Abstract

Industries based on systemic technologies are often characterized by a dynamically evolving market structure. The market structure that provides the context for firms’ investment choices itself evolves due to the feedback effect of firms’ investments. In such cases, analyses of investment-performance relationship, purporting to explain sustainable competitive advantages, should ideally account for the endogeneity of the determinants of market structure—technology, demand, and policy—and firms’ investment choices. This paper focuses on the endogeneity of the demand-side determinants of market structure and firms’ demand-side investments under the assumed conditions of constant technology and policy environment. In doing so it contradicts the extant depiction of the evolution of industrial market structure in the above context as primarily caused by the evolution of underlying technological system in response to firms’ endogenous technological investments that generate sustainable competitive advantage for the dominant firms. A dynamic evolutionary model of demand competition captures the competition in the downstream market for basic industry product and its complements in an industry based on systemic technology during its post-interoperability stage. A natural experiment drawn from the US Long-distance telecommunications services industry during 1984–1996 allows testing the hypotheses drawn from the above model in a panel data setting.

Similar content being viewed by others

Notes

For instance, the decline in price is attributable to commoditization of the underlying technology, a common feature in technologically sophisticated industries.

However, theses costs may continuously decline over time due to exogenous technological improvements.

For instance, a firm does not know the switching cost of its rivals’ customers and hence cannot calculate the optimal discount at which the customers would switch or the advertising budget to which they will respond.

For instance, each firm’s unique demand-side competence enables it to impose a switching cost on its customers.

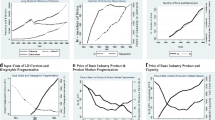

The absence of temporally varying structural variables in the analysis of investment-performance relationships specifically poses problems in the context of industries based on systemic technologies. It is commonly understood that in such industries performance characteristics of the market structure at any period influences firm performance. For instance, the total sales of any firm i at any period t are influenced by (a) the lagged effect of a firm’s sales in the preceding period (direct network effect), and (b) the effect of total industry sales of the generic (or base product) during that period on a firm’s sale of complements (indirect network effect).

In a fragmented industry the allocation of market share in one market segment could be independent of that in other market segment.

NECA collected this information for FCC since the latter recovered certain expenses as from those long distance carriers whose share of the total PSLs equaled or exceeded 0.05% towards Universal Service Fee. The PSL system for billing Universal Service Fee went into effect in April 1, 1989 and ended in December 1997 as FCC changed its rules on universal service following the passage of Telecommunications Act of 1996.

All long-distance firms expensed advertising costs as incurred in accordance with the American Institute of Certified Public Accountants (AICPA) Statement of Position No. 93–7, “Reporting on Advertising Costs”. However, they amortized certain types of advertising costs and other intangible assets such as customer lists, deferred debt issuance costs, and goodwill over the expected period of future benefit.

The future benefits of R&D and advertising are documented in the accounting literature (e.g., Bublitz and Ettredge 1989; Lev and Souginannis 1996). Further, Kovacs (2004) documents the future benefits of a calculated SGA capital (excluding advertising and R&D expenses), which varies across industries and persists for up to 4 years.

A firm’s demand-side operating cost can be mapped onto two intended effects: customer acquisition and customer retention. Customer acquisition cost supports a firm’s strategy to increase its customer base in existing or new market segments. The typical sales and marketing costs of obtaining new subscribers include advertising and a direct expense applicable to most new subscribers, either in the form of a commission payment to an agent or a salary/incentive payment to a direct sales person. Customer retention cost supports a firm’s strategy to penetrate existing markets and typically includes cost for providing customer care services. It also includes cost incurred to expand the company’s service offerings, designed to reduce the effects of unit price decreases for services and to decrease the likelihood that customers will switch.

