Abstract

What are the output responses to fiscal policy? Although important contributions have been made in the literature, quantifying the size of the fiscal multiplier remains a challenge. Indeed, the challenge of estimating a unique fiscal multiplier is probably an ill-posed one. The magnitude of the multiplier may well depend on country- and time-specific characteristics of the fiscal stance under scrutiny. In this paper, we estimate state-specific multipliers for Spain depending on the state of the economy along several dimensions. The government spending multiplier is estimated to be larger during recessions and banking stress periods, but much smaller (or even negative) during periods of weak public finances. Combining these three dimensions into a single global turmoil indicator via principal component analysis, the estimated multipliers are 1.4 for crisis (or turbulent) times and 0.6 for tranquil times.

Similar content being viewed by others

Notes

In addition to the fiscal VARs literature, some studies focus on analyzing episodes of large fiscal adjustments and their macroeconomic consequences. Based on statistical correlations between output growth and changes in the structural primary deficit, many of these studies conclude that fiscal consolidations might be expansionary for an economy depending on the composition of the adjustment (see e.g., Alesina and Ardagna 1998). However, after accounting for reverse causality between the fiscal adjustment and economic activity, IMF (2010) as well as Hernandez de Cos and Moral-Benito (2013) concludes that fiscal consolidations per se are not expansionary in the short run.

The fixed exchange rate regime might also amplify the effects of fiscal policy in Spain; however, the lack of within-time variation in our Spanish data precludes the consideration of fiscal multiplier heterogeneity across exchange rate regimes within our econometric approach. Note that empirical studies investigating this dimension exploit cross-country variation in exchange rate regimes (see Corsetti et al. 2012; Ilzetzki et al. 2013).

From a practical point of view, within the STVAR approach all observations in the sample can be used for estimation of the parameters in both regimes.

However, they find slightly smaller spillover effects in countries sharing a fixed exchange rate in spite of the inability of those countries to offset fiscal shocks from abroad via exchange rate policy.

We only provide here a brief enumeration of the papers in this literature, for reasons of space (see the working-paper version of this paper for a more detailed discussion on the identification challenge in the fiscal VAR literature).

In particular, BP02 argue that the reduced form shock to the fiscal variable is formed by three components, namely (i) the automatic response of the fiscal variable to innovations in output (e.g., an unanticipated change in tax revenues caused by a shock to output for given tax rates); (ii) the discretionary response of fiscal policy to output shocks (e.g., a reduction in the tax rate in a recession); and (iii) the pure random shock to the fiscal variable uncorrelated with any other structural shock (i.e., the structural shock we aim to identify).

Moreover, the literature has usually focused on government spending shocks more than tax shocks. The main reason is that unexpected changes in tax revenues within a quarter may arise as a result of changes in the relationship between economic activity and tax revenues rather than changes in discretionary fiscal policy. In this respect, the reliability of tax elasticities is crucial to purge the changes in tax revenues, but these elasticities may well depend on the state of the economy which further complicates the identification of tax shocks. As recently advocated by Riera-Crichton et al. (2012), the use of narrative approaches together with tax rates as a measure of tax policy —instead of commonly used revenue-based measures—represents a promising alternative to estimate tax multipliers.

The debate on the appropriateness of the fiscal multipliers used for estimating the impact of austerity programs has been recently revived by Blanchard and Leigh (2013)—who further develop the initial analysis published Box 1.1 of the October 2012 WEO. These authors suggest than fiscal multipliers considered for forecasting have been excessively low in the aftermath of the global crisis. This conclusion follows from the negative and significant relationship between growth forecast errors and the size of the associated fiscal policy change.

Along these lines, Parker (2011) argues that it is difficult to assess the effectiveness of countercyclical fiscal policy during recessions because deep recessions are few. The lack of data is even more pronounced when estimating the effects of contractionary fiscal policy during a recession, the policy that some countries in the Eurozone are currently undertaking.

Indeed, the proliferation of coefficients to be estimated combined with the reduced sample size available for estimation preclude us from including additional variables in the model.

The index \(z\) is dated at \(t-1\) to avoid contemporaneous feedbacks from policy actions to the state of the economy.

Note also that, besides the STVAR approach, a threshold VAR (TVAR) can also be considered for this purpose; however, we prefer the STVAR alternative because it allows the regimes to change smoothly from one regime to another, while the TVAR impose discrete switches from one to another regime. Moreover, this implies that within the STVAR approach, all observations in the sample can be used for estimation of the parameters in both regimes.

Fiscal variables are expressed in real terms using the GDP deflator.

