Abstract

The process aimed at discovering new ideas is an economic activity the returns from which are intrinsically uncertain. We extend the neo-Schumpeterian growth framework to investigate the role of strong uncertainty in the innovative process. In particular, we postulate that, when deciding upon R&D efforts, investors hold ‘ambiguous beliefs’ about the exact probability of arrival of the next vertical innovation, and that they face ambiguity via the α −MEU decision rule (Ghirardato et al., J Econ Theory 118:133–173, 2004). Along the balanced growth path, the higher the agent’s ambiguity aversion (α), the lower the R&D efforts and the economic performance. Consistent with cross-country empirical evidence, this causal mechanism suggests that, together with the profitability conditions of the economy, different ‘cultural’ attitudes towards ambiguity may help explain the different R&D efforts observed across countries.

Similar content being viewed by others

Notes

See, among others, Freeman and Soete (1997), Chapter 10.

The UAI is a broad measure of the country-specific cultural attitude towards uncertainty, built by interviewing 88000 IBM employees across more than 70 countries. See the appendix for a detailed description of the index, and for the connection between this index and ambiguity aversion.

Across European countries, the negative correlation is even stronger.

The two-urn version of the experiment goes as follows. There are two urns, each of which contains ten balls, colored either white or black. One of them is known to contain five white balls and five black balls, while no information is given on the distribution of the balls’ colors in the other urn. The decision maker is asked to bet on the color of the first ball drawn at random from either urn, and must decide which urn he or she prefers. The paradox arises whenever people show a preference for the ‘known’ urn, that is, for the urn containing five white and five black balls. This choice behavior cannot be explained by the SEU principle, since there is no subjective (additive) probability distribution that supports these preferences.

The ‘probability’ represents the balance of evidence in favor of a particular proposition, while the ‘weight of evidence’ stands for the quantity of information supporting that balance.

For a discussion of the limits of this approach, see Klibanoff et al. (2005).

Notice that the λ appearing in Eq. 2 and the one appearing in Eq. 3 are distinct, since they refer to the productivity of R&D in discovering, respectively, vintages t + 1 and t + 2. It follows that the structure of this class of models imposes the condition that, when deciding upon R&D activity in t, investors know the exact probabilities of the next two vertical innovations. Of course, in the standard model, this is easily satisifed because λ is assumed constant.

This assumption is meant to exclude the uninteresting cases in which the agent is either totally hopeless about the possibility of innovating ( λ t = 0), or absolutely sure of producing an innovation at the exact instant he or she invests (λ t → + ∞).

Notice that, as opposed to problem 1, now m and M are respectively associated with the maxmax level and the maxmin level.

Research efforts under pure maxmin strategy (MEU criterion) are obtained from Eq. 7 by setting α = 1.

Both a higher quality jump γ and a larger amount of skilled labor force L raise the equilibrium R&D effort \(n_{\alpha }^{\ast }\), while a higher rate of interest r, and a higher value of θ (inversely measuring the degree of market power) lower it.

More precisely, we must distinguish between two conflicting effects. On the one hand, an increase in λ makes the research activity more productive for a given level of employment, thus stimulating the R&D effort. On the other hand, this increase exacerbates the creative destruction effect, reducing the R&D effort. The former effect, however, dominates the latter.

With this statement, we do not want to deny that this routinized investment behavior may change over time. Recent empirical literature finds that organizational routines are not inert (see, for instance, Feldman 2000, 2003). In our framework, routinized R&D efforts would in fact respond to changes in the fundamentals of the economy (or even to shocks possibly hitting the economy if they originate from known distributions). We simply say that agents avoid wasting their (limited) cognitive resources in trying to predict the unpredictable, and that they develop routines when facing pervasive uncertainty.

References

Aghion P, Howitt P (1992) A model of growth through creative destruction. Econometrica 60:323–351

Becker M (2004) Organizational routines: a review of the literature. Ind Corp Change 13(4):643–677

Becker M, Knudsen T (2004) The role of routines in reducing pervasive uncertainty. J Bus Res 58:746–757

Dosi G, Egidi M (1991) Substantive and procedural uncertainty: an exploration of economic behaviours in changing environments. J Evol Econ 1:145–168

Egidi M (1996) Routines, hierarchies of problems, procedural behaviour: some evidence from experiments. In: Arrow E et al (eds) The rational foundations of economic behaviour. Macmillan London, pp 303–333

Ellsberg D (1961) Risk, ambiguity and the savage axioms. Q J Econ 75:643–669

Feldman MS (2000) Organizational routines as a source of continuous change. Organ Sci 11:611–629

Feldman MS (2003) A performative perspective on stability and change in organizational routines. Ind Corp Change 12:727–752

Freeman C, Soete L (1997) The economics of industrial innovation, 3rd edn. The MIT Press

Ghirardato P, Maccheroni F, Marinacci M (2004) Differentiating ambiguity and ambiguity attitude. J Econ Theory 118:133–173

Gilboa I, Schmeidler D (1989) Maxmin expected utility with non-unique prior. J Math Econ 18:141–153

