\psi }-2\}\) and \(R(G ) \equiv \beta \delta A(G )^{\psi -1}\). Differentiating L(G) and R(G) with respect to G results in

Since \((1-\alpha )>0\), \(k_0>0\), and \(\sigma >0\), we obtain

Therefore, the uniqueness of \(\sigma ^{*}\) is guaranteed if there is a unique \({\widehat{G}}\) that satisfies \(L({\widehat{G}})=R({\widehat{G}})\) and maximizes \(W(k_0)\). We examine how G affects \(L(G )-R(G )\). We must distinguish between the following two cases: \(0<\psi <1\) and \(\psi <0\).

1.7.1 (1) \(0<\psi <1\)

We first examine the feasible interval of G. Since \(\sigma >0\) and \(G>0\), \(0<G<A\) must hold. From Appendix E, we assume that \(0<\delta (G )^{\psi }<1\), which means that \(0<G <\delta ^{-\frac{1}{\psi }}\). Moreover, from Propositions 1 and 2, \(A^{-\psi }>\delta \) must hold for the existence of a unique equilibrium. Thus, \(A<\delta ^{-\frac{1}{\psi }}\). Therefore, the feasible interval of G is \(0<G <A\).

We next examine the difference \(L(G )-R(G )\). Since \(L(0)=1\) and \(\lim _{G \rightarrow 0} R(G )=+ \infty \), we obtain \(\lim _{G \rightarrow 0} L(G )-R(G )<0\). When \(G =A\), we obtain \(L(A)-R(A) =(1-\beta )[\delta (A)^{\psi }]^2-(2-\beta )\delta (A)^{\psi }+1\). From Propositions 1 and 2, \(A^{-\psi }>\delta \) must hold. Thus, \(0<\delta (A)^{\psi }<1\). Let us define \(\Omega \equiv \delta (A)^{\psi }\) and \(Z(\Omega )\equiv (1-\beta )\Omega ^2-(2-\beta )\Omega +1\). \(Z(\Omega )>0\) holds because \(Z(0)=1>0\), \(Z(1)=0\), and \(Z^\prime (\Omega )=2(1-\beta )\Omega -(2-\beta )<0\) for all \(\Omega \in (0, 1)\) and \(\beta \in (0, 1)\). This result implies that \(L(A)-R(A)>0\). Since L(G) and R(G) are decreasing in G when \(0<G <A\), the sufficient condition for the existence of \({\widehat{G}}\) is \(L^\prime (G )>R^\prime (G )\) for all \(G \in (0, A)\). \(L^\prime (G )-R^\prime (G )\) results in

Therefore, if \(\beta \ge 2\psi /1+\psi \) holds, \(L^\prime (G )-R^\prime (G )>0\) holds for all \(G \in (0, A)\). This result shows that the uniqueness of \(\sigma ^{*}\) is guaranteed when \(0<\psi <1\). Note that if \(\beta =1\), the uniqueness of \(\sigma ^{*}\) is always guaranteed.

1.7.2 (2) \(\psi <0\)

We first examine the feasible interval of G. Since \(\sigma >0\) and \(G >0\), \(0<G <A\) must hold. From Appendix E, we assume that \(0<\delta (G )^{\psi }<1\). Thus, \(G >\delta ^{-\frac{1}{\psi }}\). Moreover, from Propositions 1 and 2, \(A^{-\psi }>\delta \) must hold for the existence of a unique equilibrium. This property implies that \(A>\delta ^{-\frac{1}{\psi }}\). Therefore, the feasible interval of G is \(\delta ^{-\frac{1}{\psi }}<G <A\).

We next examine \(L(G )-R(G )\). As in the case of \(0<\psi <1\), we obtain \(L(A)-R(A)>0\). Since \(A^{-\psi }>\delta \) means that \(A\delta ^{\frac{1}{\psi }}>1\), \(L(\delta ^{-\frac{1}{\psi }})-R(\delta ^{-\frac{1}{\psi }})=\beta (1-A\delta ^{\frac{1}{\psi }})<0\) holds. Moreover, when \(\delta ^{-\frac{1}{\psi }}<G <A\), the graph of L(G) is upward sloping and the graph of R(G) is downward sloping. Therefore, when \(\psi <0\) and \(\delta ^{-\frac{1}{\psi }}<G <A\), there always exists a unique \({\widehat{G}}\) that satisfies \(L({\widehat{G}})=R({\widehat{G}})\). Note that if \(\beta =1\), the uniqueness of \(\sigma ^{*}\) is also always guaranteed.

Rights and permissions

About this article

Cite this article

Futagami, K., Nakabo, Y. Capital accumulation game with quasi-geometric discounting and consumption externalities. Econ Theory 71, 251–281 (2021). https://doi.org/10.1007/s00199-019-01243-2

Received:

Accepted:

Published:

Issue Date:

DOI: https://doi.org/10.1007/s00199-019-01243-2