See De Castro et al. (2014) for an in-depth analysis of the Spanish fiscal stance over this period.

Auerbach and Gorodnichenko (2012a) consider both the GDP growth and the output gap as \(z_t\) indicators for the USA. In addition, we also consider here the change in the unemployment rate.

The volume of credit to households over disposable income is also taken from the Banco de España database.

More concretely, we follow Auerbach and Gorodnichenko (2012a) and consider the seven-quarter moving average of these variables.

Alternatively, one could also consider the level of unemployment rate. However, given the high persistence of this variable in Spain, its interpretation as a proxy of the business cycle is less clear. Also, the share of unemployed people can also be interpreted as an indicator of constrained consumers in the economy that might also affect the magnitude of the fiscal multiplier. In any event, estimates based on this indicator are in line with those based on the change in the unemployment rate. To save space, these results are not reported here, but are available upon request.

In particular, we report the impact multiplier \(\left( \frac{\Delta \hbox {GDP}_t}{\Delta G_t}\right) \), the cumulative multiplier at some horizon \(H \left( \frac{\sum _{j=0}^{H}\Delta \hbox {GDP}_{t+j}}{\sum _{j=0}^{H}\Delta G_{t+j}}\right) \), and the peak multiplier over any horizon \(H \left( \max \frac{\Delta \hbox {GDP}_{t+H}}{\Delta G_t}\right) \).

In particular, \(\gamma \) is calibrated to 5, 10, and 2 for the deficit-to-GDP ratio, the change in gross debt, and the debt-to-GDP ratio, respectively. Note that our results are robust to other calibrations of the \(\gamma \) parameter, see Sect. 4.5.

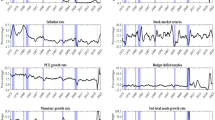

More concretely, the weights are 0.38, 0.23, 0.36, 0.43, 0.41, 0.19, 0.37, and 0.36 for GDP growth, the output gap, the change in the unemployment rate, the deficit-to-GDP ratio, the change in gross debt, the debt-to-GDP ratio, the aggregate default rate, and the flow of private credit, respectively. Note also that the sign of some indicators is modified accordingly so that low values in absolute terms are associated with “crisis” periods.

Note also that, in Fig. 13, we calibrate \(\gamma =5\) as we did for most of the individual \(z_t\) indicators in previous sections. In any case, the weights resulting from other values are very similar and also match the shaded regions.

References

Afonso A, Baxa J, Slavik M (2011) Fiscal developments and financial stress: a threshold VAR analysis. European Central Bank Working Paper 1319

Alesina A, Ardagna S (1998) Tales of fiscal adjustment. Econ Policy 27:487–545

Almunia M, Benetrix A, Eichengreen B, O’Rourke K, Rua G (2010) From great depression to great credit crisis: similarities, differences and lessons. Econ Policy 25:219–265

Andres J, Bosca J, Ferri J (2012) Household leverage and fiscal multipliers. Banco de España Working Paper 1215

Auerbach A, Gorodnichenko Y (2012a) Measuring the output responses to fiscal policy. Am Econ J Econ Policy 4:1–27

Auerbach A, Gorodnichenko Y (2012b) Fiscal multipliers in recession and expansion. In: Alesina A, Giavazzi F (eds) Fiscal policy after the financial crisis. University of Chicago Press, Chicago

Auerbach A, Gorodnichenko Y (2013) Output spillovers from fiscal policy. Am Econ Rev Pap Proc 103:141–146

Barro R, Redlick C (2011) Macroeconomic effects from government purchases and taxes. Q J Econ 126:51–102

Batini N, Callegari G, Melina G (2012) Successful Austerity in the United States. Europe and Japan IMF WP 12/190

Baum A, Koester G (2011) The impact of fiscal policy on economic activity over the business cycle evidence from a threshold VAR analysis. Deutsche Bundesbank Discussion Paper 03/2011

Baum A, Poplawski-Ribeiro M, Weber A (2012) Fiscal multipliers and the state of the economy. IMF WP 12/286

Blanchard O, Leigh D (2013) Growth forecast errors and fiscal multipliers. IMF WP 13/001

Blanchard O, Perotti R (2002) An empirical characterization of the dynamic effects of changes in government spending and taxes on output. Q J Econ 117:1329–1368

Christiano L, Eichenbaum M, Rebelo S (2011) When is the government spending multiplier large? J Polit Econ 119:78–121

Corsetti G, Meier A, Muller G (2012) What determines government spending multipliers? Econ Policy 27:521–565