The interpretation of other coefficients is as follows. \(\upgamma\)00 = 6.265659 = Initial status or the intercept for vertically integrated firms (Vi = 0) is significantly greater than zero (p < 0.001). \(\upgamma\)01 = 0.650909 = the difference in intercept between vertically integrated and vertically disintegrated firms is also significantly different from zero (p < 0.1). \(\upgamma \)10 = 0.432167 = the slope (or the rate of change of the customer-base with age) of vertically integrated firms is significantly different from zero (p < 0.001). The likelihood ratio test confirms the variances as significantly different from zero [LR test vs. linear regression: chibar2 (01) = 38.65; p < 0.001]. First, the residual variance in covariance = \(\upsigma\)2 01 = 0.3898692. It is the covariance of individual intercepts and slopes and summarizes size and direction of association between initial status and rate of change controlling for choice of vertical disintegration (Vi = 1). This means there exists a scope for including other predictors which could possibly explain the difference in variation in slope among firms. Second, the residual variance = \(\upsigma\)2 \(\upvarepsilon \) = 5.880555. It summarizes population variability in average firm’s outcome values around the firm’s change trajectory.

References

Adner R (2002) When are technologies disruptive: a demand-based view of the emergence of competition. Strateg Manage J 23:667–688

Adner R, Levinthal D (2001) Demand heterogeneity and technology evolution: implications for product and process innovation. Manage Sci 47(5):611–628

Arora A, Fosfuri A, Gambardella A (2001) Markets for technology: economics of innovation and corporate strategy. MIT Press, Cambridge

Athey S, Schmutzler A (2001) Investment and market dominance. Rand J Econ 32(1):1–26

Bakos Y, Brynjolfsson E (1999) Bundling information goods: pricing, profits, and efficiency. Manage Sci 45(12):1613–1630

Bublitz B, Ettredge M (1989) The information in discretionary outlays: advertising, research and development. Account Rev 64:108–124

Bulow J, Geanokoplos J, Klemperer P (1985) Holding excess capacity to deter entry. Econ J 95:178–182

Carlton DW, Waldman M (2002) The strategic use of tying to preserve and create market power in evolving industries. Rand J Econ 33: 194–220

Dixit A (1980) The role of investment in entry deterrence. Econ J 90:95–106

Ericson R, Pakes A (1995) Markov-perfect industry dynamics: a framework for empirical work. Rev Econ Stud 62(1):53–82

Farrell J, Saloner G (1986) Installed base and compatibility: innovation, product preannouncement, and predation. Am Econ Rev 76:940–955

FCC (1997) In: Lande J, Rangos K (ed) Carrier locator: interstate service providers. Industry Analysis Division, FCC, Washington, DC, p 20554

FCC (1999) In: Zolnierek J, Rangos K, Eisner J (eds) Long distance market shares fourth quarter 1998. Industry Analysis Division, FCC, Washington, DC, p 20554

FCC (2001) Statistics of the long distance telecommunications industry. Industry Analysis Division, Washington, DC, p 20554

Ghemawat P (1984) Capacity expansion in the titanium dioxide industry. J Ind Econ 33:145–163

Gilbert R, Vives X (1986) Entry deterrence and the free rider problem. Rev Econ Stud 53:71–83

Greve HR (2008) Multi-market contact and sales growth: evidence from insurance. Strateg Manage J 29(3):229–249

Gupta S, Lehmann DR (2003) Customers as assets. J Interact Market 17(1):9–24

Harrigan KR (1985) Vertical integration and corporate strategy. Acad Manage J 28(3):397–425

Henderson RM, Clark KB (1990) Architectural innovation: the reconfiguration of existing product technologies and the failure of established firms. Adm Sci Q 35:9–30

Klemperer P (1995) Competition when consumers have switching costs: an overview with applications to industrial organization, macroeconomics, and international trade. Rev Econ Stud 62:515–539

Katz M, Shapiro C (1994) Systems competition and network effects. J Econ Perspect 8(2):93–115

Klemperer P (1995) Competition when consumers have switching costs: an overview with applications to industrial organization, macroeconomics, and international trade. Rev Econ Stud 62:515–539