Grossman GM, Helpman E (1991) Quality ladders in the theory of growth. Rev Econ Stud 58:43–61

Heiner R (1983) The origin of predictable behaviour. Am Econ Rev 73:560–595

Hofstede GH (1980) Culture’s consequences: international differences in work-related values. Sage Publications, London

Hofstede GH (2001) Culture’s consequences: comparing values, behaviors, institutions and organizations across nations. Sage, Thousand Oaks, CA

Huang R (2008) Tolerance for uncertainty and the growth of informationally opaque industries. J Dev Econ 87(2):333–353

Hurwicz L (1951) Optimality criteria for decision-making under ignorance. Cowles Commission Discussion Paper No. 370

Keynes JM (1921) A treatise on probability. Macmillan&Co, London

Klibanoff P, Marinacci M, Mukerji S (2005) A smooth model of decision making under ambiguity. Econometrica 73:1849–1892

Knight F (1921) Risk, uncertainty and profit. Houghton Mifflin Company

Nelson R, Winter S (1982) An evolutionary theory of economic change. Harvard University Press, Cambridge, MA

Romer PM (1990) Endogeneous technological change. J Polit Econ 98:S71–S102

Rosenberg N (1994) Exploring the black box. Cambridge University Press, Cambridge, Massachusetts

Savage LJ (1954) The foundations of statistics. Wiley, New York

Schmeidler D (1989) Subjective probability and expected utility without additivity. Econometrica 57:571–587

Shane SA (1993) Cultural influences on national rates of innovation. J Bus Venturing 8:59–73

Acknowledgements

We are grateful to an anonymous referee for his/her precious suggestions. We would also like to thank seminar participants at the European University Institute (EUI), at the University of Heidelberg and at the University of Rome “La Sapienza”. Paolo E. Giordani thankfully acknowledges financial support from the Robert Schuman Centre for Advanced Studies at the EUI.

Author information

Authors and Affiliations

Corresponding author

Appendix: The uncertainty avoidance index

Appendix: The uncertainty avoidance index

The Uncertainty Avoidance Index has been computed for 72 countries, by interviewing 88000 IBM employees from 1967 to 1973, and asking the three following questions:

-

1.

Rule orientation: agreement with the statement “Company rules should not be broken, even when the employee thinks it is in the company’s best interest” (5-point answer scale, from “strongly agree” to “strongly disagree”: the more rule-oriented, the more uncertainty-avoiding).

-

2.

Employment stability: employees’ statement that they intend to continue with the company (1) for 2 years at most, (2) from 2 to 5 years, (3) more than 5 years (but before retiring), (4) until they retire (the more stability-seeking, the more uncertainty-avoiding).

-

3.

Stress, as expressed in the mean answer to the question “How often do you feel nervous or tense at work?” (5-point answer scale from “I always feel this way” to “I never feel this way”: the more stressed, the more uncertainty-avoiding).

The number is computed on the basis of the country mean scores for the answers given to the questions above, and the exact formula is the following:

The index ranges from a minimum of − 150 to a maximum of + 230. This kind of experiment has been replicated over time - even using different populations, and slightly different questions as a consequence -, and the original country rankings have always been broadly confirmed (to prove the persistence over time of ‘cultural values’).

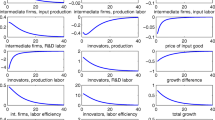

The link between the UAI and the α −MEU decision rule is intuitively strong. The UAI can roughly be considered as a proxy of parameter α across countries, in measuring their different degree of tolerance towards ambiguity. Although intuitively sound, this relationship is admittedly problematic in one respect which is worth remarking. While our theoretical formalization can easily distinguish between ambiguity (that is, the structural uncertainty of the decision setting measured by the width of the interval [m,M]) and attitude towards ambiguity (measured by coefficient α), the UAI does not. To give a simple example, the agent’s answer to the ‘employment stability’ question is probably dictated by both her personal taste for ambiguity and the labor market conditions of her country. In capturing both uncertainty and uncertainty attitude, the UAI can probably be seen in connection with the perceived variance in the interarrival time of innovations (see Subsection 5.3). This variance is a measure of uncertainty in the innovation process, which is affected by both the ‘subjective’ evaluation of λ t and by the effect of this evaluation on the amount of R&D efforts (\(n_{\alpha }^{\ast }\)). It then incorporates both uncertainty and the attitude towards it. In either interpretation, the causal mechanism highlighted in the model, according to which a fall in the ambiguity aversion index α leads to an increase in R&D employment \(n_{\alpha }^{\ast }\), is well in accord with the negative correlations between UAI and the different measures of R&D activity shown in Figs. 1 and 2.

Rights and permissions

About this article

Cite this article

Cozzi, G., Giordani, P.E. Ambiguity attitude, R&D investments and economic growth. J Evol Econ 21, 303–319 (2011). https://doi.org/10.1007/s00191-010-0217-x

Published:

Issue Date:

DOI: https://doi.org/10.1007/s00191-010-0217-x

Keywords

- Schumpeterian growth

- R&D investments

- Arrival rate of innovation

- Ambiguity

- Cultural attitude towards ambiguity