De Castro F (2006) The macroeconomic effects of fiscal policy in Spain. Appl Econ 38:913–924

De Castro F, Hernandez de Cos P (2008) The economic effects of fiscal policy: the case of Spain. J Macroecon 30:1005–1028

De Castro F, Marti F, Montesinos A, Perez JJ, Sanchez-Fuentes AJ (2014) Fiscal policies in Spain: main stylized facts revisited. Banco de España Working Paper 1408, Madrid

Fatas A, Mihov I (2001) The effects of fiscal policy on consumption and employment: theory and evidence. CEPR Discussion Papers 2760

Favero C (2002) How do European monetary and fiscal authorities behave? CEPR Discussion Papers 3426

Favero C, Giavazzi F, Perego J (2011) Country heterogeneity and the international evidence on the effects of fiscal policy. IMF Econ Rev 59:652–682

Ferraresi T, Roventini A, Fagiolo G (2013) Fiscal policies and credit regimes: a TVAR approach. LEM Working Paper Series, Scuola Superiore Sant’ Anna

Fry R, Pagan A (2011) Sign restrictions in structural vector autoregressions: a critical review. J Econ Lit 49:938–960

Gali J, Lopez-Salido D, Valles J (2007) Understanding the effects of government spending on consumption. J Eur Econ Assoc 5:227–270

Granger C, Terasvirta T (1993) Modelling nonlinear economic relationships. Oxford University Press, New York

Hebous S (2011) The effects of discretionary fiscal policy on macroeconomic aggregates: a reappraisal. J Econ Surv 25:674–707

Hernandez de Cos P, Moral-Benito E (2013) Fiscal consolidations and economic growth. Fisc Stud 34:491–515

Ilzetzki E, Mendoza E, Vegh C (2013) How big (small?) are fiscal multipliers? J Monet Econ 60:239–254

IMF (2010) Will it hurt? Macroeconomic effects of fiscal consolidation. World Economic Outlook, Chapter 3

Jorda O (2005) Estimation and inference of impulse responses by local projections. Am Econ Rev 95:161–182

Mountford A, Uhlig H (2009) What are the effects of fiscal policy shocks? J Appl Econom 24:960–992

Nickel C, Tudyka A (2013) Fiscal stimulus in times of high debt: reconsidering multipliers and twin deficits. ECB Working Paper 1513

Parker J (2011) On measuring the effects of fiscal policy in recessions. J Econ Lit 49:703–718

Perotti R (1999) Fiscal policy in good times and bad. Q J Econ 114:1399–1436

Ramey V (2011) Identifying government spending shocks: it’s all in the timing. Q J Econ 126:1–50

Ramey V, Shapiro M (1998) Costly capital reallocation and the effects of government spending. Carnegie–Rochester Conf Ser Public Policy 48:145–194

Ramey V, Zubairy S (2013) Government spending multipliers in good times and in bad: evidence from U.S. historical data. University of California, San Diego, Mimeo

Reinhart C, Rogoff K (2010) From financial crash to debt crisis. NBER Working Paper 15795

Riera-Crichton D, Vegh C, Vuletin G (2012) Tax multipliers: pitfalls in measurement and identification. NBER Working paper 18497

Riera-Crichton D, Vegh C, Vuletin G (2015) Procyclical and countercyclical fiscal multipliers: evidence from OECD countries. J Int Money Finance 52:15–31

Romer C, Bernstein J (2009) The job impact of the American recovery and reinvestment plan. Council of Economic Advisors, January 9

Romer C, Romer D (2010) The macroeconomic effects of tax changes: estimates based on a new measure of fiscal shocks. Am Econ Rev 100:763–801

Vegh C, Vuletin G (2014) The road to redemption: policy response to crises in Latin America. IMF Econ Rev 62:526–568

Author information

Authors and Affiliations

Corresponding author

Additional information

Special thanks are due to Francisco De Castro and Javier Perez for sharing their fiscal data, and Javier Ferri for fruitful discussion. We also thank Pablo Burriel, Jorge Martínez Pagés, Eva Ortega, Gaby Pérez Quirós, and Alberto Urtasun for helpful comments. We are also grateful to the Editor and two anonymous referees for insightful suggestions that led to a substantial improvement in the paper.

Rights and permissions

About this article

Cite this article

Hernández de Cos, P., Moral-Benito, E. Fiscal multipliers in turbulent times: the case of Spain. Empir Econ 50, 1589–1625 (2016). https://doi.org/10.1007/s00181-015-0969-0

Received:

Accepted:

Published:

Issue Date:

DOI: https://doi.org/10.1007/s00181-015-0969-0