Klepper S (1996) Entry, exit, growth, and innovation over the product life cycle. Am Econ Rev 86(3):562–583

Klepper S (2002) Firm survival and the evolution of oligoply. Rand J Econ 33(1):37–61

Knittel CR (1997) Interstate long-distance rates: search costs, switching costs, and market power. Rev Ind Organ 12(4):519–536

Kovacs G (2004) The future benefits in selling, general, and administrative expenses. Unpublished dissertation, Columbia University

Lancaster K (1990) The economics of product variety: a survey. Market Sci 9(3):189–206

Lev B, Sougiannis T (1996) The capitalization, amortization, and value-relevance of R&D. J Account Econ 21:107–138

Lieberman M (1987) Excess capacity as a barrier to entry: an empirical appraisal. J Ind Econ 35:607–627

McAfee RP, McMillan J, Whinston MD (1989) Multiproduct monopoly, commodity bundling, and correlation of values. Q J Econ 104:371–384

McLean RP, Riordan MH (1989) Industry structure with sequential technology choice. J Econ Theory 47:1–21

Nalebuff B (2004) Bundling as an entry barrier. Q J Econ 119(1):159–187

Nelson RR, Winter SG (1982) An evolutionary theory of economic change. Belknap Press, Cambridge

Nelson RR, Winter SG (2002) Evolutionary theorizing in economics. J Econ Perspect 16(3):23–46

Noda T, Collis DJ (2001) The evolution of intraindustry firm heterogeneity: insights from a process study. Acad Manage J 44(4):897–925

Olley GS, Pakes A (1996) The dynamics of productivity in the telecommunications equipment industry. Econometrica 64(6):1263–1297

Ordover J, Saloner G, Salop S (1990) Equilibrium vertical foreclosure. Am Econ Rev 80:127–142

Pakes A, McGuire P (1994) Computing mark-perfect Nash equilibria: numerical implications of a dynamic differentiated product model. Rand J Econ 25(4):555–589

Spence M (1977) Entry, capacity, investment and oligopolistic pricing. Bell J Econ 8:534–544

Sutton J (1991) Sunk costs and market structure: price competition, advertising, and the evolution of concentration. MIT Press, Cambridge

Sutton J (1998) Technology and market structure. MIT Press, Cambridge

vonHippel E (1988) The sources of innovation. Oxford University Press, New York

Waldman M (1987) Noncooperative entry deterrence, uncertainty, and the free-rider problem. Rev Econ Stud 54:301–310

Waldman M (1991) The role of multiple potential entrants/sequential entry in noncooperative entry deterrence. Rand J Econ 22:446–453

Whinston MD (1990) Tying, foreclosure, and exclusion. Am Econ Rev 80(4):837–859

Wooldridge JM (2002) Econometric analysis of cross section and panel data. MIT Press, Cambridge

Author information

Authors and Affiliations

Corresponding author

Additional information

This paper is based on my dissertation research at Columbia Business School, Columbia University. I highly appreciate the guidance of my thesis advisors—Richard R Nelson and Kathryn Harrigan—and valuable inputs by other committee members—Ashish Arora, Ron Adner, and Bhaven Sampat—in shaping my thesis. I also highly appreciate the kindness of Mr Rick Askoff, NECA for providing me access to the NECA proprietary dataset. Finally, I thank Dr Michael Eisner & Mr Jim Landis of the FCC along with Mr. Robert C Atkinson, Mr. John Manning, and Ms. Nancy Fears of the NANPA for their valuable information on various facets of the telecom sector and helping me navigate through the maze of telecommunications statistics.

Rights and permissions

About this article

Cite this article

Manral, L. Demand competition and investment heterogeneity in industries based on systemic technologies: evidence from the US long-distance telecommunications services industry, 1984–1996. J Evol Econ 20, 765–802 (2010). https://doi.org/10.1007/s00191-010-0175-3

Published:

Issue Date:

DOI: https://doi.org/10.1007/s00191-010-0175-3